The United States energy market is reeling after a historic mid-winter "perfect storm" sent natural gas prices skyrocketing by more than 78% in the first weeks of 2026. This dramatic escalation, driven by a combination of record-breaking Arctic temperatures and structural supply constraints, has rippled through the broader economy, contributing to a 12% jump in the global energy price index. While prices at the Henry Hub have begun to retreat from their January peaks, the shock has reignited intense debates over the nation’s aging infrastructure and the growing demand for electricity fueled by the AI revolution.

For consumers and industrial users, the immediate implications are stark. Utility bills are expected to remain elevated through the spring as providers pass on the costs of emergency spot-market purchases made during the height of the freeze. Meanwhile, the financial sector has seen a surge in volatility, with energy-focused exchange-traded funds (ETFs) recording some of their most intense trading volumes in years. As of February 23, 2026, the market is stabilizing, but the scars of the "Winter Storm Fern" price spike have fundamentally altered the outlook for the year ahead.

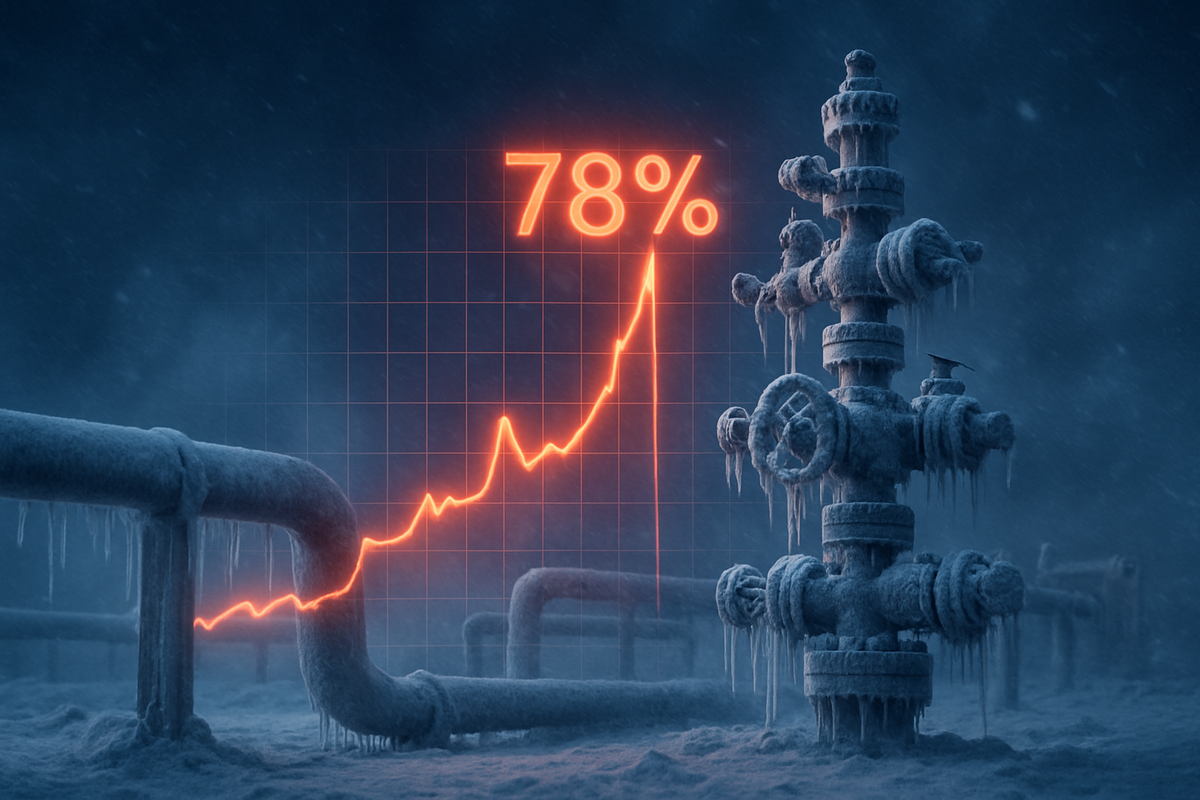

A Perfect Storm: Tracking the 78% Surge

The crisis began in mid-January 2026 when an atmospheric anomaly known as "Winter Storm Fern" descended upon the continental United States, bringing sub-zero temperatures as far south as the Gulf Coast. The extreme cold triggered widespread "wellhead freeze-offs," where water in the gas streams froze and physically blocked production. This effectively knocked offline an estimated 15% of total U.S. production—approximately 50 billion cubic feet per day (Bcf/d)—at the exact moment demand for heating was reaching its seasonal zenith.

Benchmark Henry Hub futures, which had averaged around $4.25/MMBtu in December, vaulted to a peak of approximately $7.58/MMBtu, representing a staggering 78.4% increase. The supply-demand imbalance was so severe that it led to the largest weekly storage withdrawal in U.S. history, with nearly 370 billion cubic feet (Bcf) pulled from underground reserves in a single seven-day period. By early February, national inventories had plummeted to 5.6% below the five-year average, leaving the market with almost no margin for error.

Initial reactions from the industry were a mixture of alarm and logistical maneuvering. Regional hubs in the Northeast saw spot prices briefly touch $30/MMBtu as infrastructure reached its physical limits. The Mountain Valley Pipeline, operated by EQT Corporation (NYSE: EQT), reportedly ran at 6% above its 2 Bcf/d nameplate capacity to prevent regional blackouts. This desperate scramble for supply highlighted a critical vulnerability: despite record production levels in recent years, the U.S. lacks the "midstream" pipeline capacity to move gas efficiently during extreme weather events.

Corporate Winners and Losers in the Volatility

The sudden price surge created a polarized landscape for public companies and investment vehicles. EQT Corporation (NYSE: EQT), the largest natural gas producer in the country, emerged as a primary beneficiary for its unhedged production. However, the company’s leadership has been vocal about the risks of such volatility, with CEO Toby Rice using the event to lobby for urgent permitting reform. EQT has since pivoted its strategy, increasing its 2026 price hedges from 7% to 25% to insulate the company from future price collapses now that the spike has passed.

In the midstream and export sector, Cheniere Energy (NYSE: LNG) maintained a steady course, though the domestic price spike briefly complicated the economics of liquefied natural gas (LNG) exports. While Cheniere benefits from long-term contracts, the surge in domestic prices narrowed the "arbitrage" window between U.S. and European benchmarks, reminding investors that the U.S. is no longer an isolated energy island. Other major players, such as ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX), saw modest gains in their upstream divisions, though these were partially offset by the increased costs of running their massive petrochemical and refining operations.

For retail investors, the volatility was most visible in specialized ETFs. The United States Natural Gas Fund (NYSE Arca: UNG) saw a 50% rise during the January squeeze, while the leveraged ProShares Ultra Bloomberg Natural Gas (NYSE Arca: BOIL) nearly doubled in value in less than two weeks. However, these gains proved fleeting; as weather forecasts turned warmer in mid-February, BOIL plummeted, losing over 16% in a single session on February 2. This serves as a cautionary tale for those using leveraged instruments to play short-term commodity cycles.

Broader Significance and the AI Factor

This event marks a significant departure from historical precedents due to the emergence of a new "baseload" demand driver: AI data centers. Unlike traditional residential heating, which is seasonal, the massive power requirements of 2026-era artificial intelligence facilities provide a constant, year-round pull on natural gas-fired electricity. This "floor" under demand means that when a seasonal spike like Winter Storm Fern hits, the system is already under more strain than it was a decade ago.

The 12% rise in the overall energy price index has also complicated the Federal Reserve's battle against inflation. While the U.S. Labor Department reported that falling gasoline prices helped offset some of the gas spike, the "pass-through" effect on electricity costs is expected to hit consumer wallets for months. This has led to renewed calls from the Department of Energy for a balanced energy mix, as the reliability of the gas grid faces scrutiny from both environmental advocates and industrial hawks.

Regulatory implications are already beginning to surface. The Federal Energy Regulatory Commission (FERC) has indicated it will launch an inquiry into the "wellhead freeze-offs" in the Permian and Haynesville basins, potentially mandating stricter winterization standards for gas producers—similar to those imposed on Texas power plants following previous winter disasters. This could lead to higher capital expenditure requirements for producers moving forward, potentially squeezing margins even if prices remain high.

The Path Forward: Stability or a New Normal?

As we move toward the spring of 2026, the immediate outlook is one of stabilization. Prices have settled back into the $3.00–$3.25 range, thanks to a revised NOAA forecast predicting a warmer-than-average end to the winter. However, the market is now on high alert for the summer cooling season. If the "AI demand" continues to grow at its current pace, any summer heatwave could trigger a secondary price spike, as gas-fired power plants struggle to meet the dual demand of air conditioning and data processing.

Strategic pivots are already underway. Utilities are increasingly looking to accelerate battery storage deployments to shave off the peak demand that forces them into the expensive spot market. For gas producers, the focus is shifting toward "reliability as a premium." Companies that can prove their infrastructure is resilient to extreme cold are likely to secure more favorable long-term contracts from power providers who were burned by the January volatility.

Market Wrap-Up and Investor Outlook

The 78% spike in early 2026 has served as a wake-up call for a market that had become complacent about supply abundance. The key takeaway for investors is that while the U.S. remains the world’s leading producer of natural gas, infrastructure bottlenecks and new structural demand from the tech sector have introduced a new era of "tail-risk" volatility. The 12% jump in the energy index serves as a reminder that natural gas remains the linchpin of the global energy transition, for better or worse.

Moving forward, the market will be characterized by a "wait and see" approach regarding infrastructure legislation. Investors should keep a close eye on the progress of the Mountain Valley Pipeline expansions and any new LNG export terminal approvals. In the coming months, the focus will shift from winter heating to the summer cooling "burn," where the resilience of the grid will be tested once again. For now, the "Winter of '26" stands as a testament to the enduring power of the commodity markets to surprise even the most seasoned analysts.

This content is intended for informational purposes only and is not financial advice.