The artificial intelligence (AI) boom is looking very different from the early days of the generative AI craze. Back then, GPUs grabbed most of the attention because they powered the training and inferencing of massive AI models. But as the industry moves deeper into the world of agentic AI – where systems can reason, make decisions, and execute tasks more independently – CPUs are becoming just as important. These AI agents constantly rely on CPUs to manage workflows, coordinate operations, and handle real-time updates behind the scenes.

That shift is also changing data center architecture, with the traditional model of one CPU supporting several GPUs gradually moving closer to a one-to-one balance. As CPU demand accelerates alongside AI adoption, companies like Advanced Micro Devices (AMD) are emerging as key beneficiaries of this next phase of AI infrastructure growth.

AMD designs high-performance CPUs and GPUs used across data centers, AI systems, PCs, and gaming devices, but lately, its server CPU business has been stealing the show. That momentum became impossible to ignore after AMD’s stellar first-quarter results. Server compute revenue surged over 50% annually, driven by stronger-than-expected demand for AI compute racks and data center deployments. Plus, server growth is anticipated to “accelerate meaningfully,” with the total addressable market projected to grow over 35% annually and surpass $120 billion by 2030. Even better, AMD’s management expects this demand cycle to continue through 2026 and into 2027.

That growing momentum, alongside changing AI infrastructure dynamics, is exactly why analysts are turning bullish on AMD now. Evercore ISI lifted its Street-high price target to $579 from $358 and maintained an “Outperform” rating, saying agentic AI workloads are dramatically increasing CPU demand alongside GPUs, expanding AMD’s long-term growth opportunity. Plus, many analysts still believe the market has not fully grasped how large the long-term opportunity around server CPUs and AI infrastructure could become.

So, with AMD stock gaining fresh momentum after the quarterly report, the chip giant once again finds itself at the center of the AI conversation. Let’s take a closer look at the chip giant.

About Advanced Micro Devices Stock

Founded in Santa Clara, California, AMD has evolved from a longtime chip challenger into one of the biggest forces powering the modern AI era. With a market capitalization of $665.9 billion, the company builds the processors and accelerators that run everything from cloud platforms and AI data centers to gaming consoles and next-generation PCs.

Its EPYC server chips have become increasingly popular among hyperscalers and enterprise customers looking for powerful and energy-efficient computing solutions, while AMD’s Instinct AI accelerators are helping the company expand deeper into large-scale AI infrastructure. As demand rises for more intelligent and connected computing systems, AMD is positioning itself as a full-stack AI player with technologies spanning CPUs, GPUs, networking, and software.

The market’s excitement around AMD stock has been hard to ignore lately. Over the past year, AMD shares have surged 334.23%, massively outperforming the broader market as investors piled into anything tied to AI infrastructure and high-performance computing. In the past six months alone, the stock jumped 89.1%, fueled by growing confidence in AMD’s expanding role across data centers and enterprise AI.

There have been a few bumps along the way. Rising geopolitical tensions and volatility across global markets briefly pressured semiconductor stocks in 2026, including AMD. But failed to fully derail the chip giant’s momentum. AMD stock is still up 106.2% year-to-date (YTD). In fact, the shares almost doubled within a month and recently touched a fresh high of $430.60 on May 6 following the company’s blockbuster first-quarter 2026 earnings report.

The rally has been so sharp that some technical indicators are starting to flash signs of overheating. AMD’s 14-day RSI has climbed to 79.63, a level that usually suggests the stock may be due for a breather after such a massive run. Meanwhile, rising green trading volumes show buyers are still aggressively chasing the momentum. Adding to that bullish backdrop, the MACD line has crossed above the signal line, typically seen as a sign that upward momentum remains firmly in control for now.

Of course, a rally this big comes with a price tag. AMD is no longer the kind of semiconductor stock investors can call “cheap,” with shares now trading at 70.55 times forward adjusted earnings and 13.53 times forward sales. That’s well above many sector peers and even AMD’s own historical averages.

But right now, the market seems willing to pay that premium because investors see AMD as one of the companies sitting closest to the center of the AI infrastructure boom. If AMD keeps growing revenue at a strong pace and continues gaining ground in AI data centers, today’s expensive-looking valuation may not feel nearly as stretched a few years from now.

A Snapshot of AMD’s Q1 Report

AMD unveiled its first-quarter 2026 results on May 5, and the numbers were strong across the board. Revenue jumped 37.8% year-over-year (YOY) to $10.25 billion, beating expectations, while non-GAAP EPS climbed 42.7% annually to $1.37. And once again, AMD’s data center business stood out, where the AI spending wave just keeps getting bigger. Data Center revenue surged 57.2% YOY to a record $5.8 billion, driven by incredibly strong demand for both its EPYC server CPUs and Instinct AI GPUs, as cloud companies and enterprises continue building out AI infrastructure at full speed.

But one of the more interesting topics the management talked about was the evolution of AI demand. It’s no longer just about stuffing data centers with GPUs. As AI systems become more complex, companies also need powerful CPUs to manage, orchestrate, and support those workloads. AMD believes that shift is creating another huge opportunity for its EPYC processors, especially as agentic AI and real-world inference workloads start scaling.

CEO Lisa Su also talked about growing engagement with both hyperscalers and enterprise customers, which shows AMD’s AI push is broadening well beyond a handful of early adopters.

Outside the data center business, AMD still saw healthy growth in its other segments too, like its client and gaming revenue, which grew 22.6% YOY to $3.6 billion, while Embedded revenue rose 6.1% annually to $873 million as demand improved across several end markets.

Additionally, margins moved higher, which is what one would want to see when a company shifts more heavily toward premium AI products. Non-GAAP gross margin expanded 180 basis points to 55.4%, helped largely by the stronger data center mix. Adjusted EBITDA climbed 40.5% YOY to $2.75 billion, while EBITDA margin improved to 26.8%.

Meanwhile, AMD is spending aggressively to keep up with the AI race. Non-GAAP operating expenses climbed to $3.15 billion as AMD ramped up investments in R&D and go-to-market efforts tied to its expanding AI roadmap. Even with all that spending, AMD ended the quarter with $12.35 billion in cash, cash equivalents, and short-term investments, while total debt amounted to $3.2 billion. Operating cash flow rose to $2.96 billion during Q1, and free cash flow increased to $2.57 billion from $2.08 billion in Q4 2025. AMD also continued buying back stock aggressively, returning $1.1 billion to shareholders through repurchases during the quarter.

During the Q1 earnings call, one of the most eye-catching announcements was about its partnership with Meta (META). Meta plans to deploy up to 6 gigawatts of AMD Instinct GPUs across its AI data centers under a multiyear agreement. The first delivery alone involves one gigawatt built around a custom version of AMD’s Instinct MI450-based GPU. Meta will be a lead customer for AMD’s next-generation sixth-gen EPYC processors. That’s a pretty major signal that AMD is becoming deeply embedded inside the AI infrastructure plans of some of the world’s largest tech companies.

Further, management spent time talking about its upcoming Helios rack-scale AI system and Instinct MI450 accelerator, both of which appear to be gaining traction. The Helios platform remains on track to reach customers before the end of 2026. And while AI demand remains incredibly strong, AMD admitted the environment is getting tighter from a supply-chain perspective. The management said that the company is actively expanding wafer supply and back-end capacity to keep up with growing customer demand.

Looking ahead, AMD’s Q2 guidance suggested the momentum is still building. The management expects Q2 revenue of around $11.2 billion, plus or minus $300 million. At the midpoint, that would represent roughly 46% annual growth. Growth is projected to continue being led by the Data Center segment, alongside strength in Client and Gaming and double-digit growth in Embedded.

Meanwhile, analysts tracking AMD expect Q2 EPS to be $1.23, up 355.6% YOY. Looking further ahead, profit is anticipated to jump nearly 82% to $5.95 per share in fiscal 2026 and surge another 61.2% in fiscal 2027 to $9.59 per share.

What Do Analysts Expect for AMD Stock?

Wall Street has turned increasingly bullish on AMD, especially after the company’s blockbuster Q1 report reinforced the idea that CPUs are becoming just as critical as GPUs in the emerging agentic AI era.

Wedbush’s Matt Bryson said the company “delivered in spades,” pointing to server compute revenue growth. He noted that demand for AI compute racks is helping drive both unit growth and higher pricing. Bryson believes this momentum is only getting started, with AMD expecting server CPU growth to remain strong in the future. The analyst maintained his “Outperform” rating and lifted the price target to $450 from $400.

Meanwhile, Jefferies analyst Kevin Garrigan said server CPUs may have stolen the spotlight, but AMD’s GPU business could still be heading into another major growth phase. He highlighted the upcoming MI450 and Helios ramp in the second half of 2026, adding that customer demand is already running ahead of initial expectations. Garrigan reiterated his “Buy” rating and sharply raised his price target to $415 from $300.

Even Morgan Stanley’s Joseph Moore acknowledged that enthusiasm around CPUs keeps building. He said the “world has changed,” arguing AMD remains in a strong position to gain market share. Moore raised his target to $410 from $360 and believes in “the AMD CPU story,” especially as the company targets the majority server CPU share by 2030.

KeyBanc got even more bullish on AMD, hiking its price target to $530 from $330 while keeping an “Overweight” rating. The brokerage firm pointed to blowout Q1 results and stronger Q2 guidance.

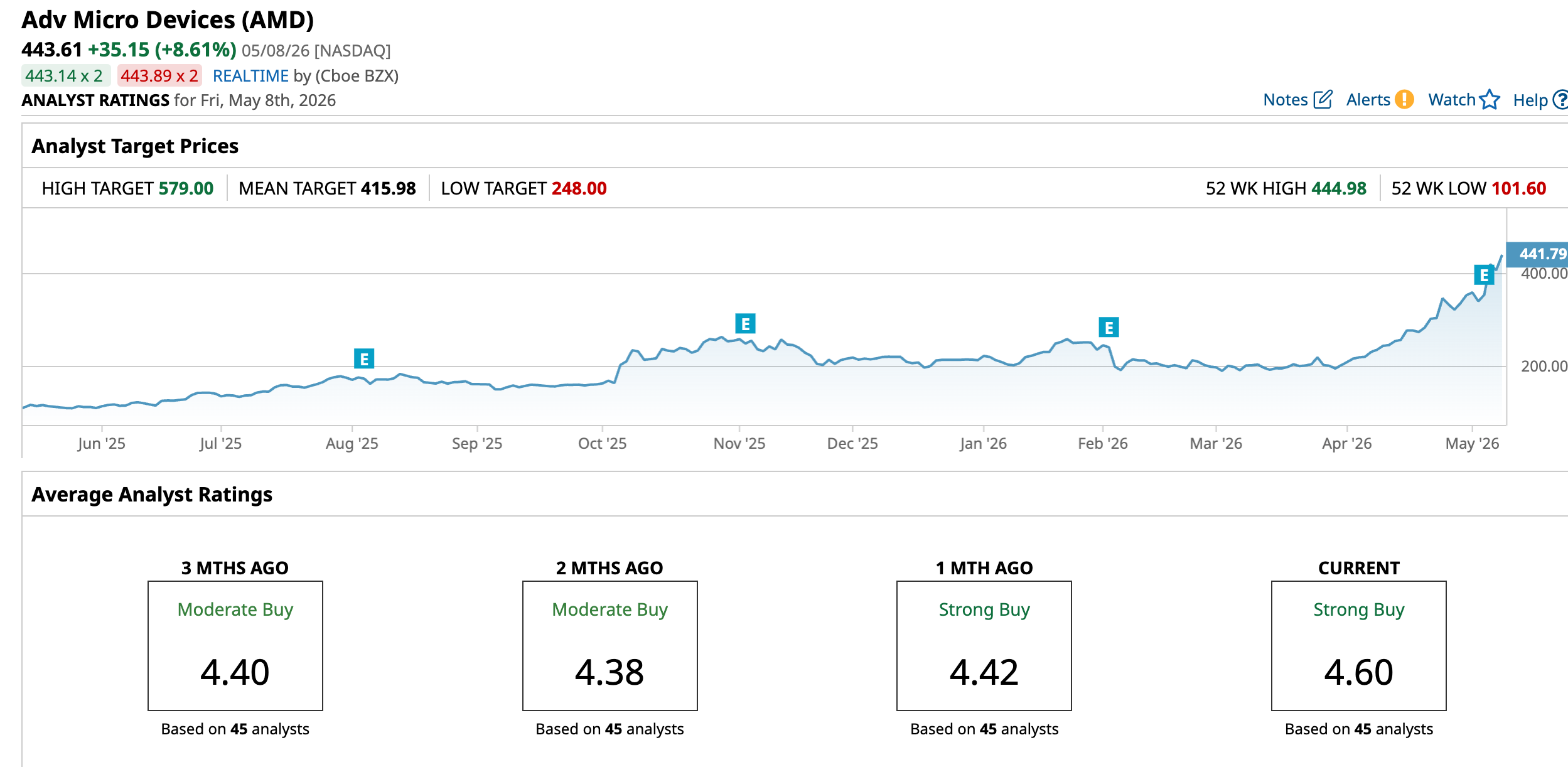

The stock carries a “Strong Buy” consensus overall – an upgrade from a “Moderate Buy” rating two months ago. Among the 45 analysts tracking the stock, 35 issue a “Strong Buy,” two give a “Moderate Buy,” and eight advise a “Hold.”

The stock’s average analyst price target of $415.98 has already been surpassed, but Evercore ISI’s Street-high target of $579 suggests that the chip stock can still rally as much as 30.5% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart