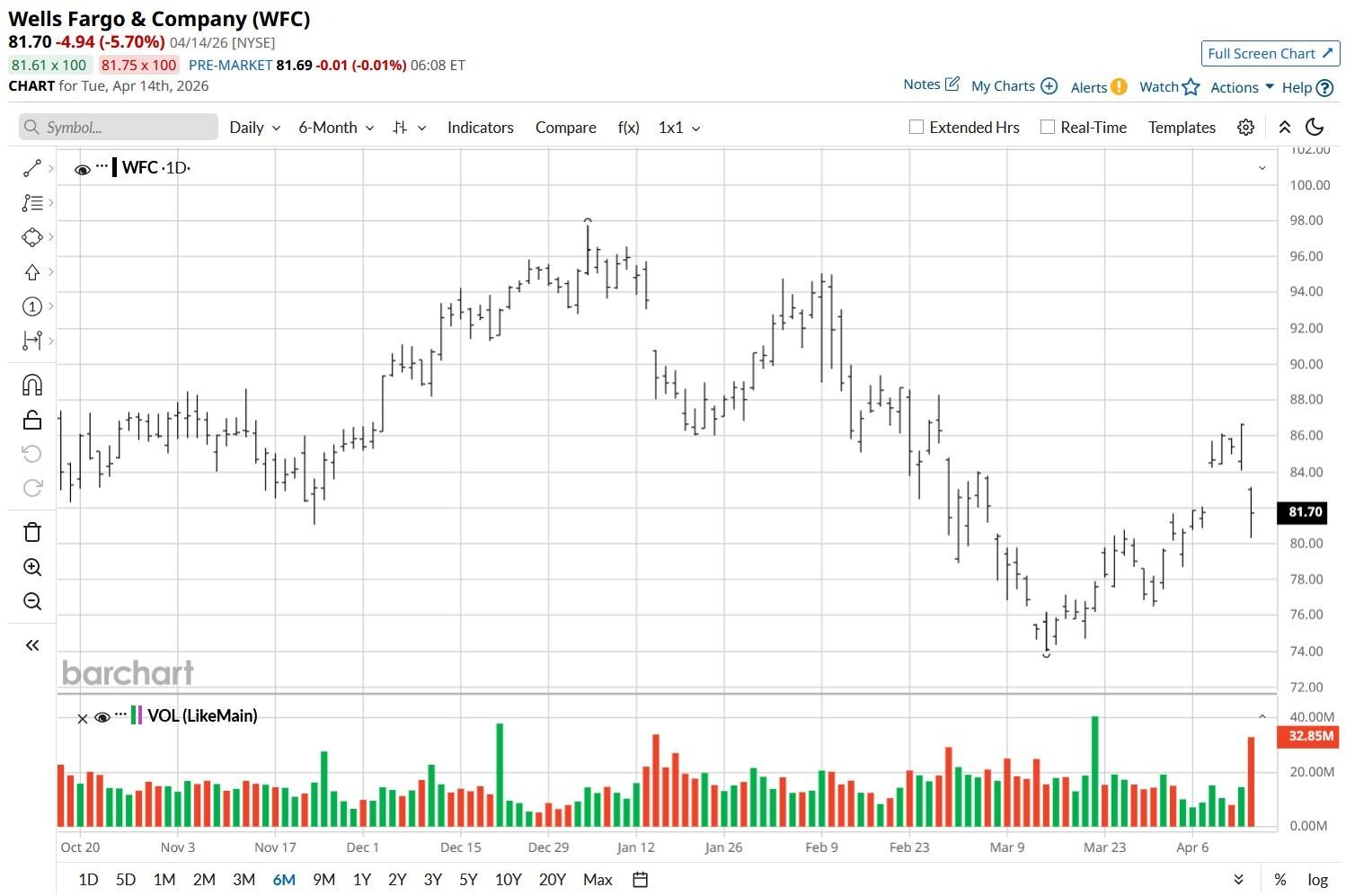

Investors are trimming exposure to Wells Fargo (WFC) after the Wall Street bank reported its fiscal Q1 results that missed expectations on both revenue and net interest income (NII).

The post-earnings decline saw WFC crash below its 50-day moving average (MA) on Tuesday, indicating selling pressure will likely continue in the near term.

Despite this pullback, however, Wells Fargo stock remains up roughly 10% versus its year-to-date low.

Does it Warrant Selling Wells Fargo Stock?

Despite headline weakness, the underlying business showed meaningful momentum.

Diluted earnings per share (EPS) went up 15%, and the bank returned $5.4 billion to shareholders, with more than half of it going to share repurchases.

Moreover, consumer checking and credit card account openings jumped over 15% and nearly 60%, respectively, while loan originations more than doubled to reflect the benefit of the regulatory asset cap removal in mid-2025.

WFC shares breaking below the 50-day MA is technically significant, but it must be viewed in the broader context: the stock is up some 30% over the past year and has roughly doubled over five years.

WFC Shares Are Trading at a Relative Discount

WFC management maintained its full-year NII guidance of about $50 billion and expense outlook of $55.7 billion, signaling confidence in the trajectory despite near-term margin pressures.

At the time of writing, Wells Fargo shares are trading at a forward price-to-earnings (P/E) multiple of about 12x, which signals a meaningful discount to peers like JPMorgan (JPM).

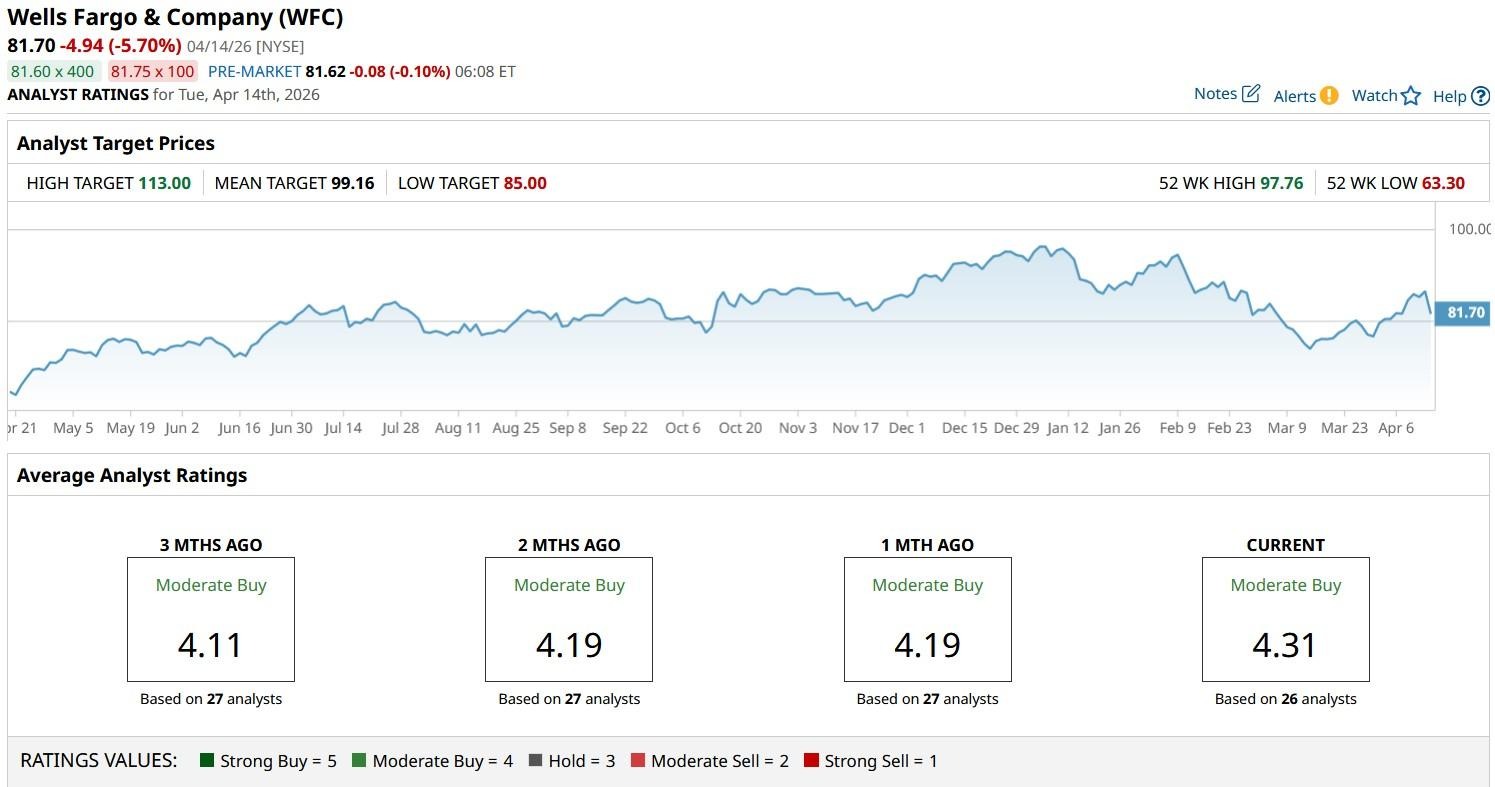

HSBC analysts recently upgraded the bank stock to “Buy,” citing valuation, national scale, and the transformative impact of the asset cap removal. Its $94 price target signals potential upside of some 15%.

Note that the bank’s artificial intelligence (AI) powered assistant, Fargo, has surpassed $1 billion in customer interactions, reflecting meaningful digital engagement gains as well.

How Wall Street Recommends Playing Wells Fargo

HSBC is actually among the more conservative Wall Street firms on Wells Fargo, especially since it continues to lower its headcount, demonstrating a commitment to efficiency amid aggressive tech investments.

The consensus rating on WFC stock sits at “Moderate Buy” currently, with the mean target of about $99 indicating potential upside of more than 20% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tesla Is Still a ‘Leader in Physical AI’ and You Should Buy TSLA Stock Now, Says UBS

- Turbine Season for Tech: John Rowland on the Next Era of AI Data Center Investments

- IonQ's DARPA Contract Win Makes It the Quantum Computing Stock to Own in 2026

- Lucid Keep Hitting New Lows: Should You Buy LCID Stock or Give Up?