There are several major “outside markets” that can and do have a daily, and sometimes significant, impact on the price movements of gold (GCM26) and silver (SIK26). These markets include global stock indexes, the U.S. dollar index ($DXY), crude oil (CLM26), and U.S. Treasuries. Importantly, the outside markets’ impact on the two precious metals is not static. Let’s look at the key outside markets and their present daily price impacts on gold and silver.

Rising U.S. Stock Indexes Also Bullish for Safe-Haven Metals. What Gives?

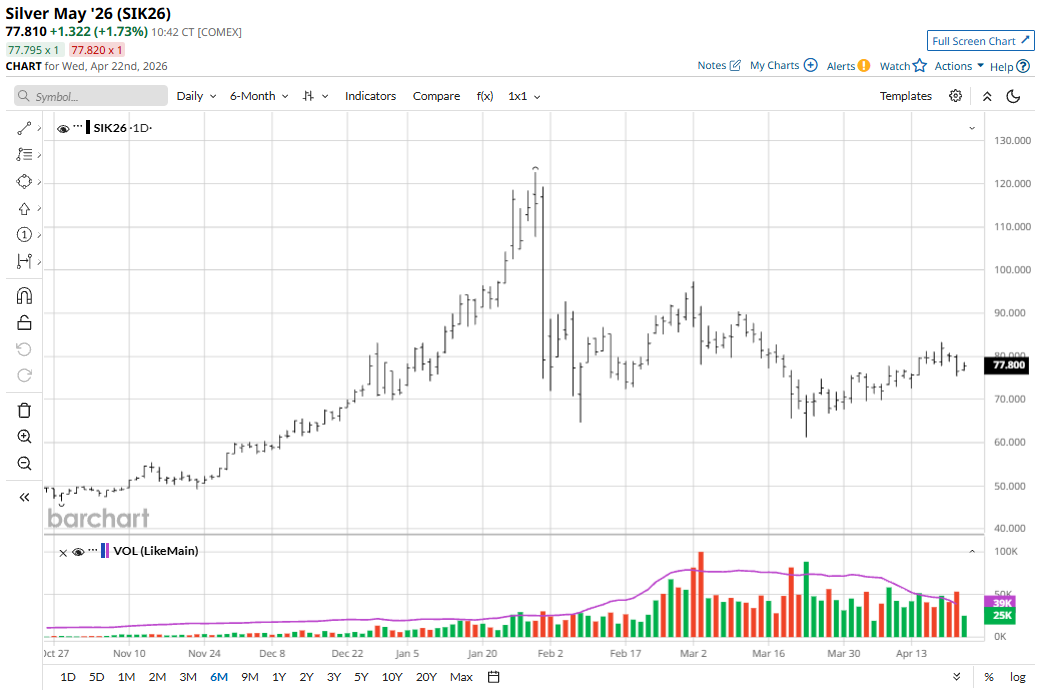

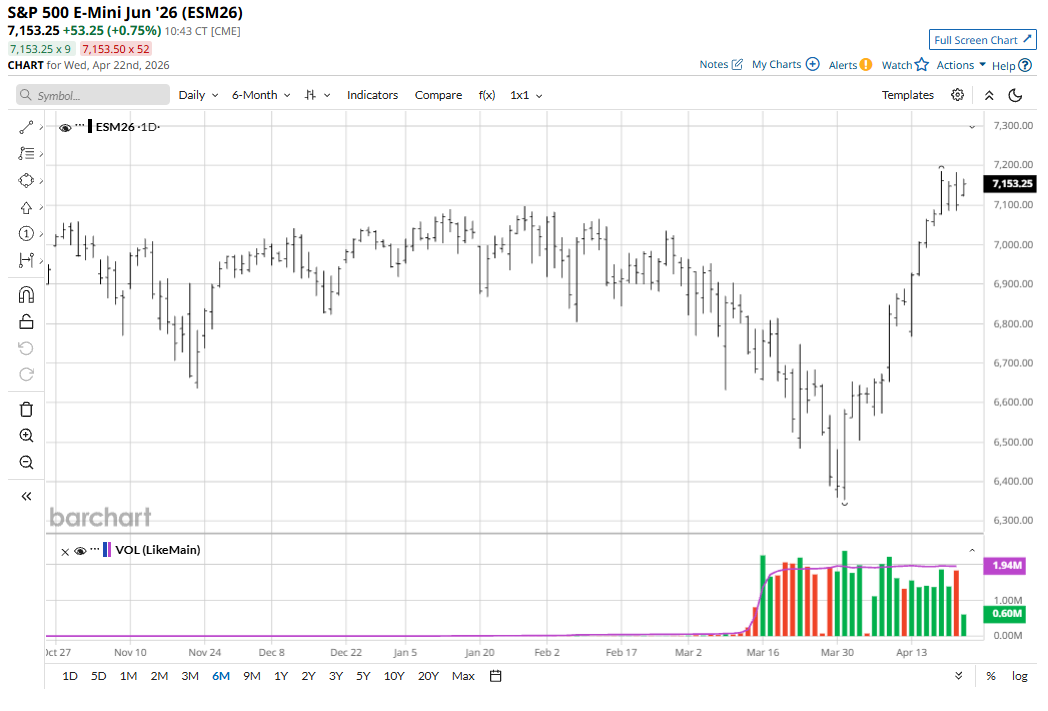

The past few weeks have highlighted a market correlation that has surprised even veteran traders and market watchers: risk-on stock indexes and risk-off gold and silver are rallying at the same time and selling off at the same time.

History and logic would dictate safe-haven gold and silver prices appreciating on trading days when the stock market is under selling pressure due to keener risk aversion in the general marketplace. And history and logic would dictate gold and silver selling off amid risk-on days when the stock market is posting good gains. Nope. Not in today’s trading environment. There is no doubt traders are fickle, and when traders are fickle, markets can seem illogical.

There is no single, absolute reason why gold and silver and the stock indexes have been more closely (but not always) tracking each other lately.

However, my interpretation of the phenomenon is that metals traders are at present more concerned about tighter monetary policies from the major central banks, including the associated inflation risks, choking off consumer and commercial global demand for metals. Such a scenario also would be bullish for the U.S. dollar. An appreciating greenback is historically bearish for gold and silver.

Metals traders, at present, appear to be less concerned about rallying risk asset prices (stocks) taking away investment demand from safe-haven gold and silver. It can also be argued that rallying stocks imply easier central bank monetary policies and lower interest rates. (Implying better global demand for metals).

Does the Rising Tide of Big Gains in Crude Oil Prices Lift All Raw Commodity Boats?

Crude oil is arguably the leader of the raw commodity sector. It’s the most fungible commodity market. Price history shows that when oil rallies, many other commodity markets also see better buying interest. That’s still the case nowadays — except when it isn’t. The past few weeks, gold and silver have on certain days seen their prices sell off on days when crude oil prices are higher and even solidly up. On those days, the metals traders reckon sharply rising crude oil prices mean higher gasoline prices at the pump, which in turn will hurt economies and constrain demand for metals.

However, gold and silver prices in recent weeks have rallied on the same days crude oil prices have posted good gains. Remember, traders are fickle. Trying to figure out what fundamental elements traders will deem most important on any given day seems to be a fool’s errand. I’m still of the opinion that higher crude oil prices are and will be overall bullish for most raw commodity markets, including precious metals.

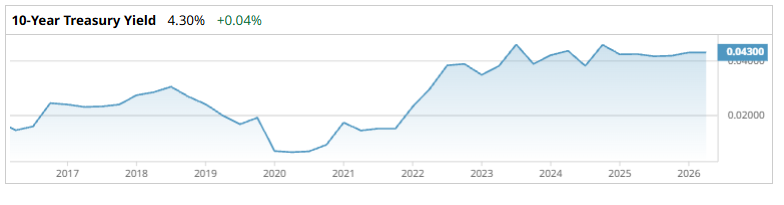

Rising Bond Yields Still Bearish for Gold, Silver

Gold and silver carry no dividends, cannot be discounted in price for a guaranteed higher payment later, nor do they provide any coupon rate payment. Bonds do.

When bond yields rise, it makes them more attractive for investors. That’s a bearish element for gold and silver from a competing asset class perspective. Rising bond yields mean expected higher interest rates, too. Higher interest rate limit demand for commodities. Rising U.S. Treasury yields suggest a stronger U.S. dollar on the foreign exchange market.

Rising bond yields also imply that inflation could become problematic for economies. Gold and silver in recent years have seemingly let loose of their grip as a hard-asset inflation hedge. My bias is that gold and silver remain inflation hedges. The reason the two metals have not displayed more price strength when inflation has risen in recent years is that inflation levels have not been problematic enough to create major problems in economies — such as was the case in the late 1970s when annual inflation came close to 15%. My bet is that if annual inflation rates move to double-digit levels, the markets and the public will be spooked and will look to hard assets to hedge that inflation.

Tell me what you think. I enjoy hearing from my valued Barchart readers from all around the globe. Email me at jim@jimwyckoff.com.

On the date of publication, Jim Wyckoff did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart