RadNet has gotten torched over the last six months - since December 2025, its stock price has dropped 30.5% to $52.97 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy RadNet, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is RadNet Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons you should be careful with RDNT, plus one stock we’d rather own.

1. Fewer Distribution Channels than Larger Competitors

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $2.14 billion in revenue over the past 12 months, RadNet lacks scale in an industry where it matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

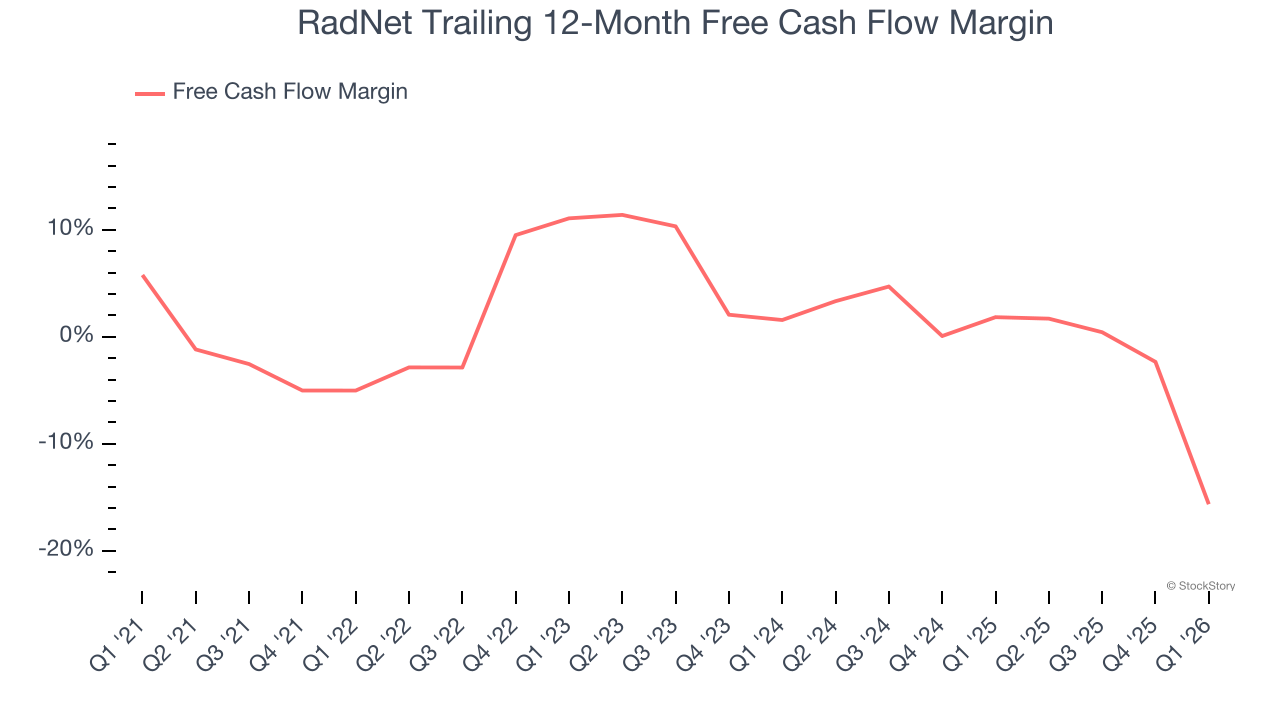

2. Free Cash Flow Margin Dropping

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, RadNet’s margin dropped by 10.6 percentage points over the last five years. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business. RadNet’s free cash flow margin for the trailing 12 months was negative 15.7%.

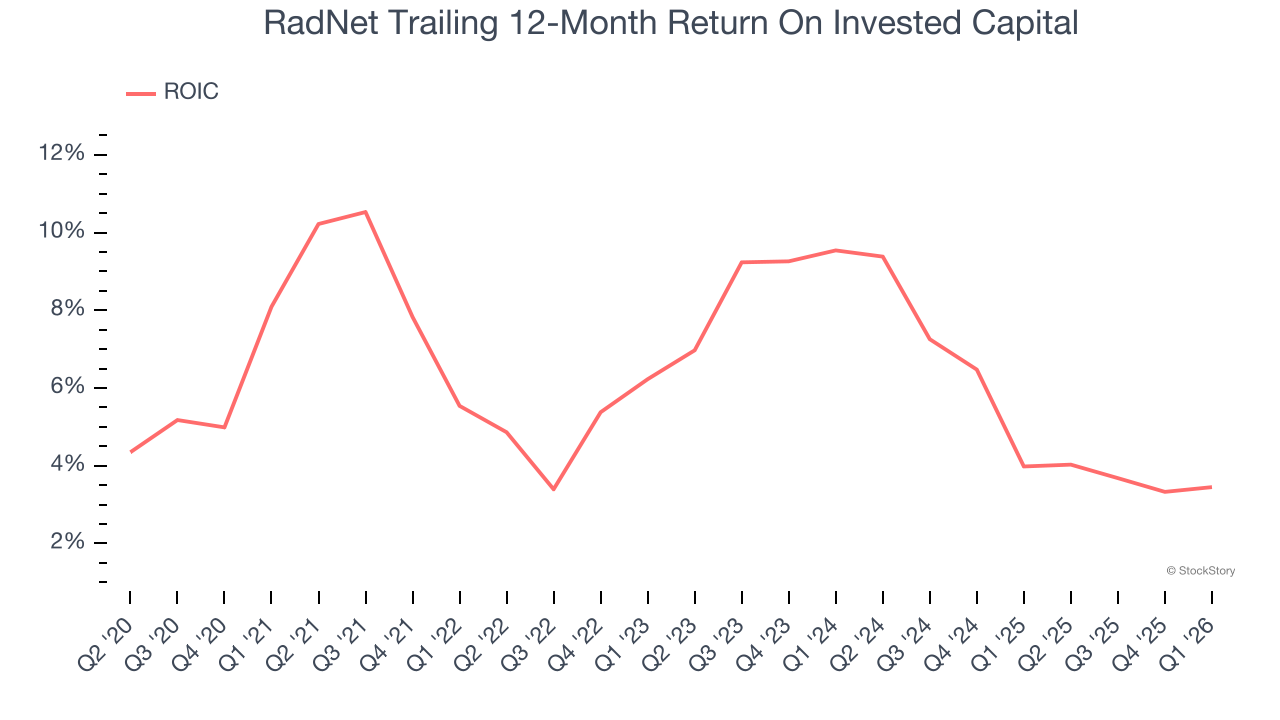

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

RadNet historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.7%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

Final Judgment

RadNet isn’t a terrible business, but it isn’t one of our picks. Following the recent decline, the stock trades at 72.3× forward P/E (or $52.97 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.