Solo Brands’s stock price has taken a beating over the past six months, shedding 42.4% of its value and falling to $1.14 per share. This might have investors contemplating their next move.

Is now the time to buy Solo Brands, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why there are better opportunities than DTC and a stock we'd rather own.

Why Do We Think Solo Brands Will Underperform?

Started through a Kickstarter campaign, Solo Brands (NYSE: DTC) is a provider of outdoor and recreational products.

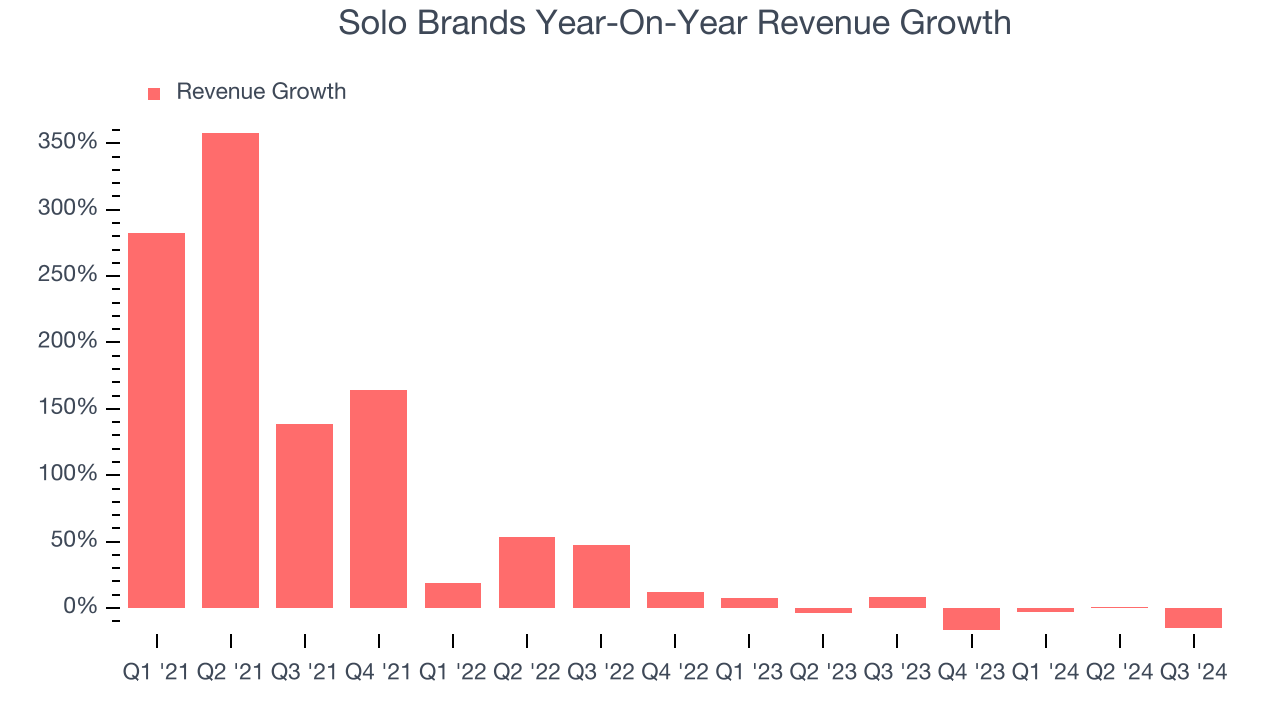

1. Revenue Tumbling Downwards

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Solo Brands’s recent history marks a sharp pivot from its four-year trend as its revenue has shown annualized declines of 2.1% over the last two years.

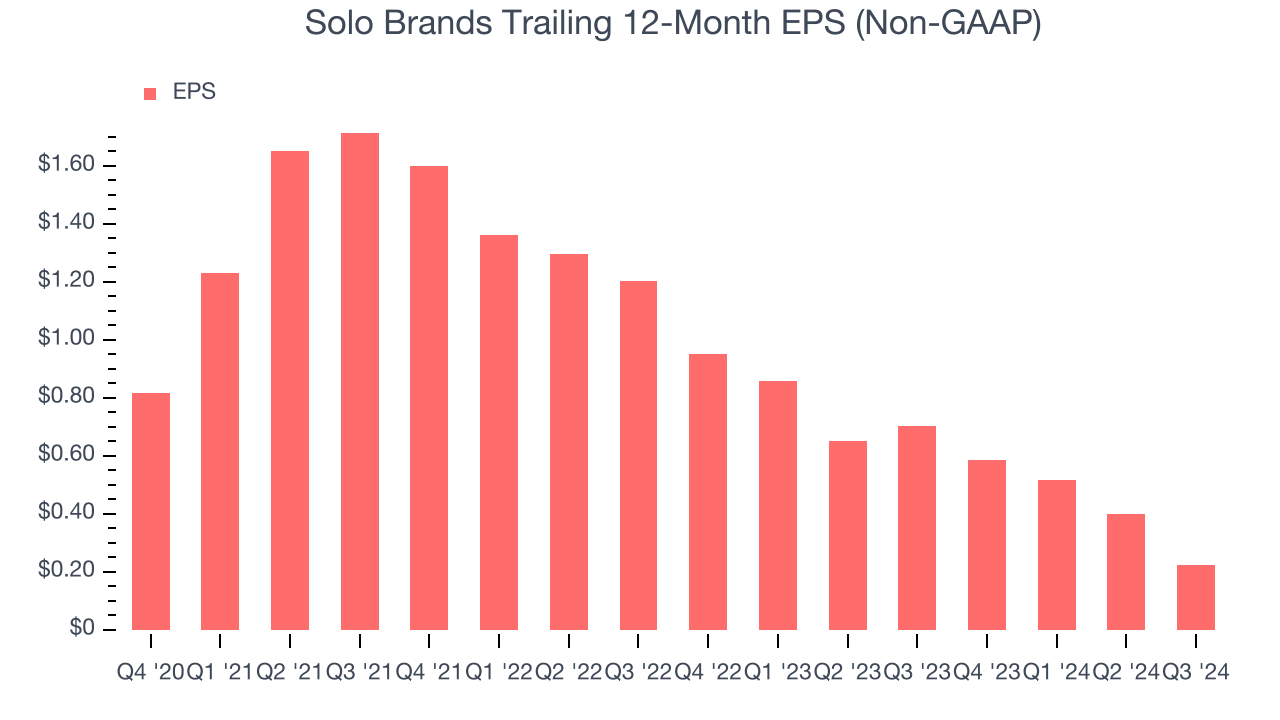

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Solo Brands, its EPS declined by 18.1% annually over the last four years while its revenue grew by 47%. This tells us the company became less profitable on a per-share basis as it expanded.

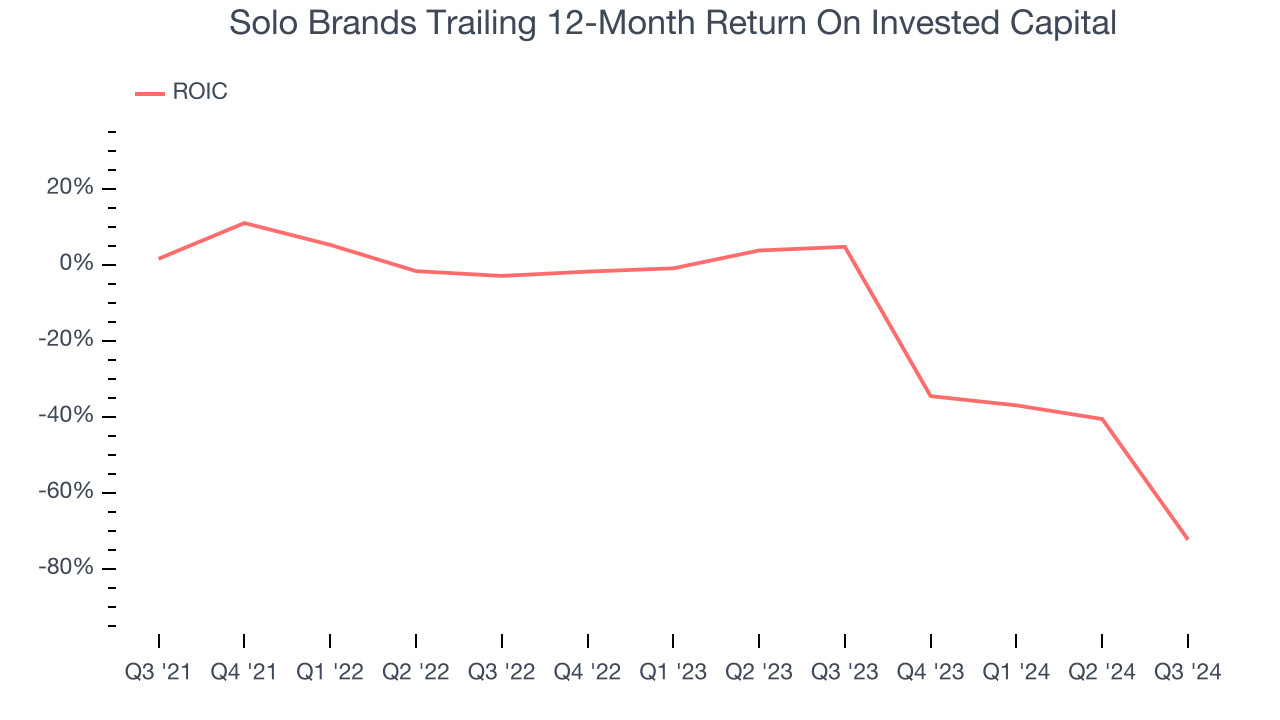

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Solo Brands’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Solo Brands doesn’t pass our quality test. After the recent drawdown, the stock trades at 3.1× forward price-to-earnings (or $1.14 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment. We’d suggest looking at Meta, a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Solo Brands

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.