Synchrony Financial (SYF) is a leading Stamford, Connecticut-based consumer financial services company specializing in private-label credit cards, installment financing, and consumer lending, primarily through partnerships with retailers, healthcare providers, and digital platforms. With a market cap of $30.5 billion, the company firmly qualifies as a large-cap, well above the $10 billion benchmark, and leverages this scale to deliver extensive credit solutions across a broad network of major retailers and service partners.

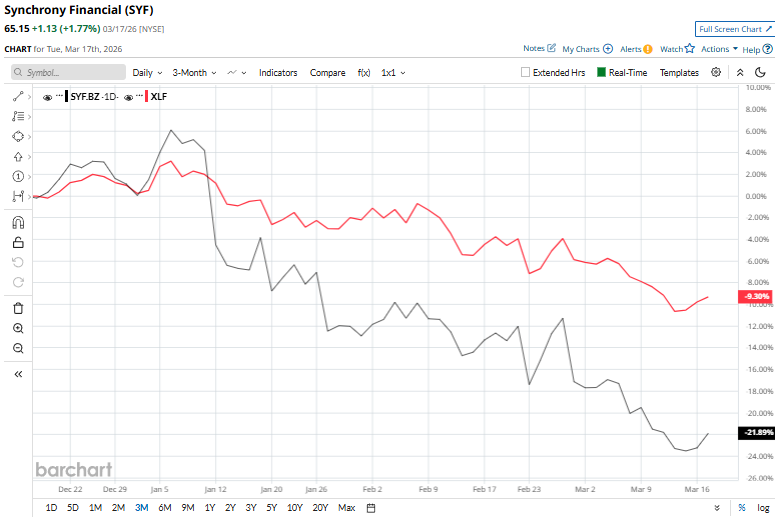

However, the stock has fallen 26.6% below its 52-week high of $88.77 touched on Jan. 9. Moreover, over the past three months, SYF has tanked 21.7%, trailing the State Street Financial Select Sector SPDR ETF’s (XLF) 9.3% drop during the same stretch.

The stock has climbed 21.9% over the past 52 weeks and has plunged 12.9% over the past six months, whereas XLF gained marginally over 52 weeks and dipped 8.4% over the past six months.

SYF stock has slipped below its 50-day and 200-day moving averages since mid-Jan and the end of February, respectively, indicating a downtrend.

Shares of Synchrony Financial dropped 7.1% on Feb. 27, as investor sentiment weakened due to rising macro and sector-specific concerns. The decline was triggered by fears that increased adoption of artificial intelligence, highlighted by workforce cuts at Block, could hurt employment and, in turn, consumer credit health. Additional pressure came from stronger-than-expected inflation data, reinforcing concerns about prolonged high interest rates, along with growing anxiety around credit quality and rising problem loans, prompting investors to reassess risk across credit-sensitive financial stocks.

Synchrony Financial has demonstrated far stronger resilience than its peer SLM Corporation (SLM), which has tanked 32.2% over the past year and nearly 30% in the last six months.

This relative outperformance is reflected in analyst sentiment as well, with 24 analysts assigning a “Moderate Buy” consensus rating and an average price target of $88.33, suggesting a potential upside of 35.6% from current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- 3 Headline-Grabbing Stocks Look Overvalued. Should Investors Sell Now?

- GOOGL, NVDA, and More: Iron Condor Screener Results for March 18

- S&P Futures Climb as Oil Prices Retreat in Run-Up to Fed Rate Decision, U.S. PPI Data and Micron Earnings on Tap

- As Applied Materials Raises Its Dividend 15%, Should You Buy AMAT Stock?