Specialized talent solutions company Robert Half (NYSE: RHI) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 8.4% year on year to $1.35 billion. Its GAAP profit of $0.17 per share was 52.9% below analysts’ consensus estimates.

Is now the time to buy Robert Half? Find out by accessing our full research report, it’s free.

Robert Half (RHI) Q1 CY2025 Highlights:

- Revenue: $1.35 billion vs analyst estimates of $1.41 billion (8.4% year-on-year decline, 4.3% miss)

- EPS (GAAP): $0.17 vs analyst expectations of $0.36 (52.9% miss)

- Adjusted EBITDA: $51.89 million vs analyst estimates of $65.39 million (3.8% margin, 20.6% miss)

- Operating Margin: 2.9%, in line with the same quarter last year

- Market Capitalization: $4.64 billion

Company Overview

With roots dating back to 1948 as the first specialized recruiting firm for accounting and finance professionals, Robert Half (NYSE: RHI) provides specialized talent solutions and business consulting services, connecting skilled professionals with companies across various fields.

Professional Staffing & HR Solutions

The Professional Staffing & HR Solutions subsector within Business Services is set to benefit from evolving workforce trends, including the rise of remote work and the gig economy. With companies casting a wider net to find talent due to remote work, the expertise of staffing and recruiting companies is even more valuable. For those who invest wisely, the use of predictive AI in recruitment and screening as well as automation in HR workflows can enhance efficiency and scalability. On the other hand, digitization means that talent discovery is less of a manual process, opening the door for tech-first platforms. Additionally, regulatory scrutiny around data privacy in HR is evolving and may require companies in this sector to change their go-to-market strategies over time.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

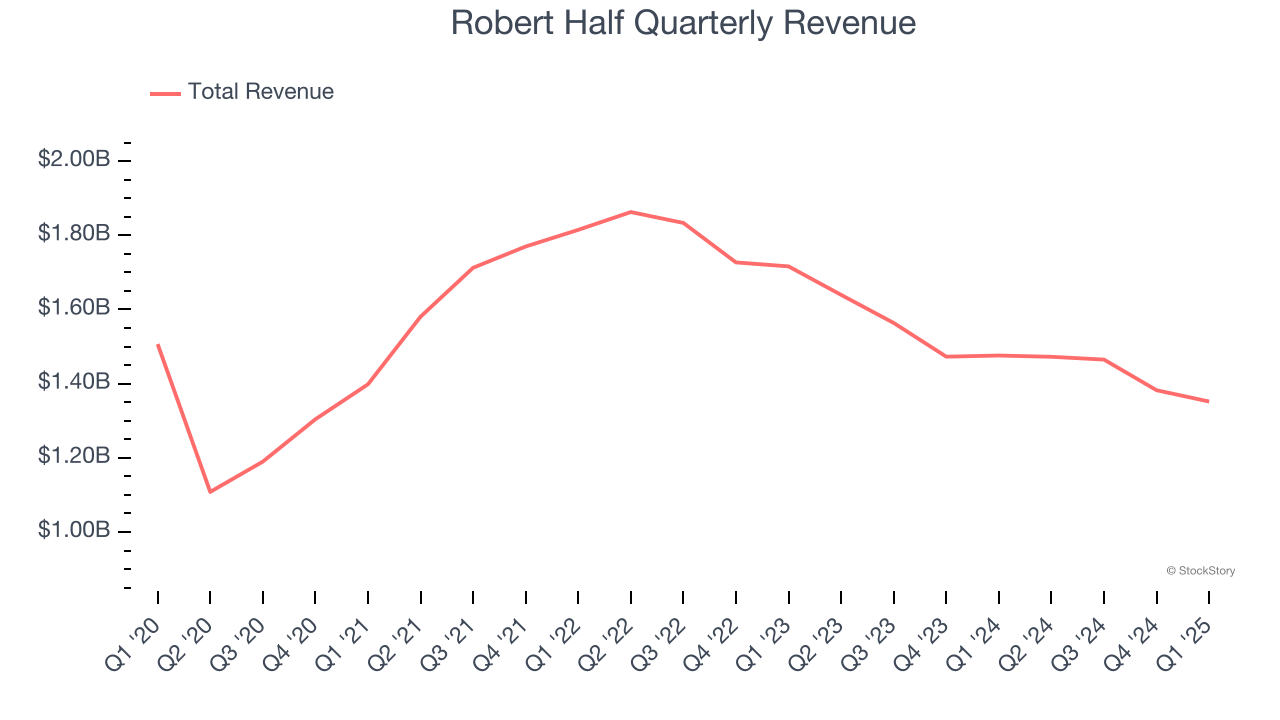

With $5.67 billion in revenue over the past 12 months, Robert Half is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when you’ve penetrated most of the market. For Robert Half to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

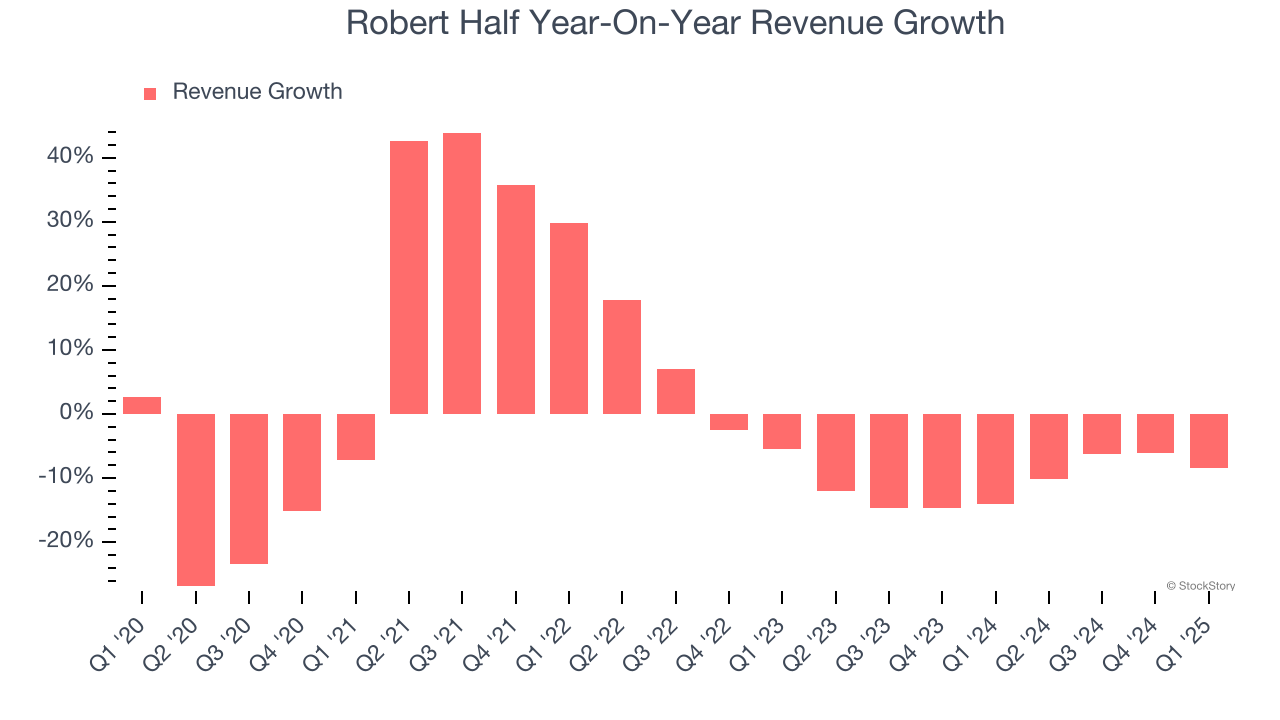

As you can see below, Robert Half’s revenue declined by 1.5% per year over the last five years, a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Robert Half’s recent performance shows its demand remained suppressed as its revenue has declined by 10.9% annually over the last two years.

This quarter, Robert Half missed Wall Street’s estimates and reported a rather uninspiring 8.4% year-on-year revenue decline, generating $1.35 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

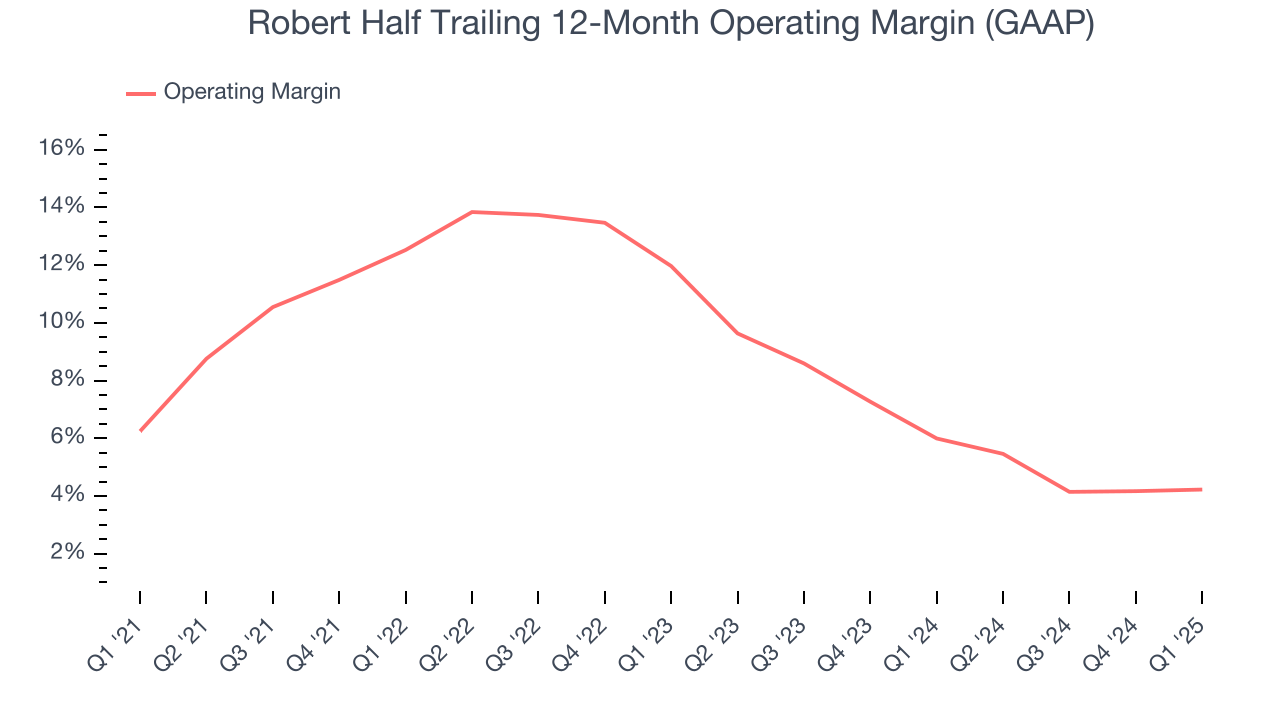

Robert Half was profitable over the last five years but held back by its large cost base. Its average operating margin of 8.5% was weak for a business services business.

Looking at the trend in its profitability, Robert Half’s operating margin decreased by 2 percentage points over the last five years. Robert Half’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q1, Robert Half generated an operating profit margin of 2.9%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

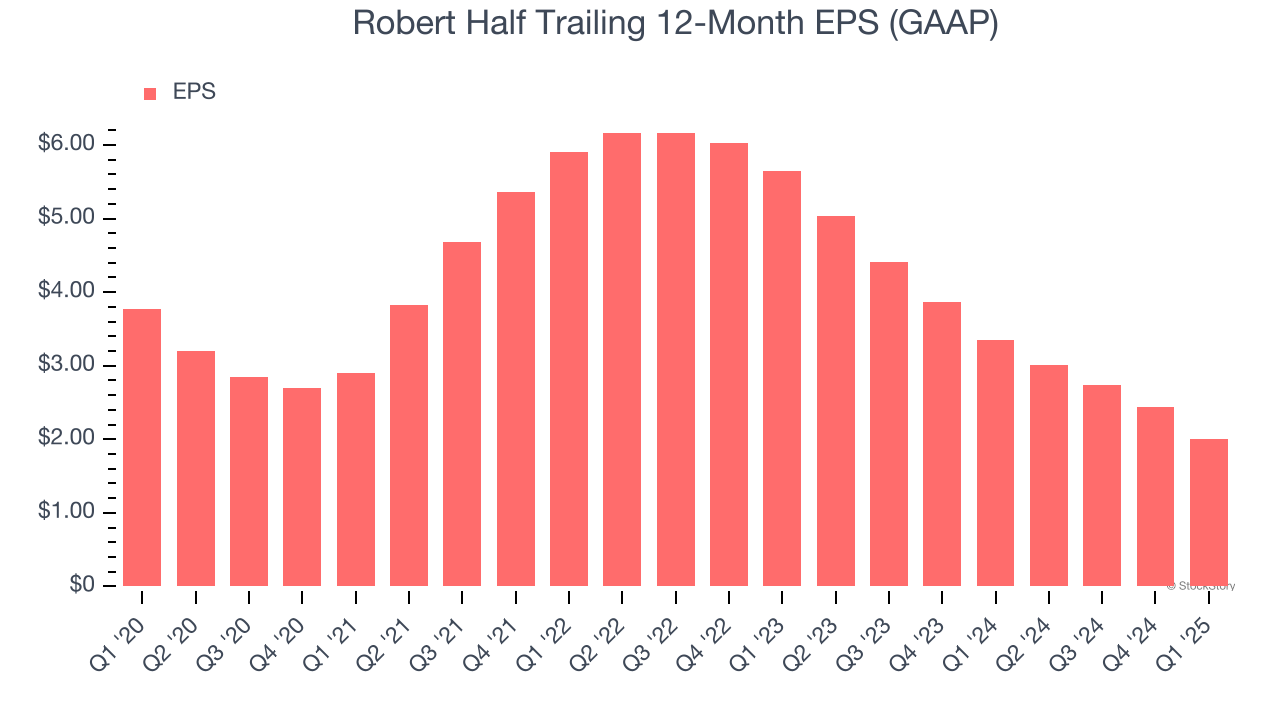

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Robert Half, its EPS declined by 11.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Robert Half’s earnings can give us a better understanding of its performance. As we mentioned earlier, Robert Half’s operating margin was flat this quarter but declined by 2 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Robert Half reported EPS at $0.17, down from $0.61 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Robert Half’s full-year EPS of $2.00 to grow 31.3%.

Key Takeaways from Robert Half’s Q1 Results

We struggled to find many positives in these results as its revenue,EPS, and EBITDA missed significantly. Overall, this was a weaker quarter. The stock traded down 10% to $41.80 immediately after reporting.

Robert Half’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.