Since October 2025, Peabody Energy has been in a holding pattern, posting a small loss of 3.8% while floating around $27.25. The stock also fell short of the S&P 500’s 6.1% gain during that period.

Is there a buying opportunity in Peabody Energy, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Peabody Energy Will Underperform?

We're sitting this one out for now. Here are three reasons there are better opportunities than BTU and a stock we'd rather own.

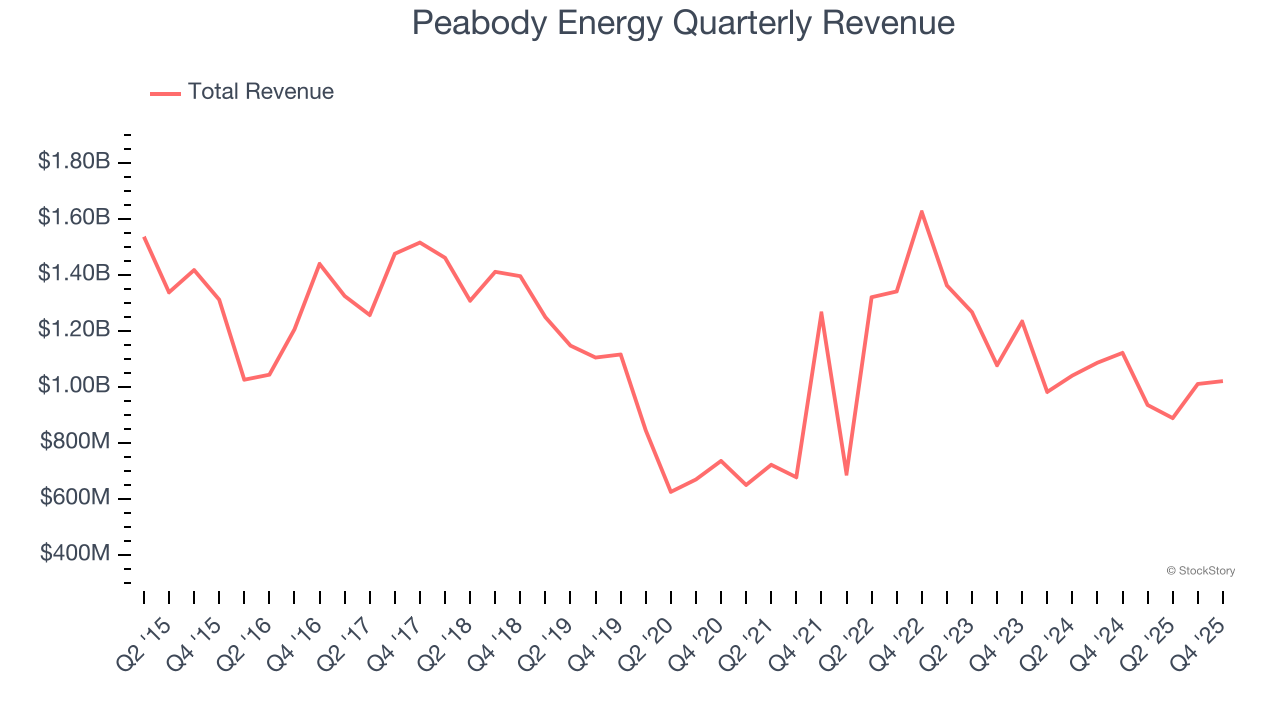

1. Long-Term Revenue Growth Disappoints

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Unfortunately, Peabody Energy’s 6% annualized revenue growth over the last five years was sluggish. This was below our standard for the energy upstream and integrated energy sector.

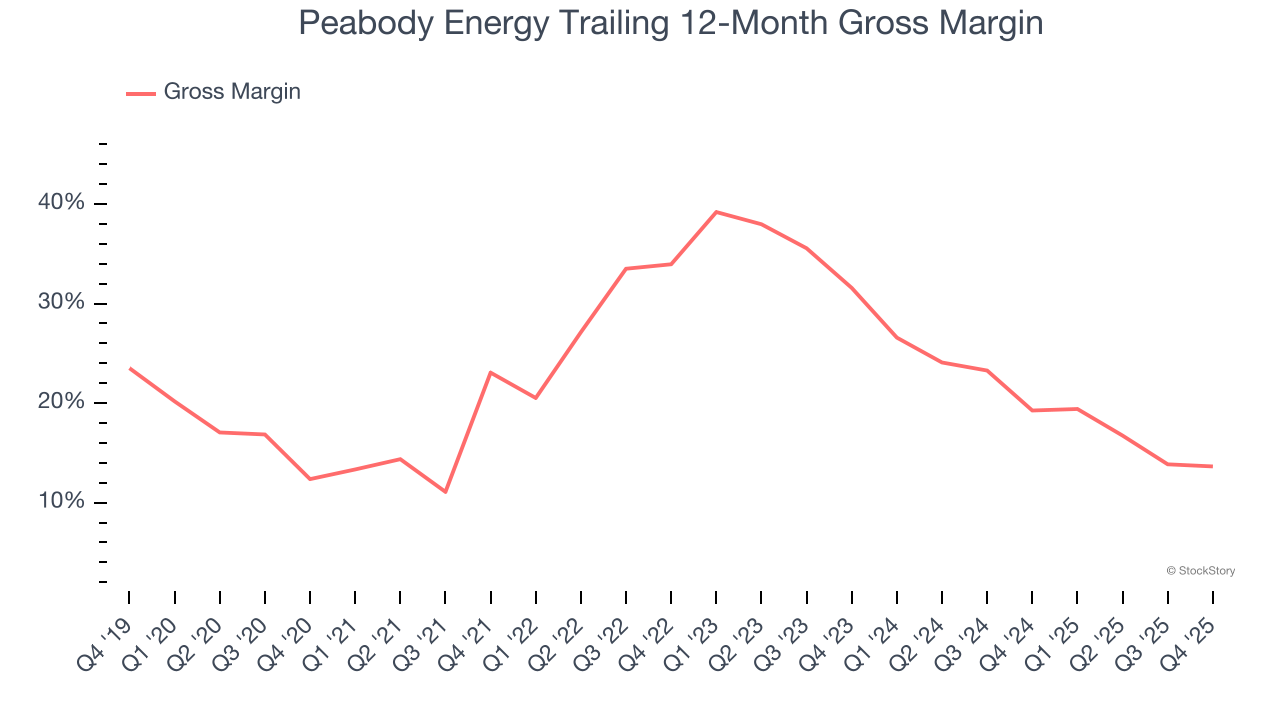

2. Low Gross Margin Reveals Weak Structural Profitability

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Peabody Energy, which averaged 25.1% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

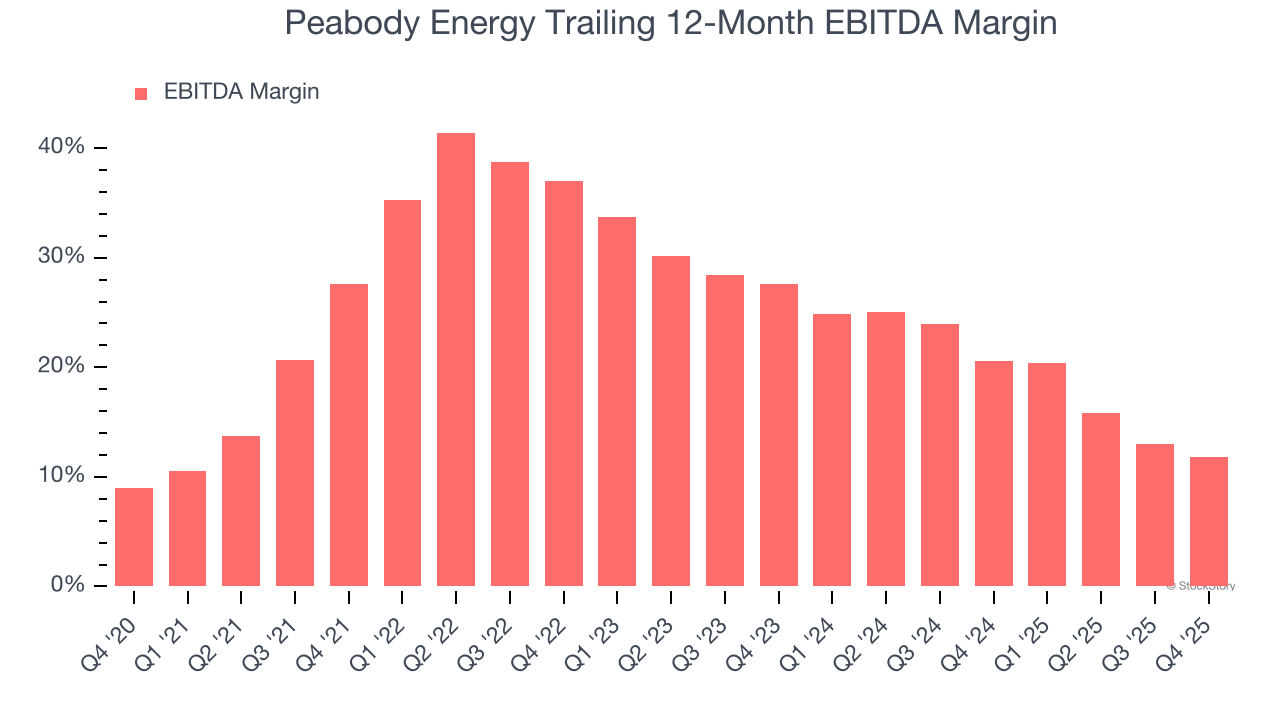

3. Shrinking EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Looking at the trend in its profitability, Peabody Energy’s EBITDA margin decreased by 15.8 percentage points over the last year. Peabody Energy’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its EBITDA margin for the trailing 12 months was 11.8%.

Final Judgment

We see the value of companies helping consumers, but in the case of Peabody Energy, we’re out. With its shares lagging the market recently, the stock trades at 8.7× forward P/E (or $27.25 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Peabody Energy

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.