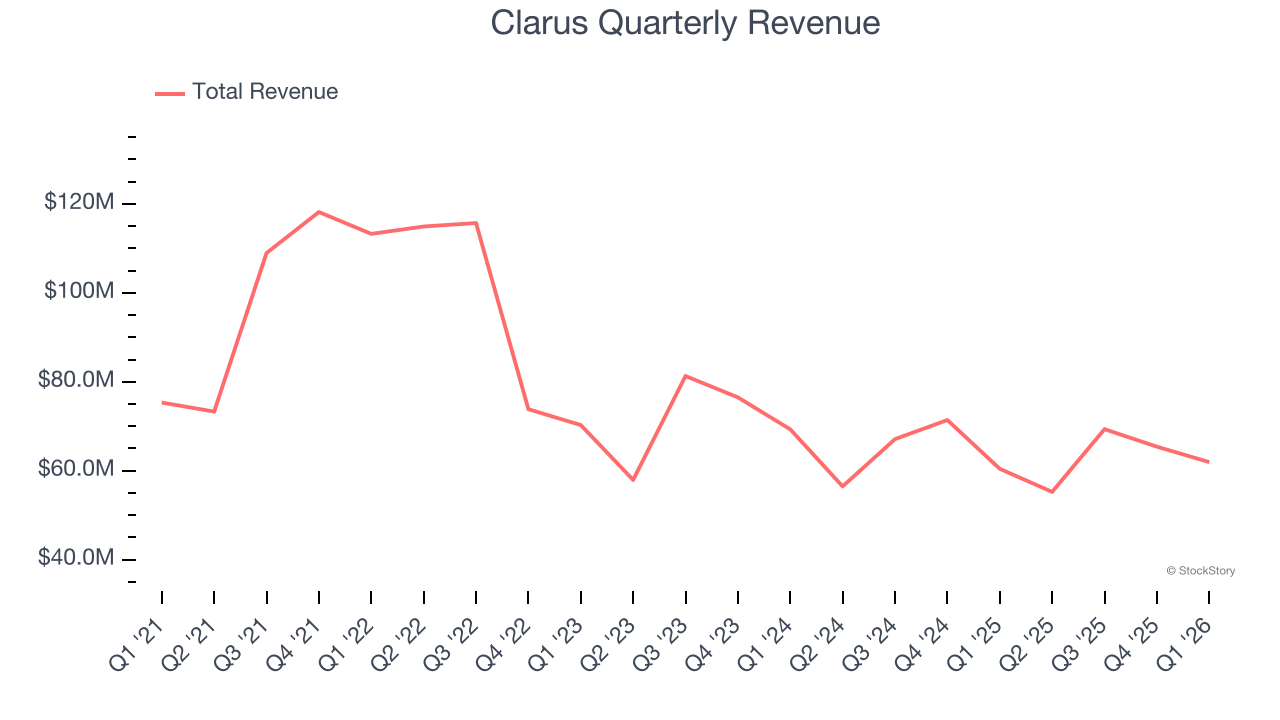

Outdoor lifestyle and equipment company Clarus (NASDAQ: CLAR) announced better-than-expected revenue in Q1 CY2026, with sales up 2.5% year on year to $61.94 million. On the other hand, the company’s full-year revenue guidance of $250 million at the midpoint came in 3.3% below analysts’ estimates. Its non-GAAP profit of $0.02 per share was $0.02 above analysts’ consensus estimates.

Is now the time to buy Clarus? Find out by accessing our full research report, it’s free.

Clarus (CLAR) Q1 CY2026 Highlights:

- Revenue: $61.94 million vs analyst estimates of $61.21 million (2.5% year-on-year growth, 1.2% beat)

- Adjusted EPS: $0.02 vs analyst estimates of $0 ($0.02 beat)

- Adjusted EBITDA: -$1.12 million vs analyst estimates of $160,600 (-1.8% margin, significant miss)

- The company dropped its revenue guidance for the full year to $250 million at the midpoint from $260 million, a 3.8% decrease

- EBITDA guidance for the full year is $4 million at the midpoint, below analyst estimates of $9.32 million

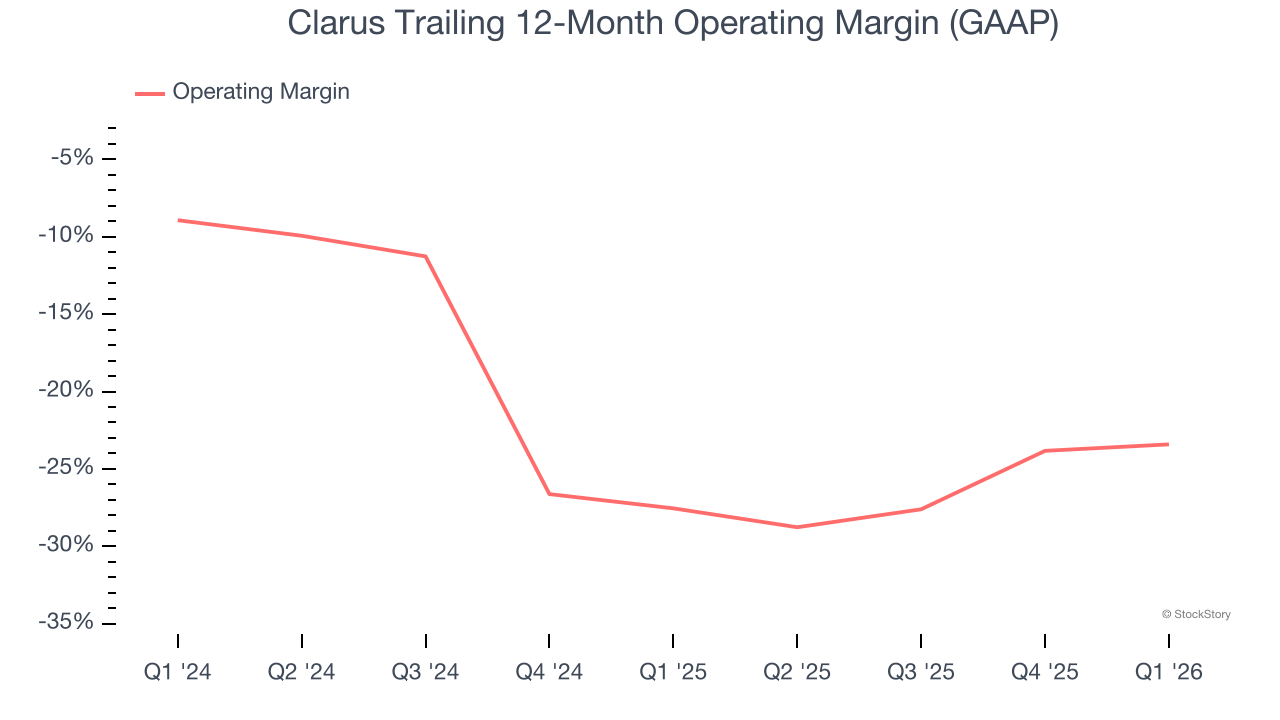

- Operating Margin: -9.8%, up from -11.2% in the same quarter last year

- Market Capitalization: $113 million

Management Commentary“During the first quarter, we advanced key initiatives and delivered improved revenue and adjusted EBITDA year-over-year,” said Warren Kanders, Clarus’ Executive Chairman.

Company Overview

Initially a financial services business, Clarus (NASDAQ: CLAR) designs, manufactures, and distributes outdoor equipment and lifestyle products.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Clarus struggled to consistently increase demand as its $251.9 million of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

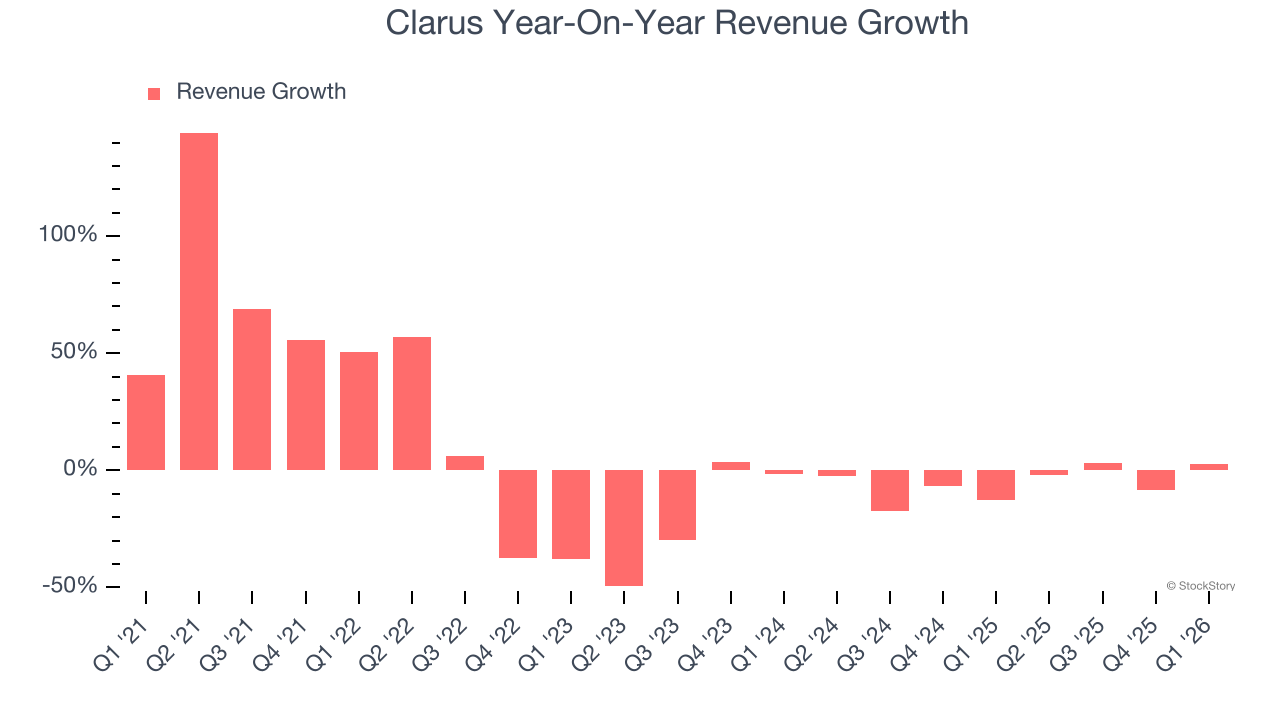

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Clarus’s recent performance shows its demand remained suppressed as its revenue has declined by 6% annually over the last two years.

This quarter, Clarus reported modest year-on-year revenue growth of 2.5% but beat Wall Street’s estimates by 1.2%.

Looking ahead, sell-side analysts expect revenue to grow 3.9% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Clarus’s operating margin has been trending up over the last 12 months, but it still averaged negative 25.5% over the last two years. This is due to its large expense base and inefficient cost structure.

This quarter, Clarus generated a negative 9.8% operating margin. The company's consistent lack of profits raise a flag.

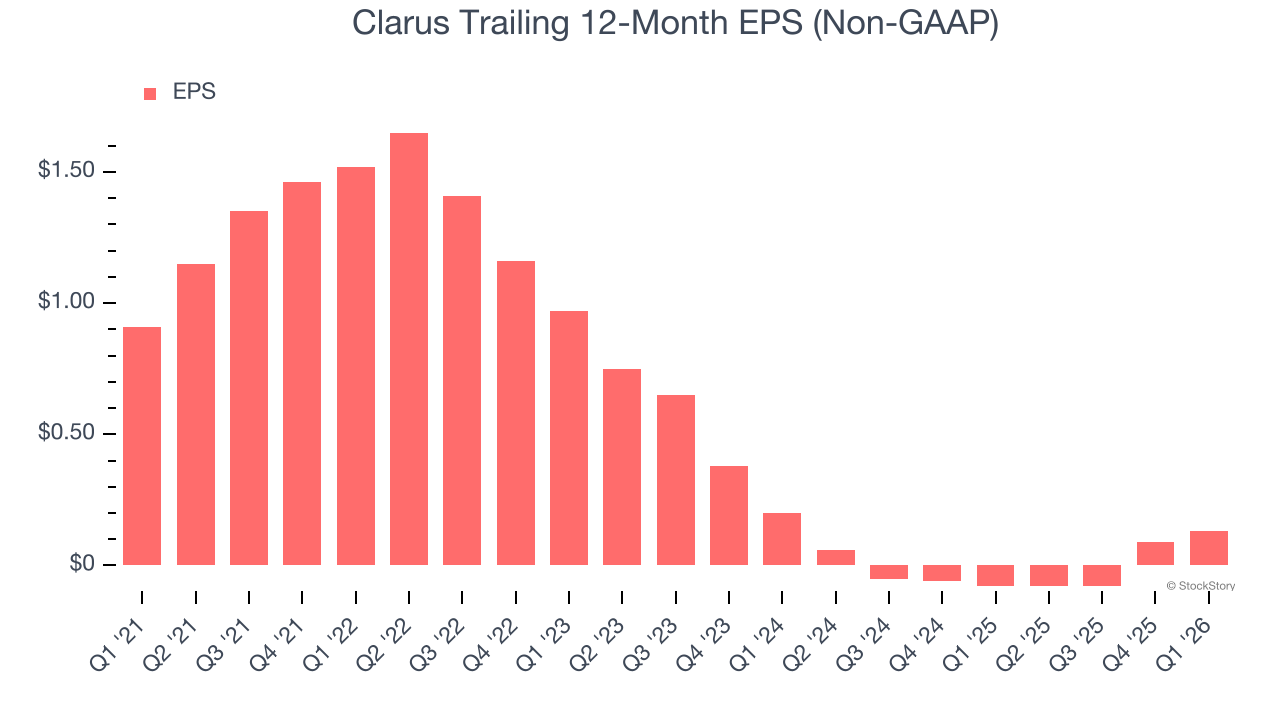

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Clarus, its EPS declined by 32.2% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q1, Clarus reported adjusted EPS of $0.02, up from negative $0.02 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Clarus’s Q1 Results

It was good to see Clarus beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $2.90 immediately following the results.

Is Clarus an attractive investment opportunity right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).