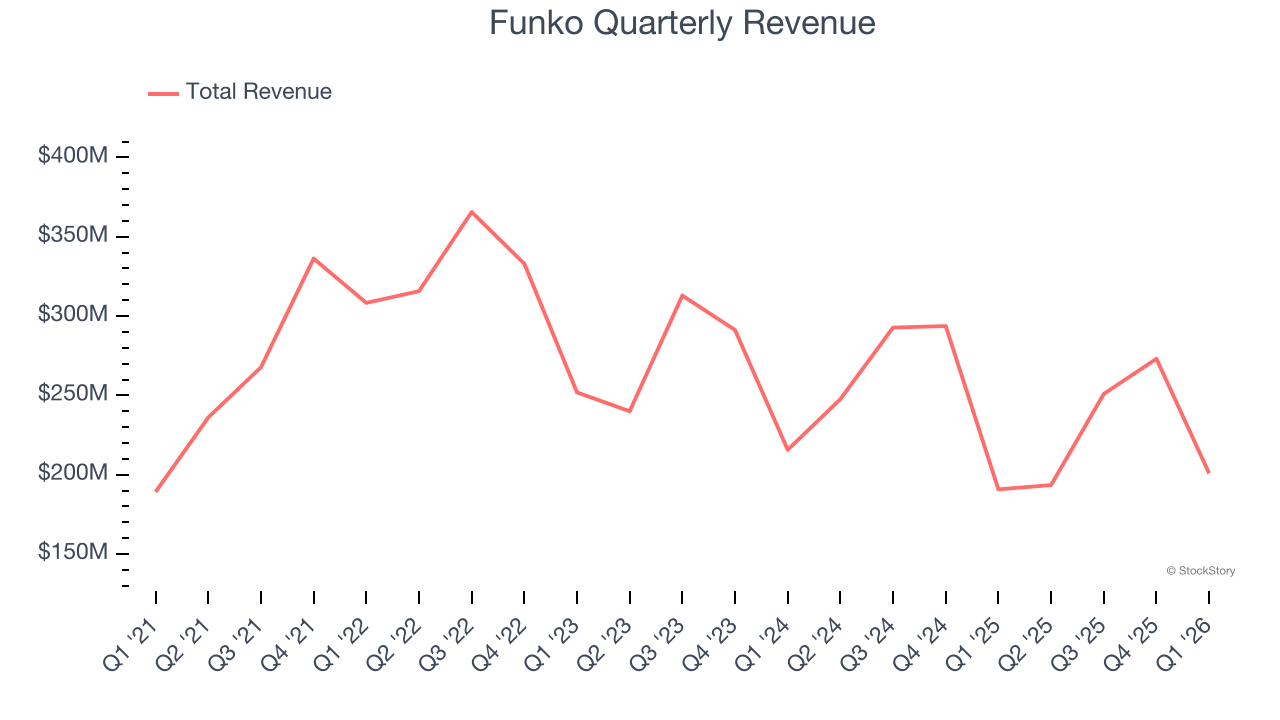

Pop culture collectibles manufacturer Funko (NASDAQ: FNKO) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 5.3% year on year to $200.9 million. On the other hand, next quarter’s revenue guidance of $200 million was less impressive, coming in 2% below analysts’ estimates. Its non-GAAP loss of $0.11 per share was 63.3% above analysts’ consensus estimates.

Is now the time to buy Funko? Find out by accessing our full research report, it’s free.

Funko (FNKO) Q1 CY2026 Highlights:

- Revenue: $200.9 million vs analyst estimates of $188.8 million (5.3% year-on-year growth, 6.4% beat)

- Adjusted EPS: -$0.11 vs analyst estimates of -$0.30 (63.3% beat)

- Adjusted EBITDA: $11.28 million vs analyst estimates of $4,500 (5.6% margin, significant beat)

- Revenue Guidance for Q2 CY2026 is $200 million at the midpoint, below analyst estimates of $204.1 million

- EBITDA guidance for the full year is $75 million at the midpoint, in line with analyst expectations

- Operating Margin: -4.8%, up from -12.2% in the same quarter last year

- Free Cash Flow was $1.94 million, up from -$28.39 million in the same quarter last year

- Market Capitalization: $242.8 million

“We kicked off the year with a strong Q1 performance, building on the positive momentum from the second half of 2025, with net sales, gross margin and adjusted EBITDA all exceeding expectations,” said Josh Simon, Chief Executive Officer of Funko.

Company Overview

Boasting partnerships with media franchises like Marvel and One Piece, Funko (NASDAQ: FNKO) is a company specializing in creating and distributing licensed pop culture collectibles.

Revenue Growth

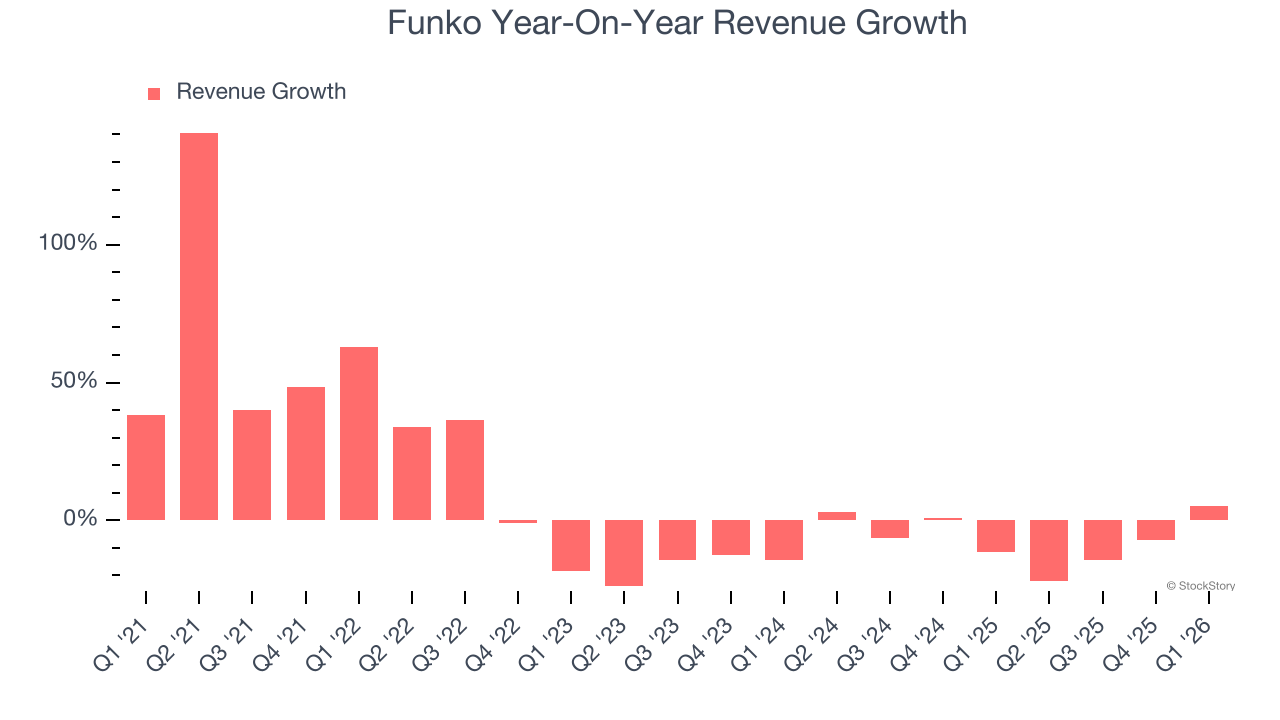

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Funko’s sales grew at a weak 5.4% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Funko’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 6.9% annually.

This quarter, Funko reported year-on-year revenue growth of 5.3%, and its $200.9 million of revenue exceeded Wall Street’s estimates by 6.4%. Company management is currently guiding for a 3.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.2% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

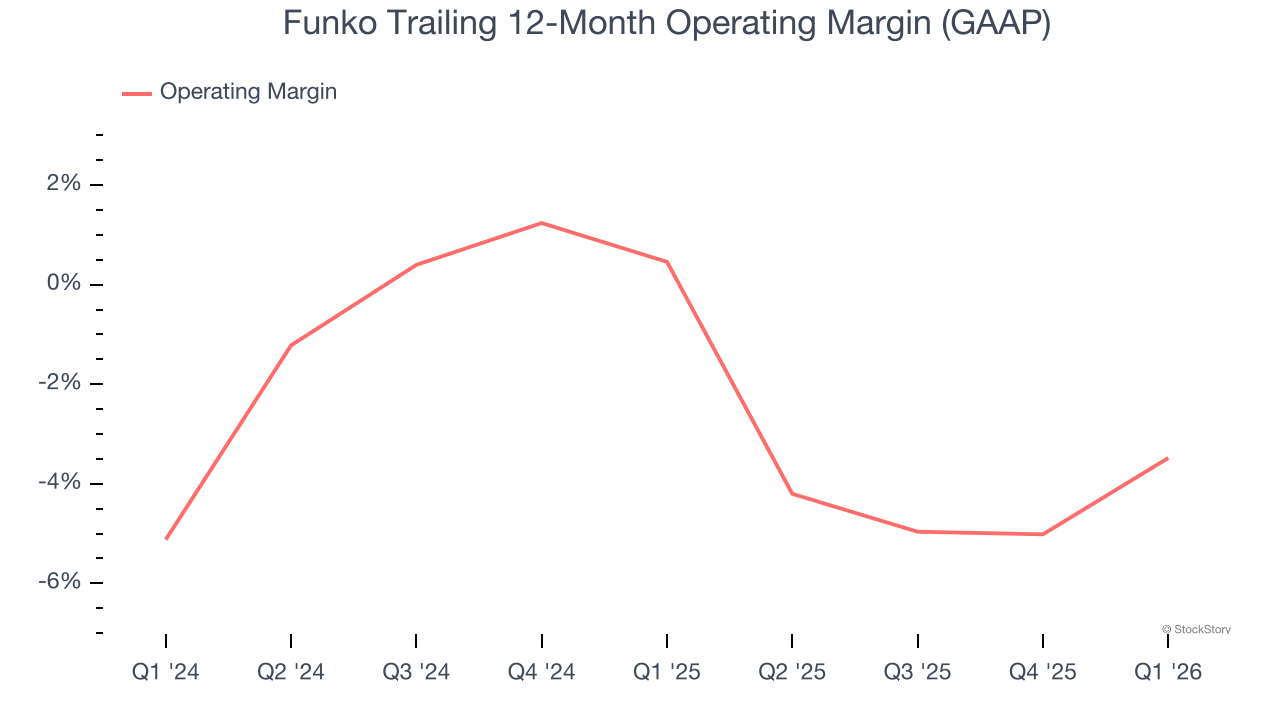

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Funko’s operating margin has shrunk over the last 12 months and averaged negative 1.4% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

This quarter, Funko generated a negative 4.8% operating margin. The company's consistent lack of profits raise a flag.

Earnings Per Share

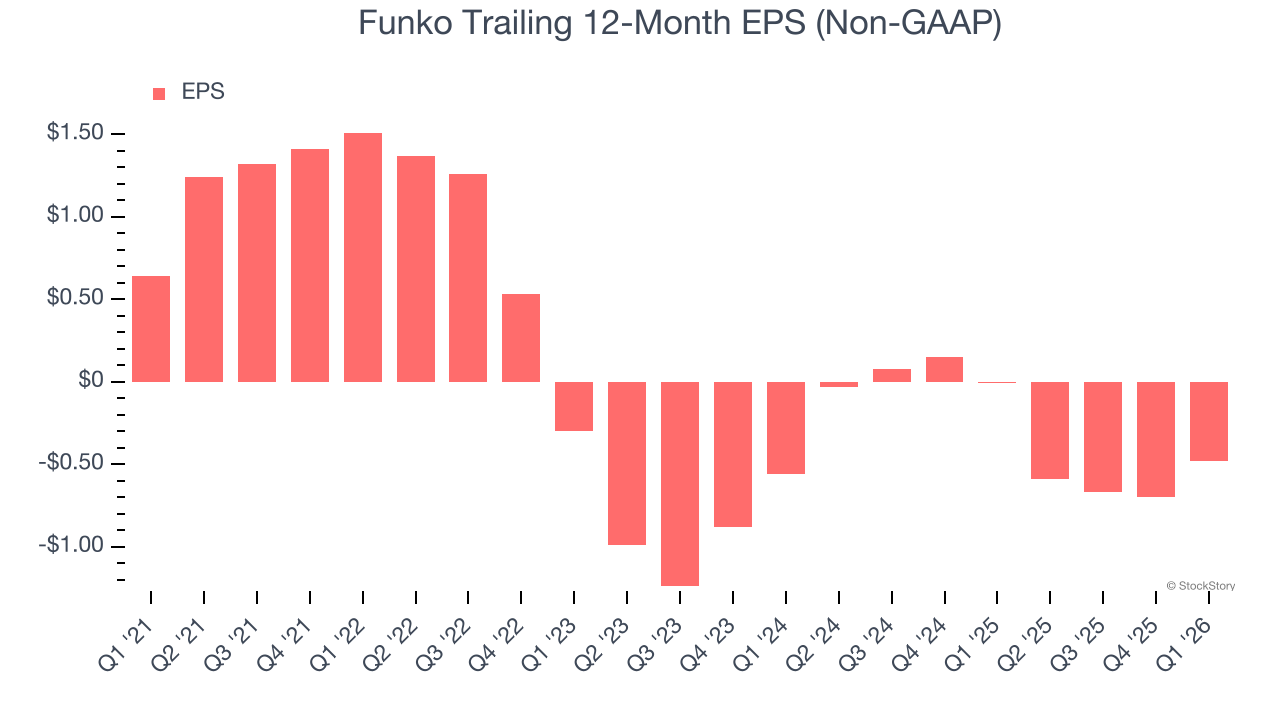

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Funko, its EPS declined by 22.4% annually over the last five years while its revenue grew by 5.4%. This tells us the company became less profitable on a per-share basis as it expanded.

In Q1, Funko reported adjusted EPS of negative $0.11, up from negative $0.33 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street is optimistic. Analysts forecast Funko’s full-year EPS of negative $0.48 will reach break even.

Key Takeaways from Funko’s Q1 Results

It was good to see Funko beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its EBITDA guidance for next quarter missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 6.4% to $4.82 immediately after reporting.

Funko had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).