Midwest regional bank QCR Holdings (NASDAQGM:QCRH) missed Wall Street’s revenue expectations in Q1 CY2026 as sales rose 4.1% year on year to $90.39 million. Its non-GAAP profit of $1.99 per share was 11.9% above analysts’ consensus estimates.

Is now the time to buy QCR Holdings? Find out by accessing our full research report, it’s free.

QCR Holdings (QCRH) Q1 CY2026 Highlights:

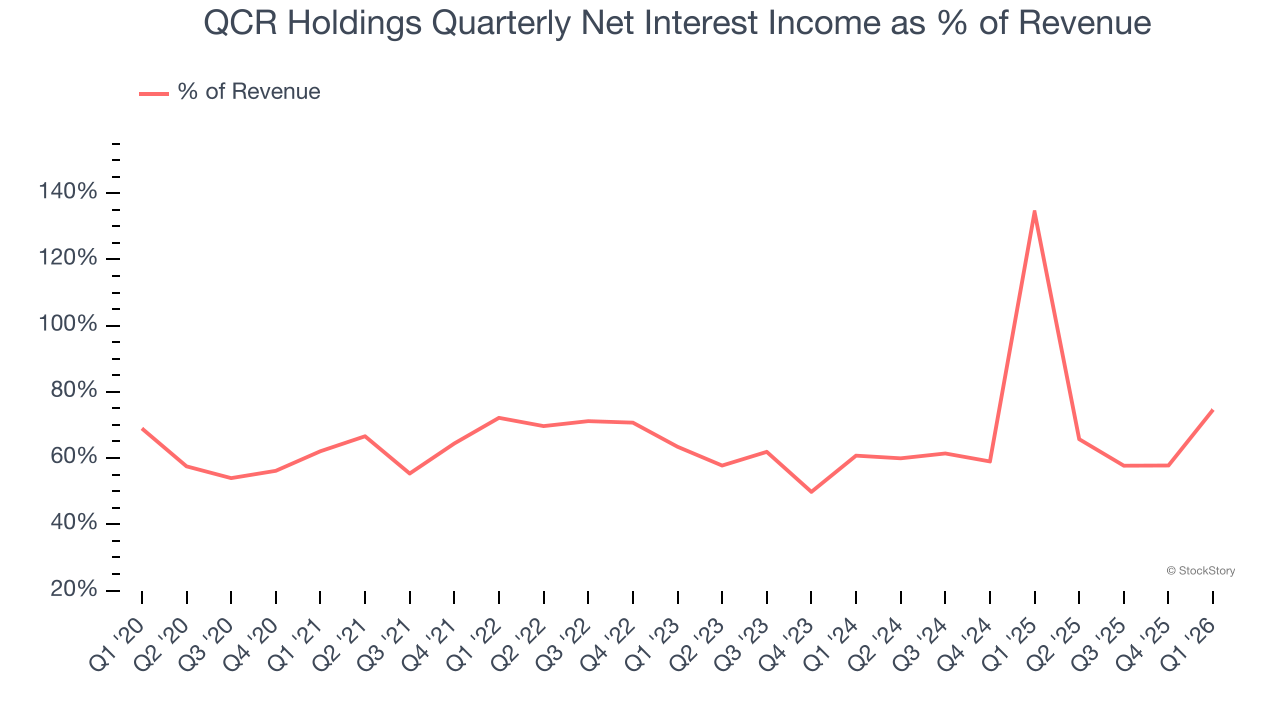

- Net Interest Income: $67.44 million vs analyst estimates of $67.04 million (42.2% year-on-year decline, 0.6% beat)

- Net Interest Margin: 3.2% vs analyst estimates of 3.6% (44.8 basis point miss)

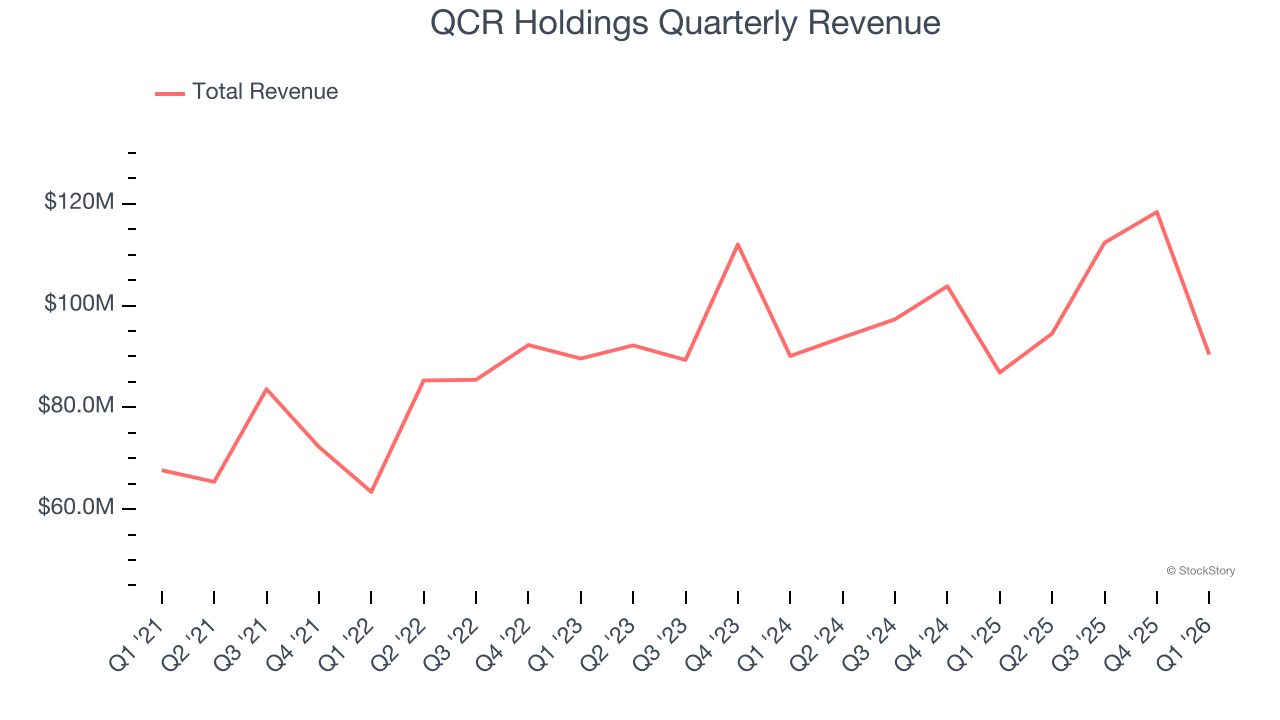

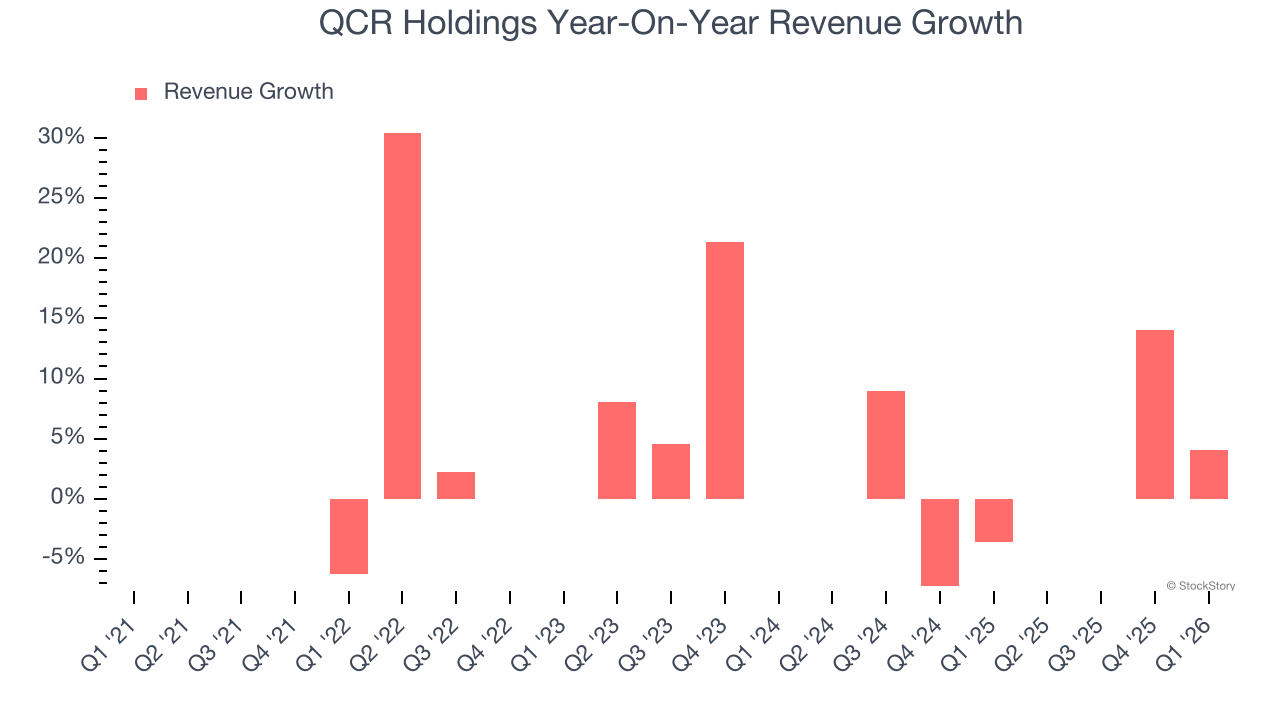

- Revenue: $90.39 million vs analyst estimates of $105 million (4.1% year-on-year growth, 13.9% miss)

- Efficiency Ratio: 57.7% vs analyst estimates of 56.2% (144.8 basis point miss)

- Adjusted EPS: $1.99 vs analyst estimates of $1.78 (11.9% beat)

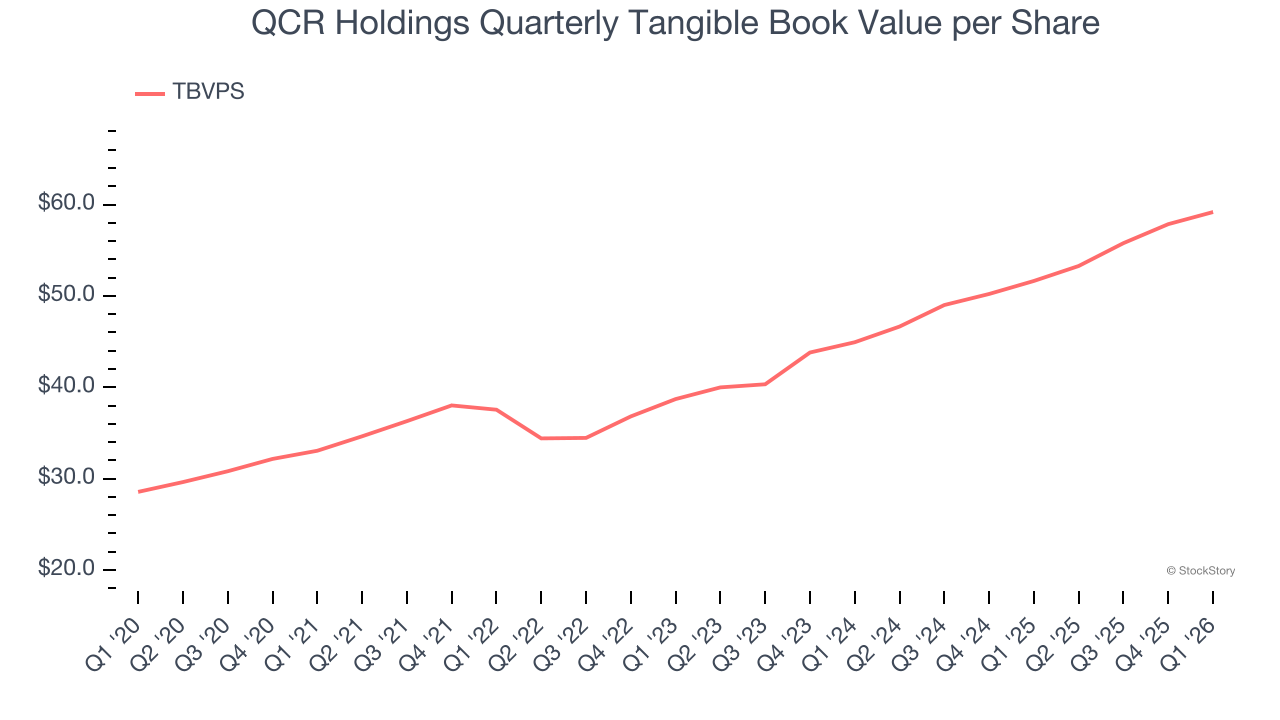

- Tangible Book Value per Share: $59.18 vs analyst estimates of $59.45 (14.6% year-on-year growth, in line)

- Market Capitalization: $1.51 billion

“We are very pleased to have delivered record first quarter net income, representing 1.40% ROAA and 31% EPS growth compared to a year ago, in what is historically a softer quarter for capital markets revenue. Our strong first quarter results were highlighted by healthy loan and deposit growth, significantly lower noninterest expense, and modest margin expansion. These results underscore the continued progress we are making in strengthening profitability across our traditional banking and wealth management businesses. We also maintained excellent asset quality and generated meaningful growth in tangible book value per share while returning nearly $21 million to shareholders through opportunistic share repurchases. Additionally, we continued investing in our digital transformation as we build a more modern, scalable bank for our clients and employees,” said Todd Gipple, President and Chief Executive Officer.

Company Overview

With roots dating back to 1993 and a name reflecting its original Quad Cities market, QCR Holdings (NASDAQGM:QCRH) operates four community banks across Iowa and Missouri, providing commercial, consumer banking, and trust services to businesses and individuals.

Sales Growth

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Unfortunately, QCR Holdings’s 6.8% annualized revenue growth over the last five years was tepid. This was below our standard for the banking sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. QCR Holdings’s recent performance shows its demand has slowed as its annualized revenue growth of 4.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, QCR Holdings’s revenue grew by 4.1% year on year to $90.39 million, falling short of Wall Street’s estimates.

Net interest income made up 66.7% of the company’s total revenue during the last five years, meaning lending operations are QCR Holdings’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

QCR Holdings’s TBVPS grew at an incredible 12.4% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 14.8% annually over the last two years from $44.93 to $59.18 per share.

Over the next 12 months, Consensus estimates call for QCR Holdings’s TBVPS to grow by 13.2% to $66.99, decent growth rate.

Key Takeaways from QCR Holdings’s Q1 Results

It was good to see QCR Holdings beat analysts’ EPS expectations this quarter. We were also happy its net interest income narrowly outperformed Wall Street’s estimates. On the other hand, its revenue and net interest margin missed. Overall, this was a mixed quarter. The stock remained flat at $88.97 immediately after reporting.

QCR Holdings underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).