Looking back on medical devices & supplies - imaging, diagnostics stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Hologic (NASDAQ: HOLX) and its peers.

The medical devices and supplies industry, particularly those specializing in imaging and diagnostics, operates with a comparatively stable yet capital-intensive business model. Companies in this space benefit from consistent demand driven by the essential nature of diagnostic tools in patient care, as well as recurring revenue streams from consumables, service contracts, and equipment maintenance. However, the industry faces challenges such as significant upfront development costs, stringent regulatory requirements, and pricing pressures from hospitals and healthcare systems, which are increasingly focused on cost containment. Looking ahead, the industry should enjoy tailwinds from advancements in technology, including the integration of artificial intelligence to enhance diagnostic accuracy and workflow efficiency, as well as rising demand for imaging solutions driven by aging populations. On the other hand, headwinds could arise from a rethinking of healthcare costs potentially resulting in reimbursement cuts and slower capital equipment purchasing. Additionally, cybersecurity concerns surrounding connected medical devices could introduce new risks and complexities for manufacturers.

The 4 medical devices & supplies - imaging, diagnostics stocks we track reported a slower Q4. As a group, revenues beat analysts’ consensus estimates by 3.5%.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 13.5% since the latest earnings results.

Weakest Q4: Hologic (NASDAQ: HOLX)

As a pioneer in 3D mammography technology that has revolutionized breast cancer detection, Hologic (NASDAQ: HOLX) develops and manufactures diagnostic products, medical imaging systems, and surgical devices focused primarily on women's health and wellness.

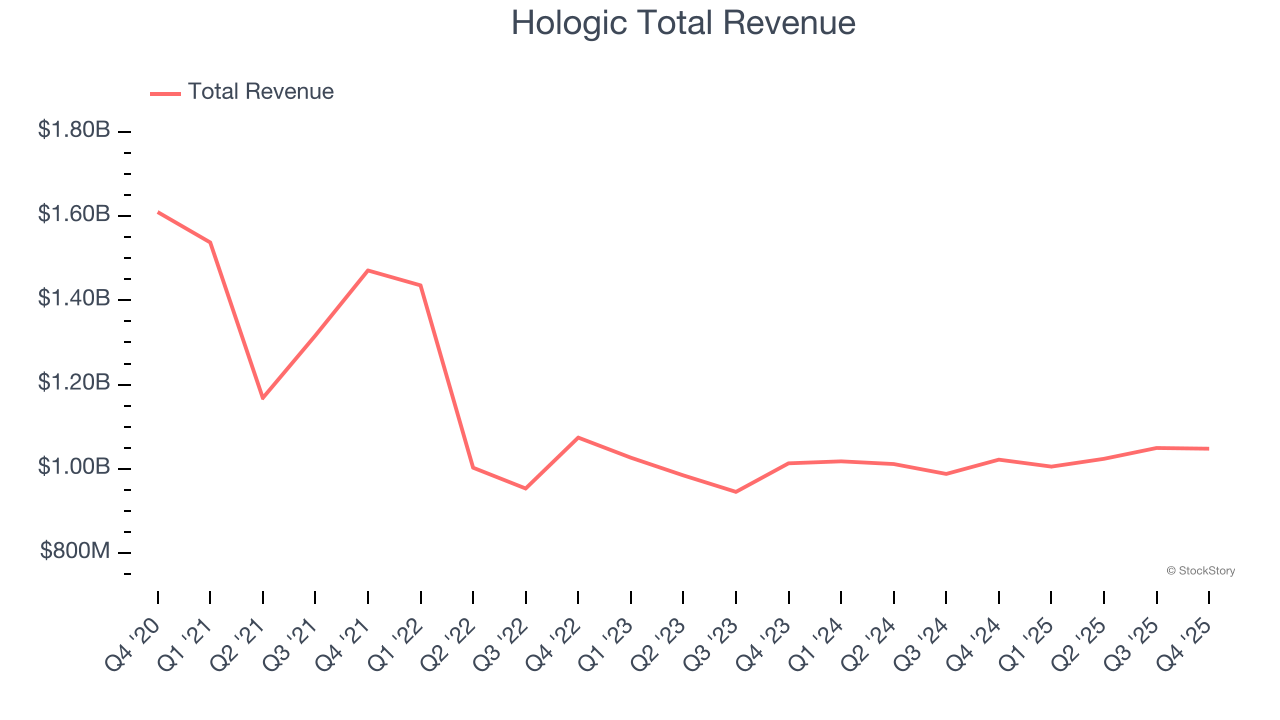

Hologic reported revenues of $1.05 billion, up 2.5% year on year. This print fell short of analysts’ expectations by 2.1%. Overall, it was a disappointing quarter for the company with a significant miss of analysts’ revenue and EPS estimates.

Hologic delivered the weakest performance against analyst estimates of the whole group. Interestingly, the stock is up 1.4% since reporting and currently trades at $76.05.

Read our full report on Hologic here, it’s free.

Best Q4: GE HealthCare (NASDAQ: GEHC)

Spun off from industrial giant General Electric in 2023 after over a century as its healthcare division, GE HealthCare (NASDAQ: GEHC) provides medical imaging equipment, patient monitoring systems, diagnostic pharmaceuticals, and AI-enabled healthcare solutions to hospitals and clinics worldwide.

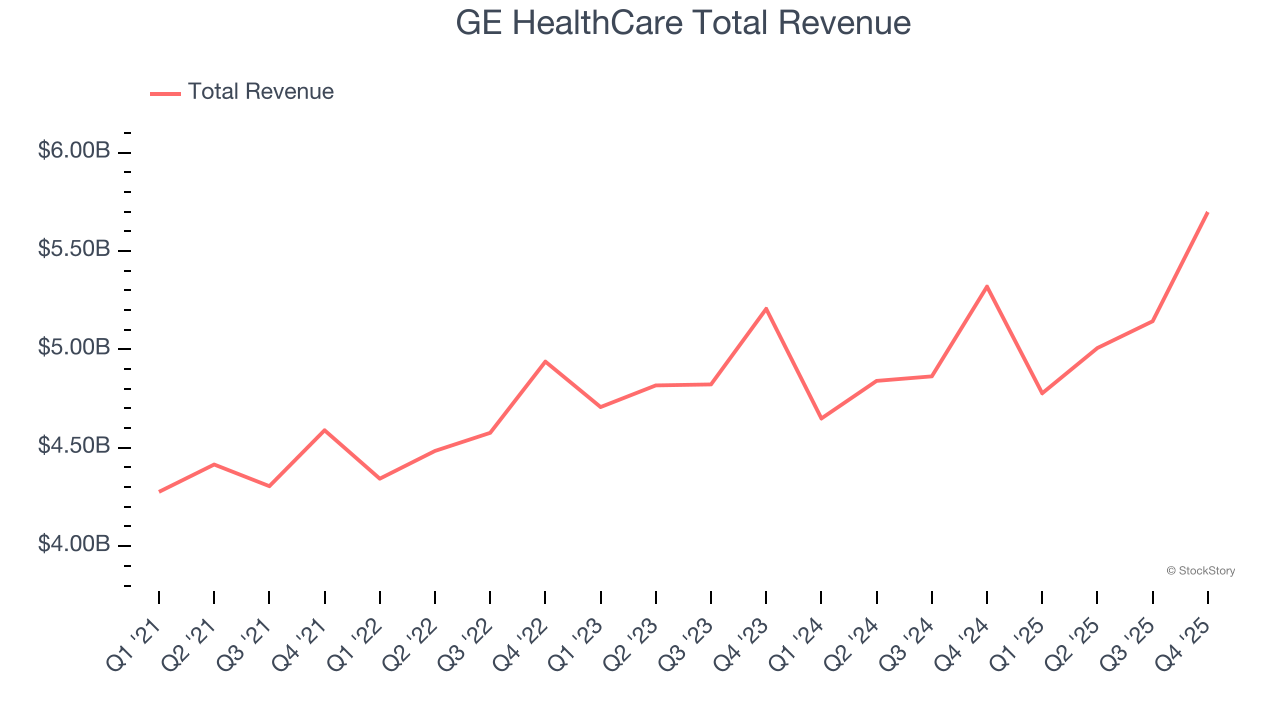

GE HealthCare reported revenues of $5.70 billion, up 7.1% year on year, outperforming analysts’ expectations by 1.7%. The business had a strong quarter with a solid beat of analysts’ full-year EPS guidance estimates and an impressive beat of analysts’ organic revenue estimates.

GE HealthCare achieved the fastest revenue growth among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 11.1% since reporting. It currently trades at $70.01.

Is now the time to buy GE HealthCare? Access our full analysis of the earnings results here, it’s free.

Lantheus (NASDAQ: LNTH)

Pioneering the "Find, Fight and Follow" approach to disease management, Lantheus Holdings (NASDAQGM:LNTH) develops and commercializes radiopharmaceuticals and other imaging agents that help healthcare professionals detect, diagnose, and treat diseases.

Lantheus reported revenues of $406.8 million, up 4% year on year, exceeding analysts’ expectations by 11%. Still, it was a slower quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and a significant miss of analysts’ full-year EPS guidance estimates.

Lantheus delivered the biggest analyst estimates beat but had the weakest full-year guidance update in the group. The stock is flat since the results and currently trades at $75.89.

Read our full analysis of Lantheus’s results here.

QuidelOrtho (NASDAQ: QDEL)

Born from the 2022 merger of Quidel and Ortho Clinical Diagnostics, QuidelOrtho (NASDAQ: QDEL) develops and manufactures diagnostic testing solutions for healthcare providers, from rapid point-of-care tests to complex laboratory instruments and systems.

QuidelOrtho reported revenues of $723.6 million, up 2.2% year on year. This result beat analysts’ expectations by 3.2%. Taking a step back, it was a mixed quarter as it also produced an impressive beat of analysts’ revenue estimates but a significant miss of analysts’ full-year EPS guidance estimates.

QuidelOrtho achieved the highest full-year guidance raise but had the slowest revenue growth among its peers. The stock is down 44.7% since reporting and currently trades at $15.94.

Read our full, actionable report on QuidelOrtho here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.