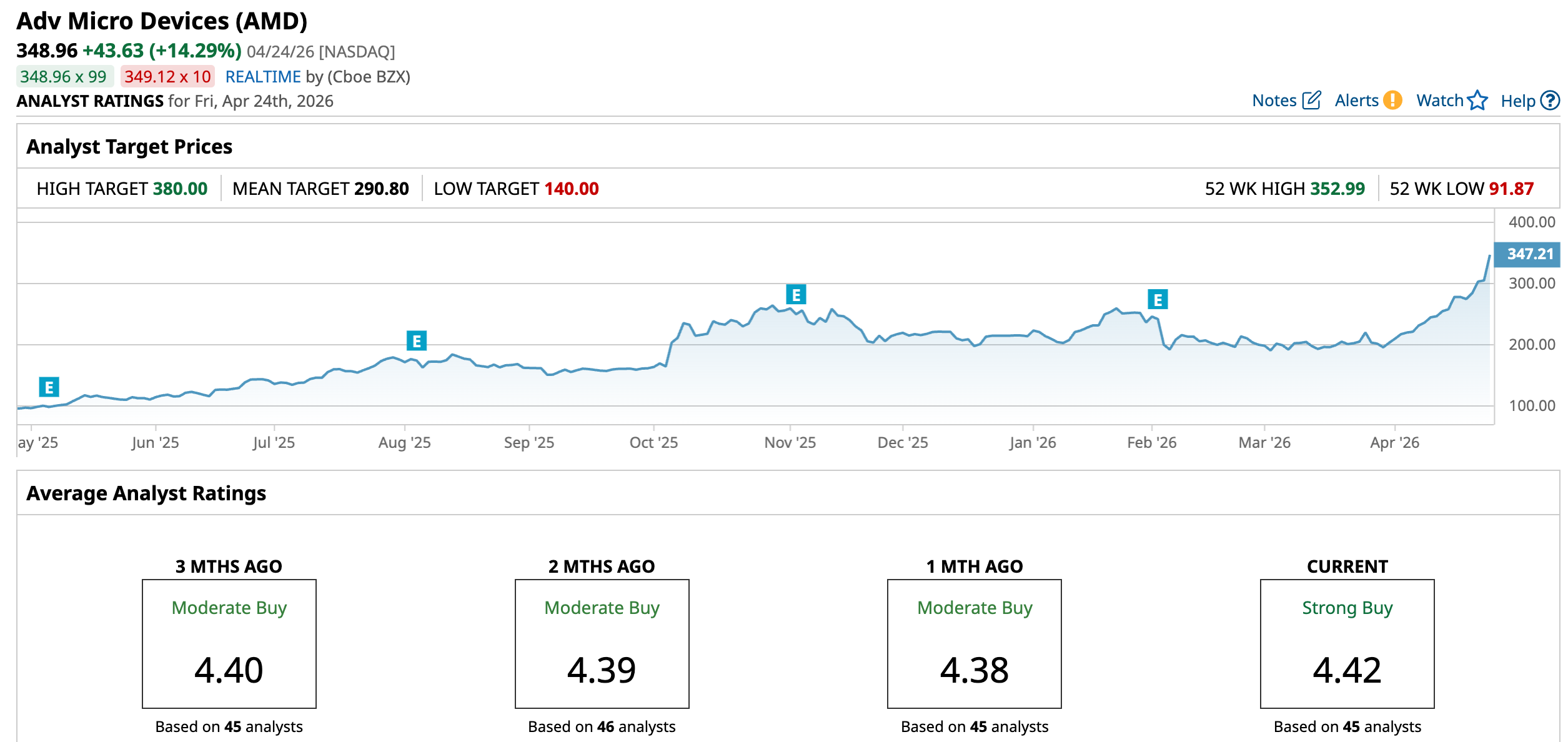

Shares of Advanced Micro Devices (AMD) have surged 70.6% over the past month, recently hitting record highs. The stock is up almost 15% in the morning trading session after rival Intel (INTC) reported strong AI-driven demand for CPUs.

Intel’s management emphasized that the CPU is gaining prominence within AI systems, with enterprise and cloud customers increasingly deploying server CPUs alongside accelerators. This has translated into robust demand for Intel’s Xeon processors, signaling that the ongoing expansion of AI infrastructure is likely to boost CPU usage more broadly.

In addition, Intel’s leadership expressed confidence that this demand will persist, forecasting double-digit growth in server CPU shipments across the industry through 2027.

That outlook bodes well for AMD, which has been steadily strengthening its position in the data center market.

AMD’s data center revenue jumped 39% year-over-year (YOY) to a record $5.4 billion in its most recent quarter. Growth has been driven by both its Instinct GPUs and its EPYC server CPUs. Notably, AMD’s latest fifth-generation EPYC processors made up more than half of its server revenue. At the same time, older EPYC chips are still selling well, thanks to their strong performance and cost advantages.

Demand is coming from both major cloud providers and traditional enterprises. Hyperscalers are continuing to expand their infrastructure to handle rising AI workloads, while enterprises are upgrading their data centers to support new applications. In both cases, AMD is benefiting from a shift toward more efficient, high-performance CPUs and gaining market share.

Looking ahead, AMD is preparing to launch its next-generation Venice CPUs, which are already generating strong customer interest. Management said that large cloud deployments are in the works, and support from hardware partners is expected to be broad. This suggests that AMD’s momentum in the server market could continue.

On top of strong demand, AMD may also benefit from rising CPU prices. Tight supply across the industry is creating a more favorable pricing environment that could help improve the company’s profit margins.

Why AMD Stock Is Still a Buy?

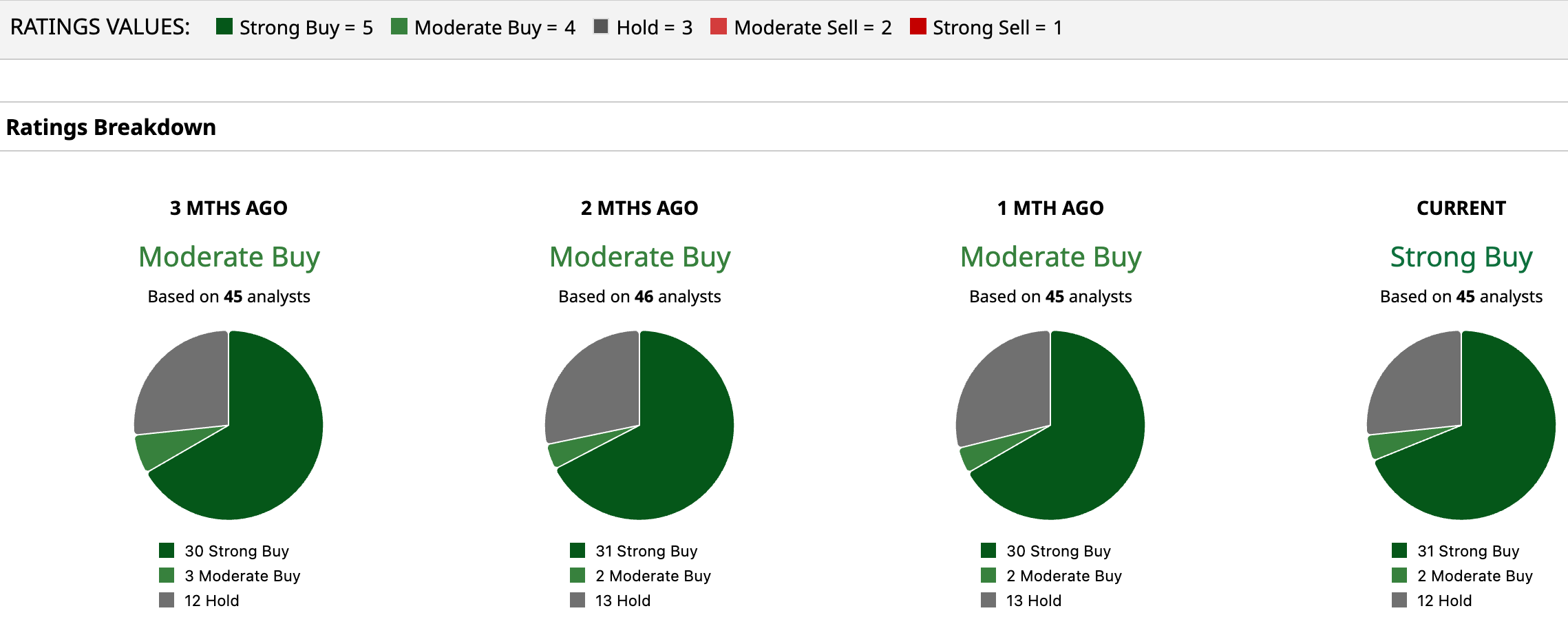

Despite the rally, AMD’s investment case remains compelling, supported by accelerating demand for its server CPUs and Instinct GPUs. Along with solid momentum in its server CPUs, AMD is witnessing strong adoption of its Instinct GPU lineup. Demand for the MI350 series has translated into a meaningful uptick in data center revenue, with customer adoption expanding.

The company’s roadmap further strengthens this trajectory. The upcoming MI400 series is designed to address a broader spectrum of workloads spanning cloud infrastructure, high-performance computing, and enterprise AI, while development of the MI500 series, targeted for a 2027 release, indicates sustained long-term investment in this high-growth category.

AMD expects its data center segment to grow at a CAGR of over 60% in the next three to five years, with AI-related revenue likely to generate solid growth. As AI workloads become more complex and widespread, the need for diversified hardware solutions should continue to expand AMD’s addressable market.

While AMD’s revenue is expected to increase at a solid pace, improved product mix and pricing power are likely to give its business a significant lift. Strategic partnerships are also strengthening AMD’s growth prospects. Its expanded agreement with Meta Platforms (META) will likely support its growth.

From a valuation point, AMD stock appears reasonably priced relative to its growth profile. AMD stock trades at a forward price-to-earnings multiple of approximately 52.5 times, which is justified by its projected earnings trajectory. Analysts’ consensus estimates point to earnings growth exceeding 77% in 2026, suggesting further upside.

Overall, AMD’s investment case is supported by sustained demand for high-performance CPUs, rapid expansion in AI accelerators, a solid product roadmap, and deepening relationships with major cloud customers. Moreover, its reasonable valuation and positive analyst sentiment support AMD’s bull case.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 3 Under-the-Radar Dividend Stocks Yielding Up to 13% That Wall Street Rates a Strong Buy

- Intel Is Leading SanDisk Higher. Should You Chase SNDK Stock Today?

- Should You Buy the Dip in Oracle Stock? Dan Ives Thinks So.

- Much Like Their Pants, I’m Not Ready for Another Tight Squeeze with Lululemon’s Stock