Over the past six months, Matrix Service’s shares (currently trading at $11.99) have posted a disappointing 13.6% loss, well below the S&P 500’s 4.8% gain. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy Matrix Service, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Matrix Service Not Exciting?

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons we avoid MTRX and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

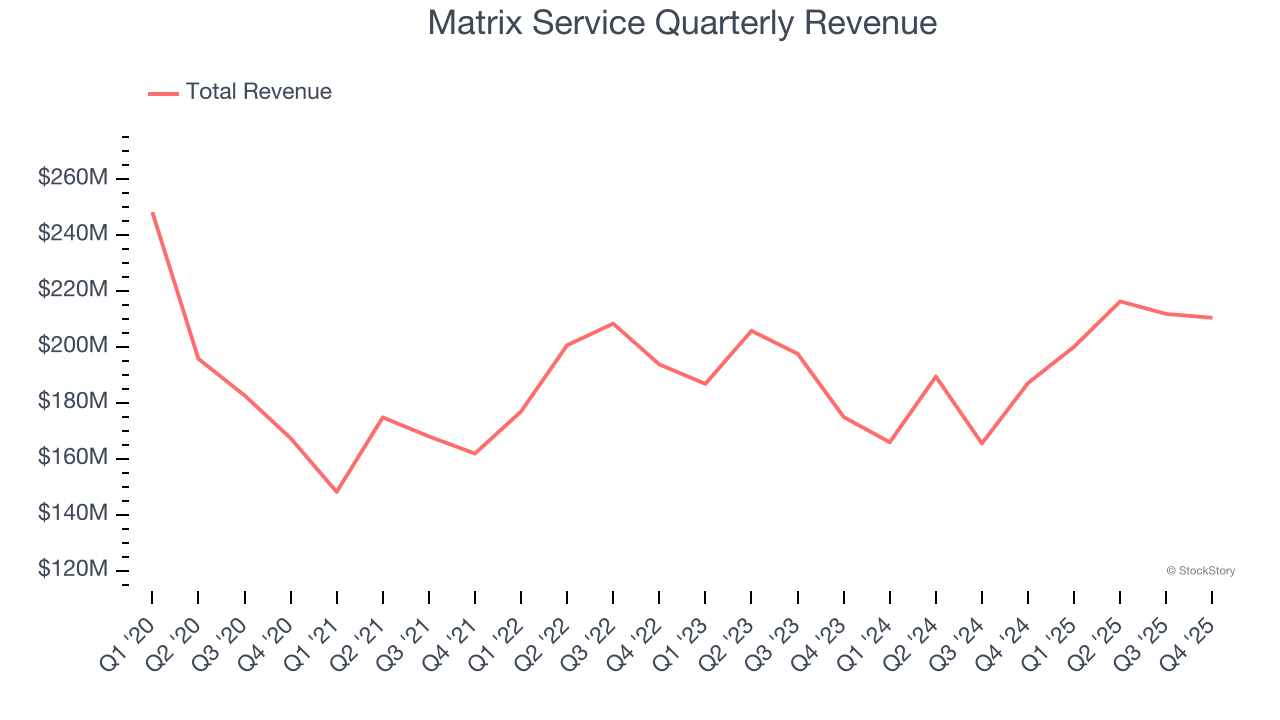

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Matrix Service’s sales grew at a weak 1.1% compounded annual growth rate over the last five years. This was below our standards.

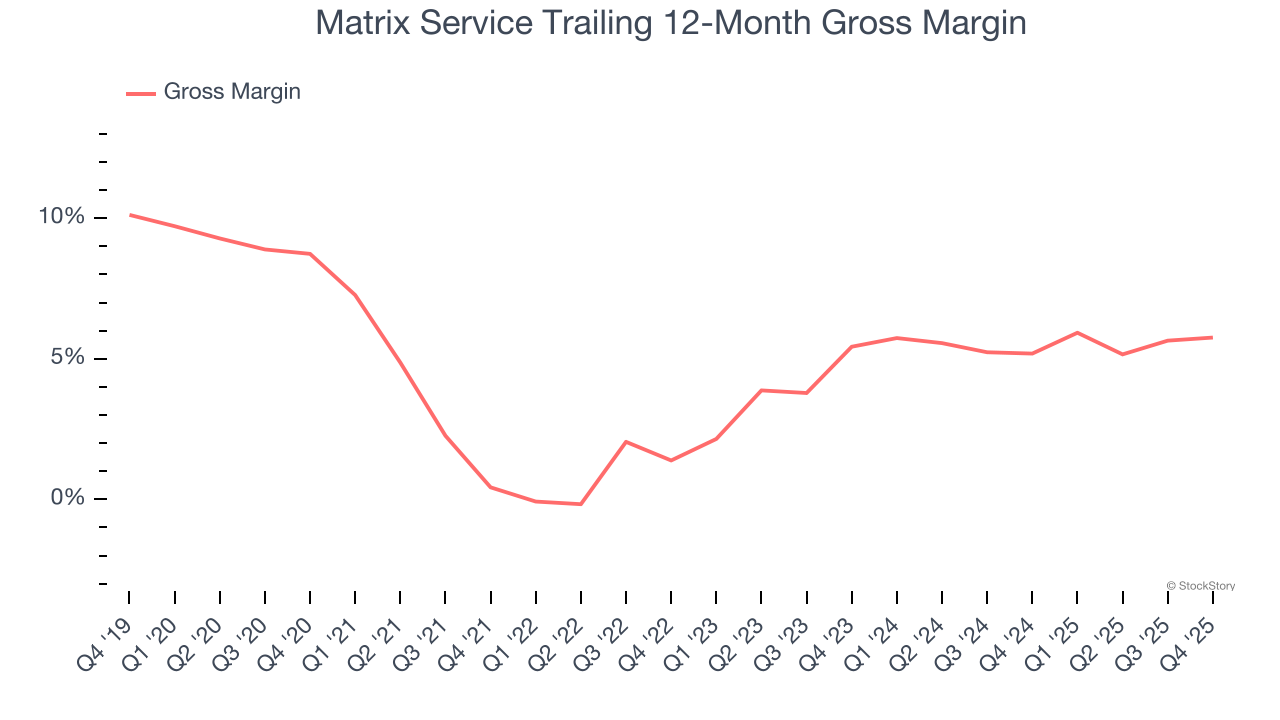

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they usually indicate that a company sells more differentiated products and commands stronger pricing power.

Matrix Service has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 3.7% gross margin over the last five years. That means Matrix Service paid its suppliers a lot of money ($96.26 for every $100 in revenue) to run its business.

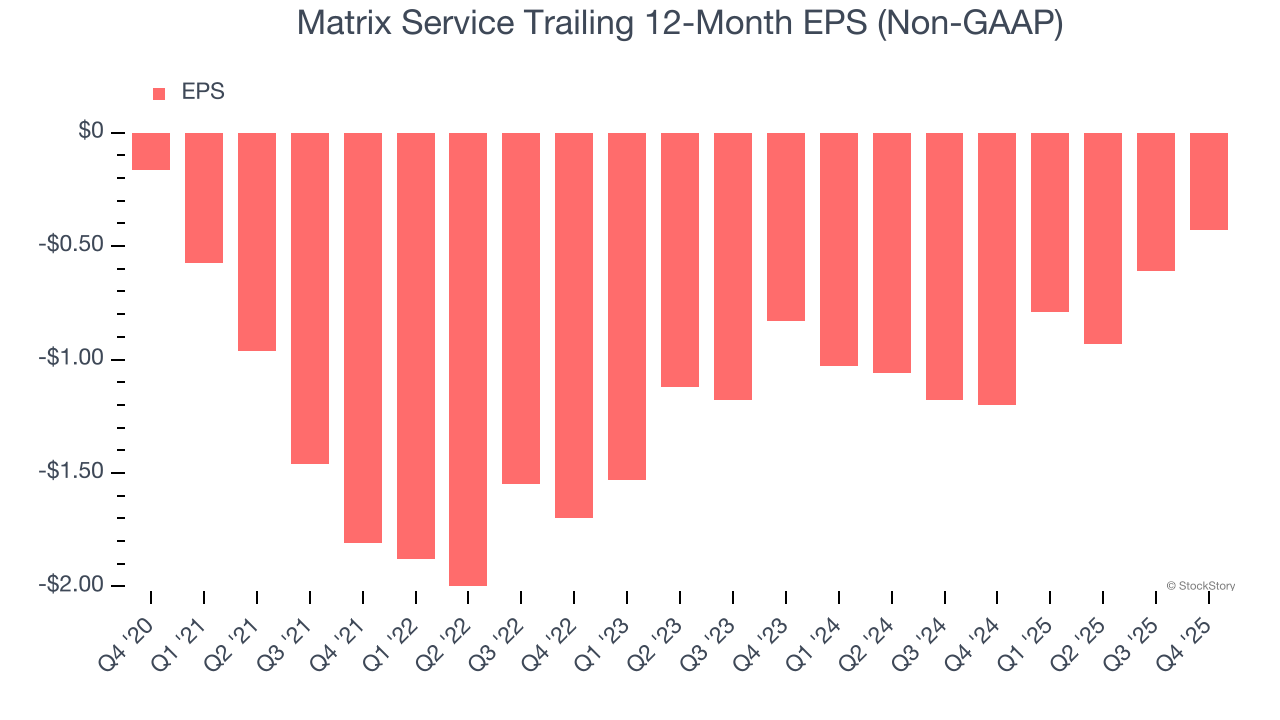

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Matrix Service’s earnings losses deepened over the last five years as its EPS dropped 21.4% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Matrix Service’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Matrix Service’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 18.3× forward P/E (or $11.99 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Matrix Service

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.