Since April 2021, the S&P 500 has delivered a total return of 61.5%. But one standout stock has nearly doubled the market - over the past five years, BJ's has surged 116% to $98.06 per share. Its momentum hasn’t stopped as it’s also gained 8.8% in the last six months, beating the S&P by 11.2%.

Is now the time to buy BJ's, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is BJ's Not Exciting?

Despite the momentum, we're sitting this one out for now. Here are three reasons you should be careful with BJ and a stock we'd rather own.

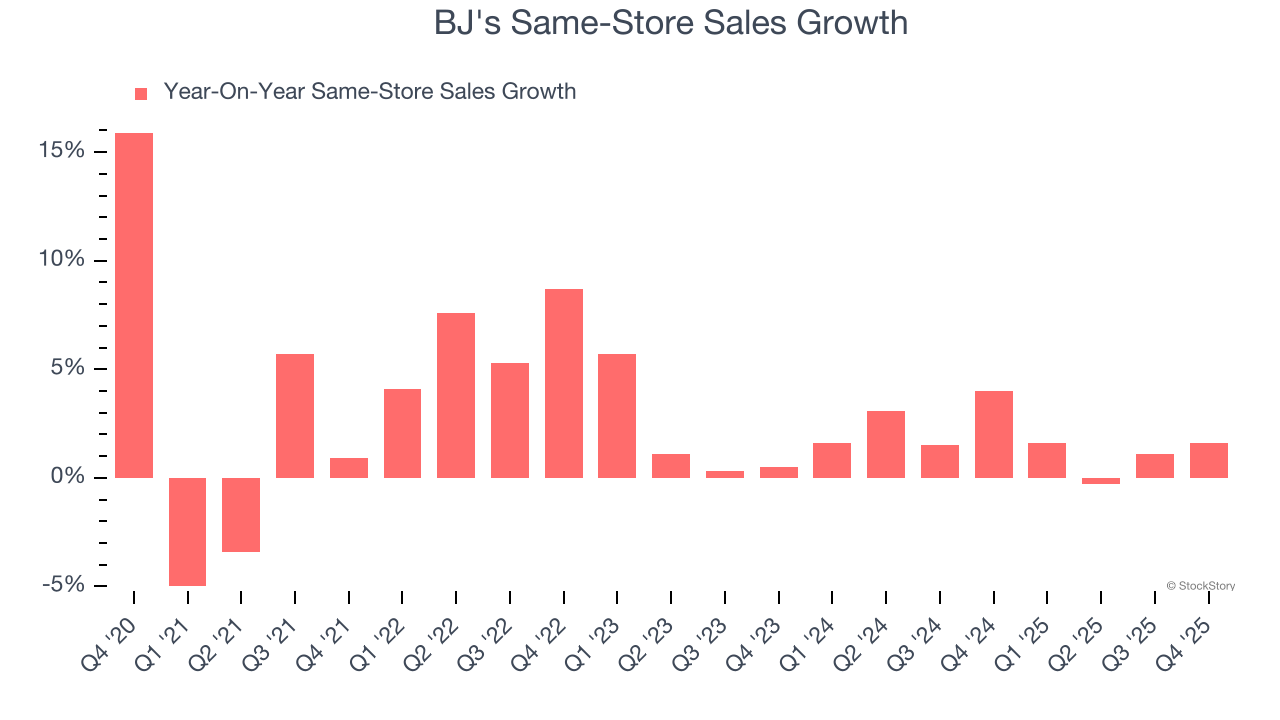

1. Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

BJ’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.8% per year.

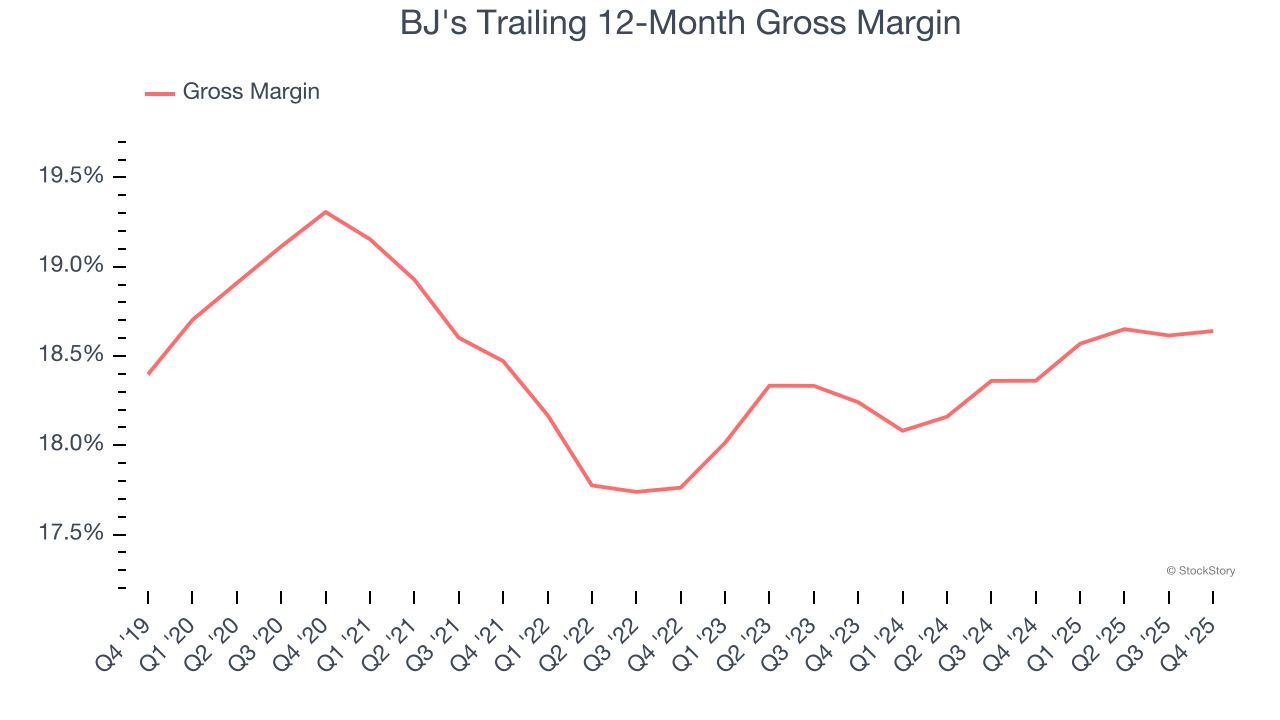

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

BJ's has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 18.5% gross margin over the last two years. Said differently, BJ's had to pay a chunky $81.50 to its suppliers for every $100 in revenue.

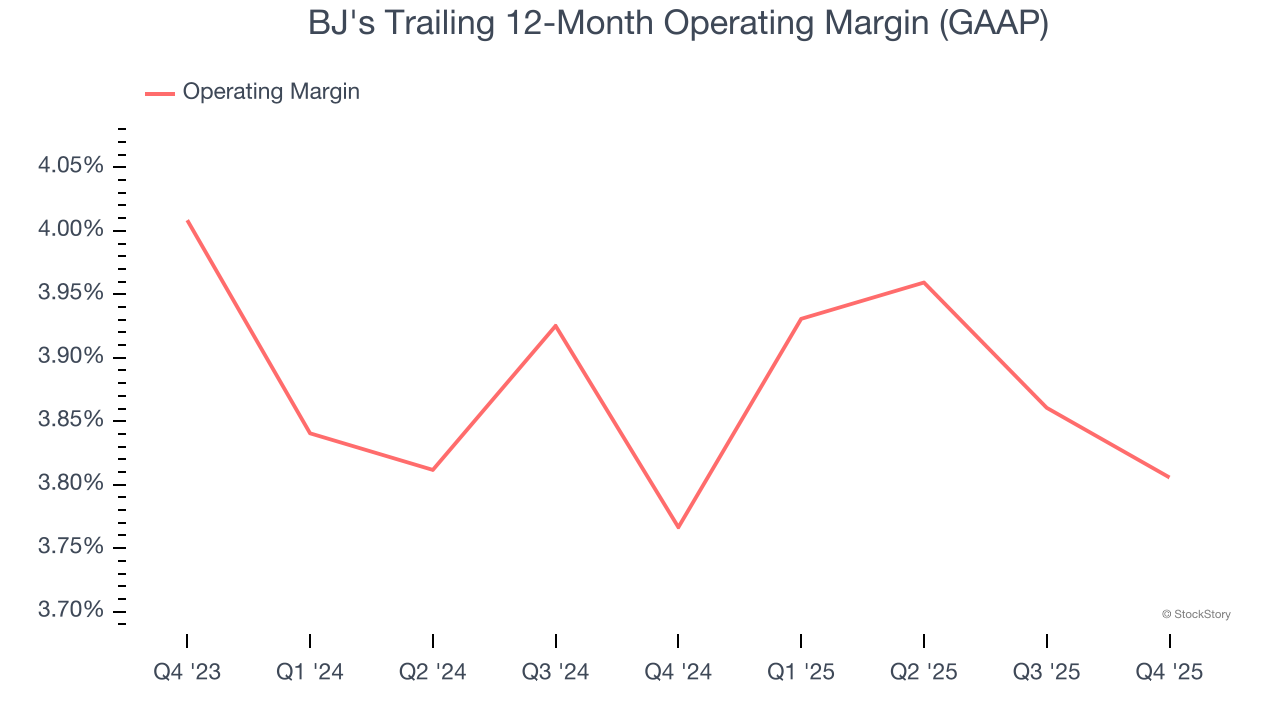

3. Weak Operating Margin Could Cause Trouble

Operating margin is an important measure of profitability for retailers as it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

BJ’s operating margin has more or less stayed the same over the last 12 months , averaging 3.8% over the last two years. This profitability was lousy for a consumer retail business and caused by its suboptimal cost structureand low gross margin.

Final Judgment

BJ's isn’t a terrible business, but it isn’t one of our picks. With its shares beating the market recently, the stock trades at 21.7× forward P/E (or $98.06 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Would Buy Instead of BJ's

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.