Although the S&P 500 is down 2.3% over the past six months, EPAM’s stock price has fallen further to $138.56, losing shareholders 9.1% of their capital. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for EPAM? Find out in our full research report, it’s free.

Why Does EPAM Spark Debate?

Founded in 1993 during the early days of offshore software development, EPAM Systems (NYSE: EPAM) provides digital engineering, cloud, and AI transformation services to help global enterprises and startups modernize their technology systems and create digital products.

Two Things to Like:

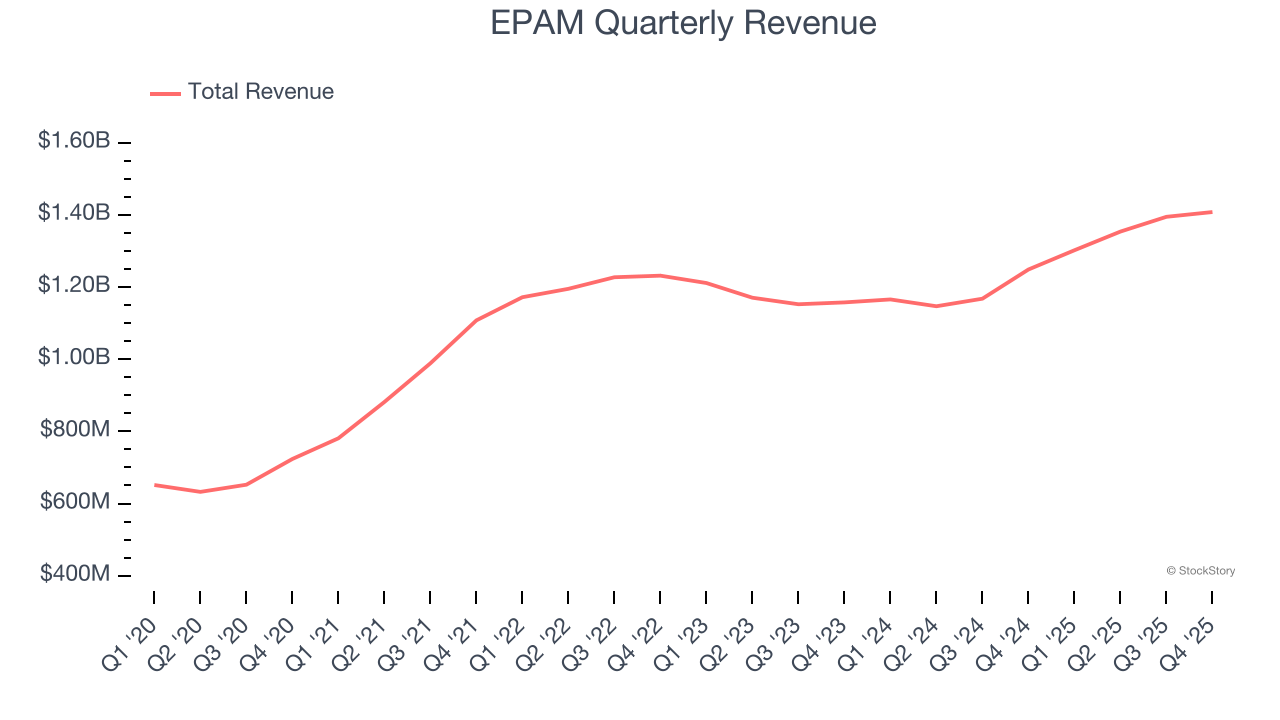

1. Skyrocketing Revenue Shows Strong Momentum

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, EPAM grew its sales at an incredible 15.5% compounded annual growth rate. Its growth surpassed the average business services company and shows its offerings resonate with customers.

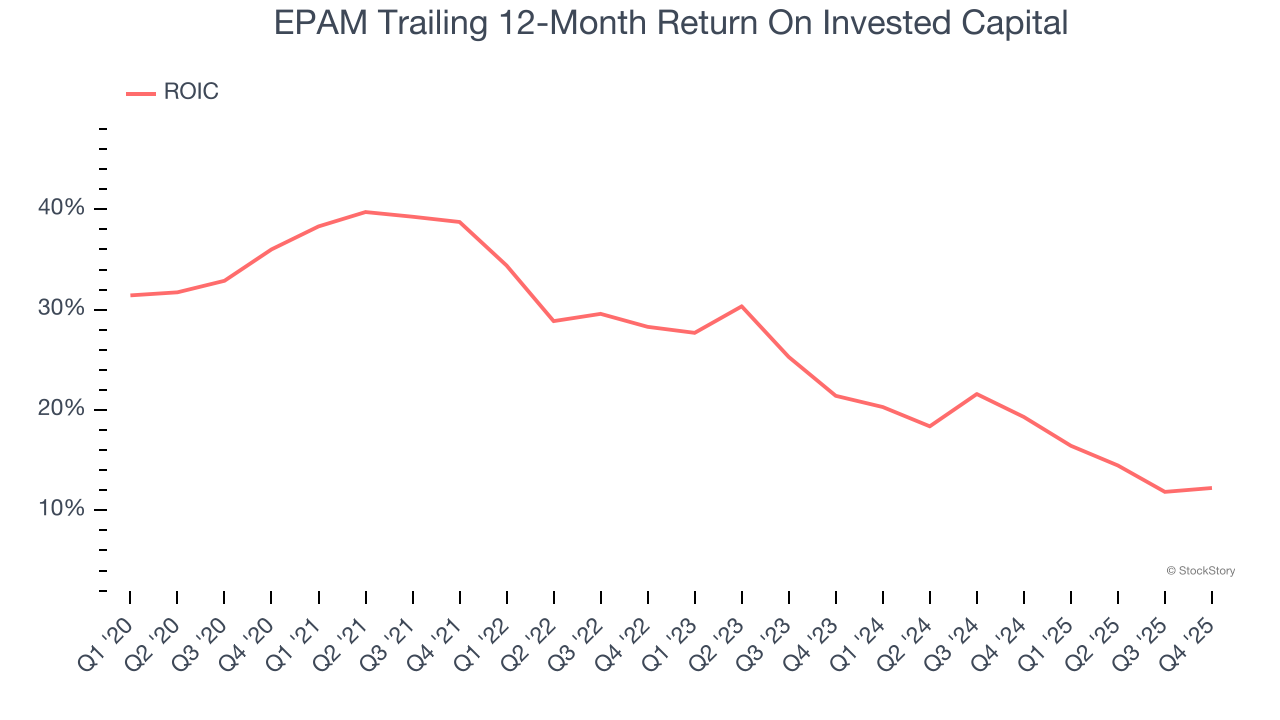

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

EPAM’s five-year average ROIC was 24%, placing it among the best business services companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

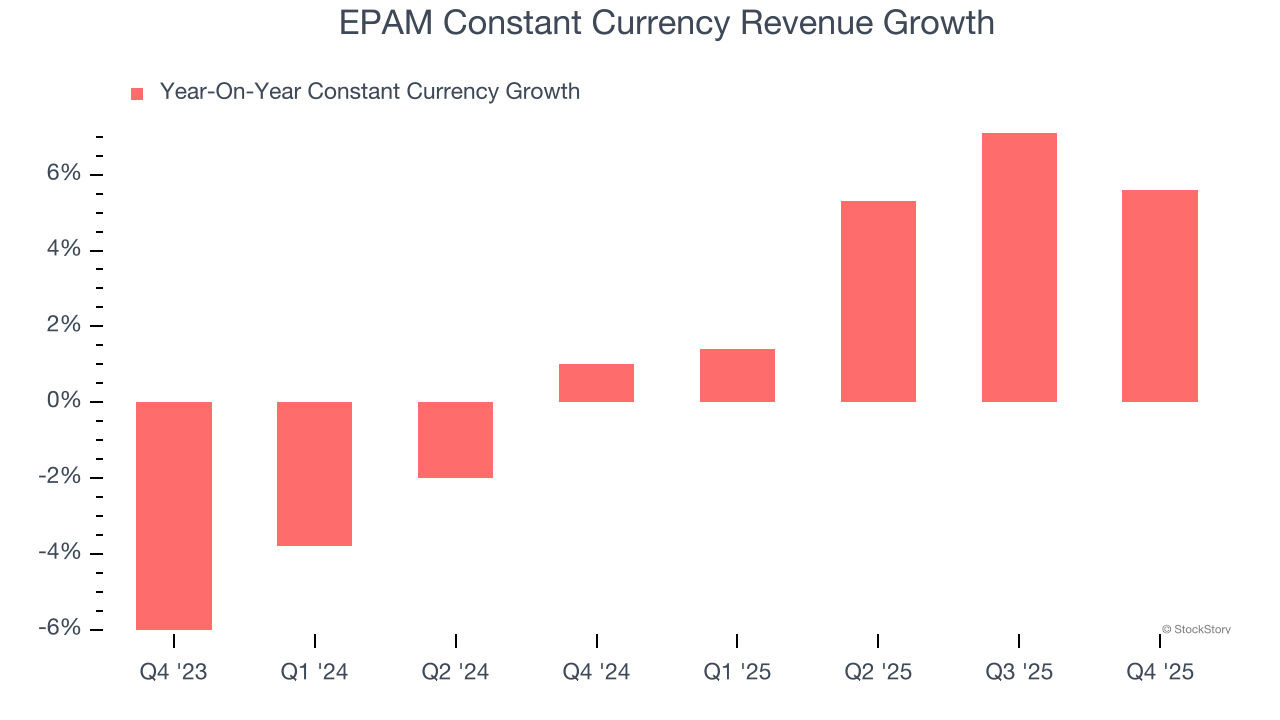

Weak Constant Currency Growth Points to Soft Demand

In addition to reported revenue, constant currency revenue is a useful data point for analyzing IT Services & Consulting companies. This metric excludes currency movements, which are outside of EPAM’s control and are not indicative of underlying demand.

Over the last two years, EPAM’s constant currency revenue averaged 2.1% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

Final Judgment

EPAM has huge potential even though it has some open questions. After the recent drawdown, the stock trades at 10.8× forward P/E (or $138.56 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than EPAM

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.