Exton, Pennsylvania-based West Pharmaceutical Services, Inc. (WST) designs, manufactures, and sells containment and delivery systems for injectable drugs and healthcare products. Valued at $17.9 billion by market cap, the company’s technologies include the design and manufacture of packaging components, research and development of drug delivery systems, and contract laboratory services and other services.

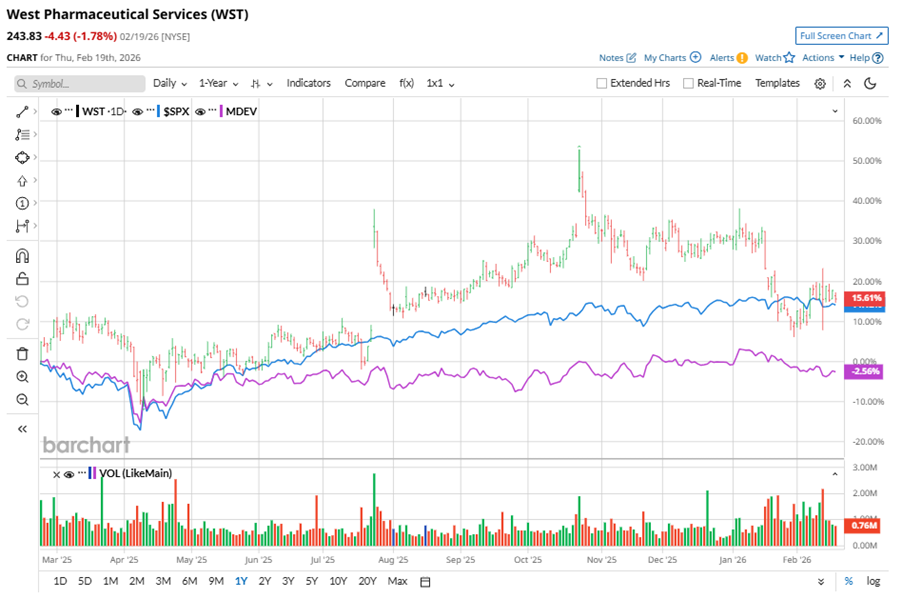

Shares of this leading manufacturer of containment and delivery systems have outperformed the broader market over the past year. WST has gained 20.4% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 11.7%. However, in 2026, WST’s stock fell 11.4%, compared to the SPX’s marginal rise on a YTD basis.

Zooming in further, WST’s outperformance is also apparent compared to the First Trust Indxx Global Medical Devices ETF (MDEV). The exchange-traded fund has declined 2.9% over the past year. However, the ETF’s 1.8% dip on a YTD basis outshines WST’s low double-digit losses over the same time frame.

WST’s outperformance was driven by strong demand for high-value products, especially biologics and GLP-1 therapies. Favorable product mix and capacity investments in European sites boosted margins, offsetting R&D and compensation costs. New product launches, like the Synchrony prefillable syringe system, also contributed to growth.

On Feb. 12, WST shares closed down more than 1% after reporting its Q4 results. Its adjusted EPS of $2.04 topped Wall Street expectations of $1.83. The company’s revenue was $805 million, exceeding Wall Street forecasts of $794.3 million. WST expects full-year adjusted EPS in the range of $7.85 to $8.20, and revenue in the range of $3.2 billion to $3.3 billion.

For fiscal 2026, ending in December, analysts expect WST’s EPS to grow 10% to $8.02 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

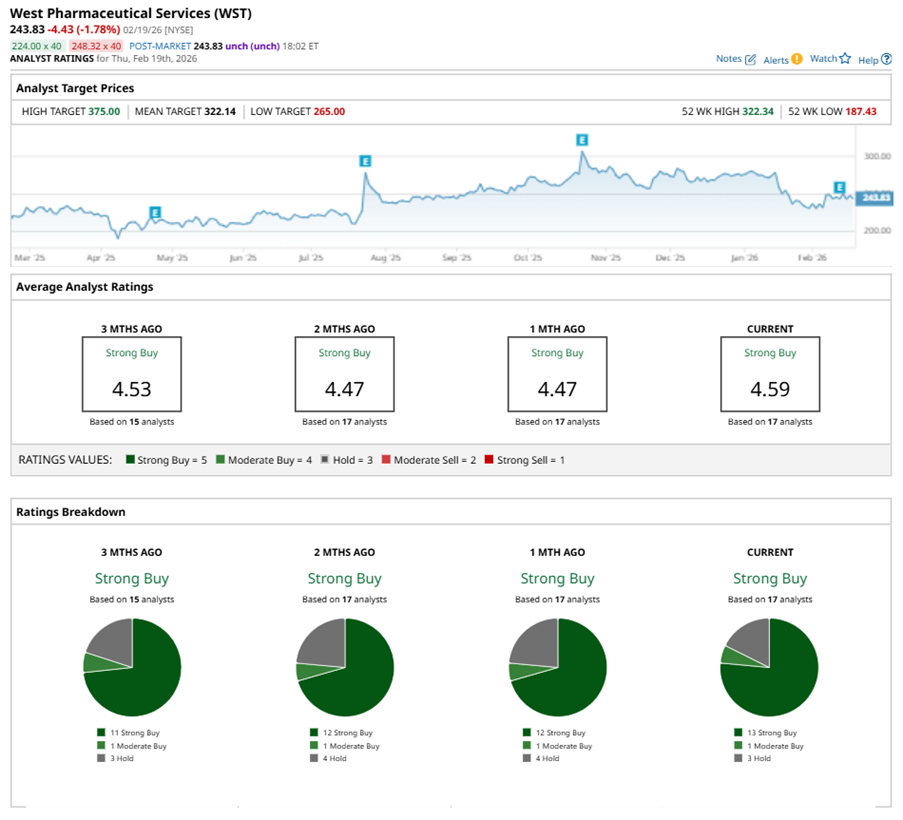

Among the 17 analysts covering WST stock, the consensus is a “Strong Buy.” That’s based on 13 “Strong Buy” ratings, one “Moderate Buy,” and three “Holds.”

This configuration is more bullish than a month ago, with 12 analysts recommending a “Strong Buy.”

On Feb. 17, Kallum Titchmarsh from Morgan Stanley (MS) maintained a “Hold” rating on WST with a price target of $285, implying a potential upside of 16.9% from current levels.

The mean price target of $322.14 represents a 32.1% premium to WST’s current price levels. The Street-high price target of $375 suggests a notable upside potential of 53.8%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Down 24% in 2026, Where Is Palantir Stock Headed Next and Should You Buy PLTR Here?

- As Meta and Nvidia Announce a Huge, Multi-Year Partnership, Which Is the Better Stock to Buy?

- Palo Alto Networks Stock Has Tanked But Its Free Cash Flow is Strong - Time to Buy PANW?

- 1 Analyst Thinks This Stock is The "Godfather of AI"