In the last quarter, NVIDIA Corporation (NVDA) executed a notable portfolio shift by fully divesting its stake in Arm Holdings plc (ARM), the semiconductor design firm whose architecture underpins billions of devices worldwide.

According to Nvidia’s latest 13F regulatory filing, the company sold its remaining 1.1 million Arm shares, netting roughly $140 million and completely exiting its position by the end of the fourth quarter of 2025. This move closes a long-running chapter that began with Nvidia’s attempted $40 billion acquisition of Arm in 2020, a deal that ultimately collapsed under regulatory scrutiny and competitive pushback.

Does this signal a lack of confidence from one of the industry’s most prominent tech companies, or is the pullback in ARM stock now a contrarian buying opportunity?

About Arm Holdings Stock

Arm Holdings is a semiconductor and software design company best known for developing the ARM architecture, a family of energy-efficient CPU designs widely licensed across the technology industry. Headquartered in the United Kingdom, Arm doesn’t manufacture physical chips itself but instead generates revenue by licensing its processor designs and related intellectual property to semiconductor companies and original equipment manufacturers, while also earning royalties on chips shipped by its partners. Arm went public on the NASDAQ in September 2023, and its current market cap stands at $132.7 billion.

Over the past 52 weeks, ARM has nudged into a softer performance profile, with the stock down 16.75% after earlier strength proved difficult to sustain amid investor concerns about near-term demand, higher memory prices affecting markets and competitive pressures. The stock had registered a high of $183.16 in October 2025, but is down by 31% from that peak.

In contrast to the 12-month slide, ARM has posted a 14.88% year-to-date (YTD) gain, reflecting renewed optimism and resilience. The positive returns have been supported by a rebound in broader tech sentiment and continued enthusiasm around Arm’s long-term positioning in AI-driven computing.

Adding to the gains was the Q3 earnings release on Feb. 4, in which Arm reported revenue and earnings that beat expectations. Shares initially sold off due to investor caution, only to rebound in the subsequent sessions with the stock climbing as much as 5.7% on Feb. 5 and 11.6% on Feb. 6, on renewed focus on strong royalty expansion that underpins its longer-term growth trajectory.

The stock is trading at a significant premium compared to industry peers at 149.33 times forward earnings.

Robust Top Line Performance

Arm Holdings reported its third-quarter fiscal 2026 results on Feb. 4 and delivered solid year-over-year (YOY) growth across its core business segments.

The company posted total revenue of a record $1.2 billion, up about 26% YOY, driven by strong demand across its royalty and licensing streams as next-generation Armv9 architecture adoption and growth in data-center and AI-oriented designs boosted per-unit royalty rates and broadened customer engagement. Royalty revenue alone rose roughly 27% YOY to a record of $737 million, while licensing and other revenue climbed about 25% YOY to about $505 million, reflecting an expanding pipeline of high-value deals.

Moreover, non-GAAP operating income expanded by about 14% YOY to roughly $505 million, and non-GAAP EPS rose near 10% to $0.43, beating the consensus estimate.

For the fourth quarter of fiscal 2026, management guided to revenue of approximately $1.47 billion plus or minus $50 million, and non-GAAP EPS of about $0.58 plus or minus $0.04.

Analysts predict EPS to be around $0.85 for fiscal 2026, a decline of around 19.8% YOY, but again rise 40% to $1.19 in fiscal 2027.

What Do Analysts Expect for Arm Stock?

Earlier this month, KeyBanc cut its price target on Arm Holdings to $170 from $200 but maintained an “Overweight” rating. While the data center segment is expanding and expected to become a larger royalty contributor over time, KeyBanc flagged risks from memory pricing pressures and potential handset unit declines, even as management expects only a limited impact on royalties.

Also, RBC Capital lowered its price target on ARM to $130 from $140 while maintaining an “Outperform” rating.

On the other hand, last month, BofA downgraded ARM to “Neutral” from “Buy,” citing near-term smartphone unit headwinds.

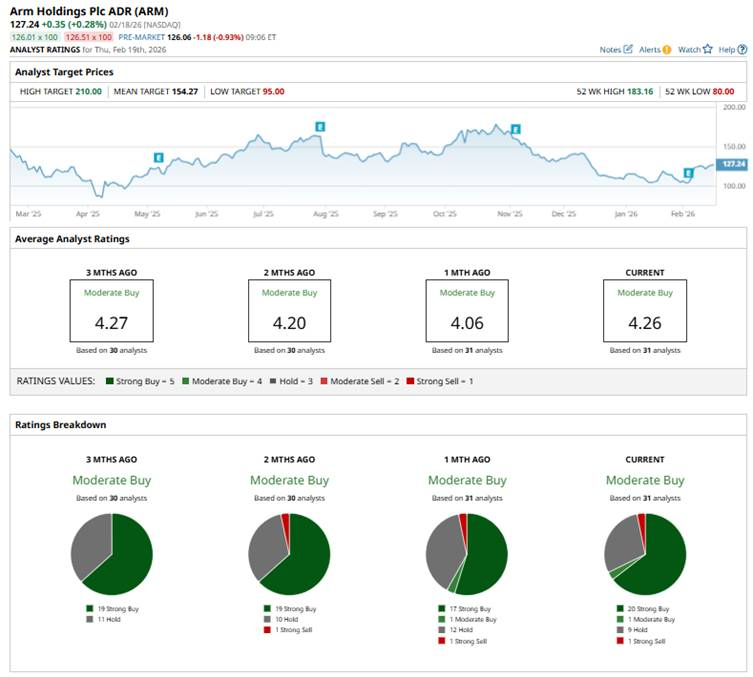

The stock has a consensus “Moderate Buy” rating overall. Out of 31 analysts covering the stock, 20 recommend a “Strong Buy,” one gives a “Moderate Buy,” nine analysts stay cautious with a “Hold” rating, and one has a “Strong Sell” rating.

ARM’s average analyst price target of $154.27 indicates a 21.2% upside potential, while the Street-high target price of $210 suggests 65% upside ahead.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- RingCentral Stock Soared on Friday. Is There More Room for RNG to Run?

- This AI Stock is Beating The Market and Could Keep Climbing in 2026

- Should You Buy Meta Platforms Stock Before Its New Smartwatch Comes Out This Year?

- Stanley Druckenmiller Just Exited Sandisk Stock. Should You Buy SNDK After Its Blowout Earnings?