Apple (AAPL) will release its second-quarter fiscal 2026 earnings on Thursday, April 30, against the backdrop of a leadership transition. The iPhone maker announced that CEO Tim Cook will step down, with John Ternus, currently Apple’s senior vice president of hardware engineering, taking over the role effective Sept. 1. Notably, Ternus has been closely involved in shaping Apple’s core products innovation pipeline, and his appointment points to enhancement in the company’s product strategy.

AAPL stock has remained largely range-bound ahead of the earnings release, reflecting that the market has already priced in margin pressure linked to rising memory costs and supply constraints. While component inflation is expected to weigh on gross margins, this headwind could be offset by resilient iPhone demand, which continues to drive its overall revenues. Strong unit volumes and pricing power in the flagship product category could support top-line growth and earnings in the quarter.

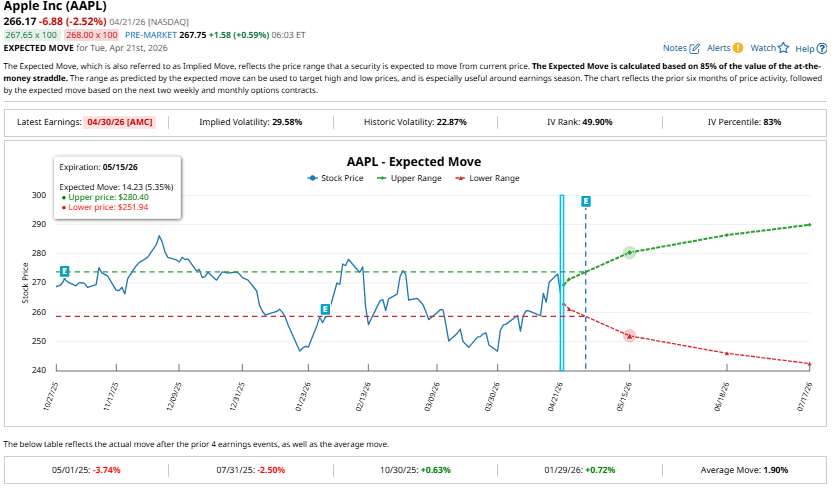

Market expectations indicate heightened volatility in AAPL stock relative to recent earnings cycles. Options pricing suggests a potential post-earnings move of approximately 5.4% in either direction, a notable increase from the average 1.9% move observed over the past four quarters. This signals heightened investor uncertainty, driven by leadership changes and margin pressures.

Apple Q2: iPhone and Services Could Power Apple’s Financials

Apple’s Q2 will reflect strong demand for its hardware and services. The iPhone remains the key catalyst, with strong upgrade activity and sustained switching from competing platforms driving its revenue and profitability. Even as tight supply could weigh on the sales, management’s guidance for 13% to 16% year-over-year (YoY) growth in overall revenue implies that underlying demand remains solid.

Supporting the favorable outlook is Apple’s first-quarter performance. Notably, iPhone revenue reached $85.3 billion in Q1, up 23% YoY with strong growth across all geographic segments. iPhone sales are expected to benefit from a significant increase in iPhone upgraders and steady growth in switchers.

Apple projects gross margins in the March quarter to be within 48% to 49%. The midpoint is slightly above the previous quarter’s 48.2%. While input costs and broader macro pressures persist, the company appears to be offsetting these challenges through a favorable product mix and operating leverage. Higher-end devices and an increasing contribution from services are key factors supporting this margin stability.

The services segment will continue to drive Apple’s profitability. First-quarter services revenue reached $30 billion, growing 14% YoY. The growth was broad-based, spanning advertising, digital content, payments, and cloud offerings. Importantly, services' gross margin rose to 76.5%, reflecting both scale benefits and mix improvements.

Apple’s installed base, which exceeded 2.5 billion active devices, provides a significant base for long-term growth. Engagement metrics remain robust, with both paid accounts and transaction volumes reaching all-time highs.

Looking ahead, management expects services growth to maintain a trajectory similar to the December quarter, suggesting continued momentum.

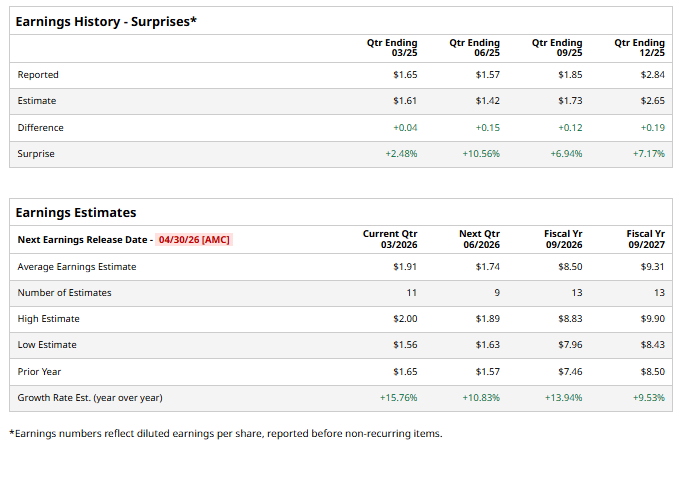

Analysts are projecting solid YoY earnings growth for the quarter, reflecting confidence in Apple’s ability to navigate cost pressures while sustaining demand. Analysts expect Apple to deliver second-quarter earnings of $1.91 per share, up 15.8% YoY. Moreover, the company’s historical tendency to outperform earnings expectations adds optimism.

AAPL Stock: Buy, Sell, or Hold?

Apple’s near-term outlook presents a balanced risk-reward profile. On one hand, resilient iPhone demand, strong services growth, and a vast installed base provide structural support for continued earnings expansion. On the other hand, margin pressures, supply constraints, and leadership transitions introduce uncertainty that could drive short-term volatility.

For long-term investors, Apple’s fundamentals remain intact, supported by its ecosystem strength and evolving revenue mix. This supports a positive bias towards AAPL stock. However, for short-term traders, the elevated volatility expectations suggest a more cautious approach.

Analysts are cautiously optimistic about AAPL stock ahead of the earnings release and maintain a “Moderate Buy” consensus rating.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Should You Buy the Dip in United Airlines Stock?

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?