Regional banking company Flagstar Financial (NYSE: FLG) fell short of the market’s revenue expectations in Q1 CY2026 as sales only rose 1.6% year on year to $498 million. Its non-GAAP profit of $0.04 per share was in line with analysts’ consensus estimates.

Is now the time to buy Flagstar Financial? Find out by accessing our full research report, it’s free.

Flagstar Financial (FLG) Q1 CY2026 Highlights:

- Net Interest Income: $443 million vs analyst estimates of $474.9 million (8% year-on-year growth, 6.7% miss)

- Net Interest Margin: 2.2% vs analyst estimates of 2.3% (10.4 basis point miss)

- Revenue: $498 million vs analyst estimates of $553 million (1.6% year-on-year growth, 9.9% miss)

- Adjusted EPS: $0.04 vs analyst estimates of $0.04 (in line)

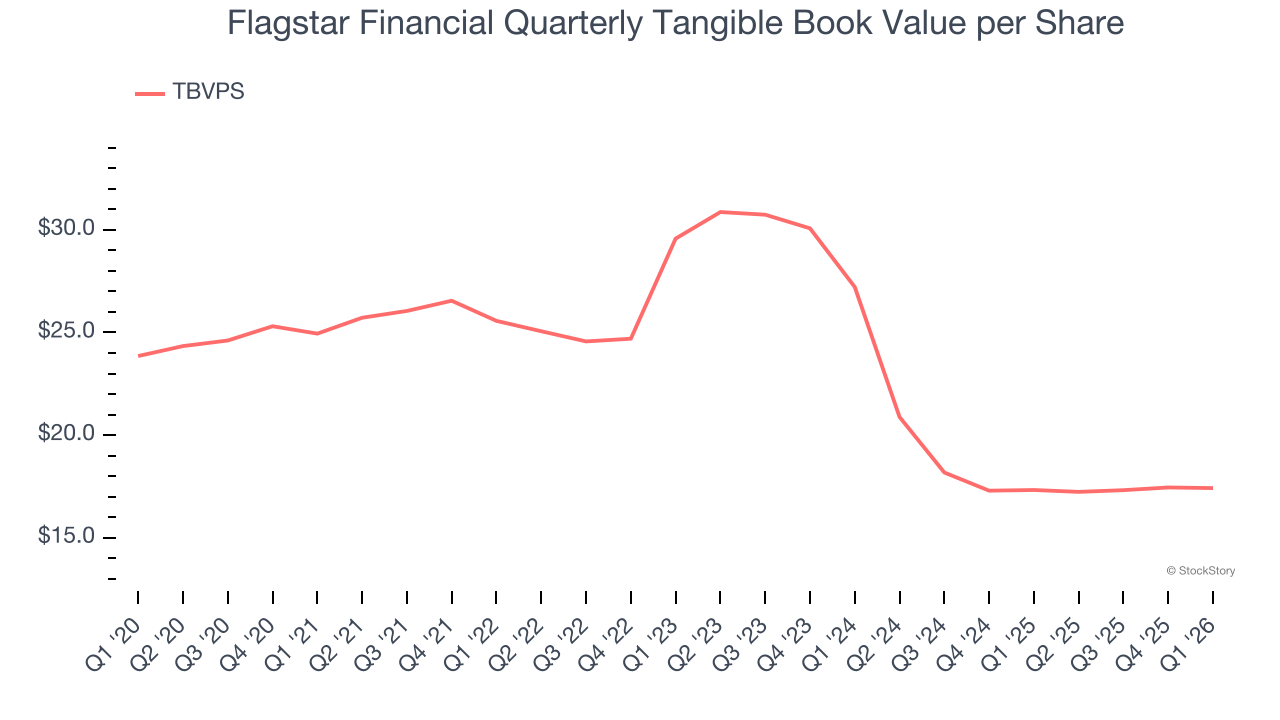

- Tangible Book Value per Share: $17.42 vs analyst estimates of $17.23 (flat year on year, 1.1% beat)

- Market Capitalization: $5.97 billion

Commenting on the Bank's first quarter performance, Chairman, President, and Chief Executive Officer, Joseph M. Otting stated, "We are pleased to report another quarter of solid progress, highlighted by our second consecutive quarter of profitability and continued momentum across our core banking franchise. We reported net income attributable to common stockholders of $13 million, or $0.03 per diluted share on a GAAP basis and net income attributable to common stockholders of $20 million or $0.04 per diluted share on an adjusted basis. Our first quarter 2026 performance reflects the disciplined execution of our strategic plan and improving fundamentals, including strong C&I loan growth, a higher level of deposits, additional progress in reducing the level of non-accrual and criticized/classified loans, further expansion of our net interest margin, and a strong capital position.

Company Overview

Tracing its roots back to 1859 and rebranded from New York Community Bancorp in 2024, Flagstar Financial (NYSE: FLG) is a bank holding company that offers commercial and consumer banking services, with specialties in multi-family lending, mortgage originations, and warehouse lending.

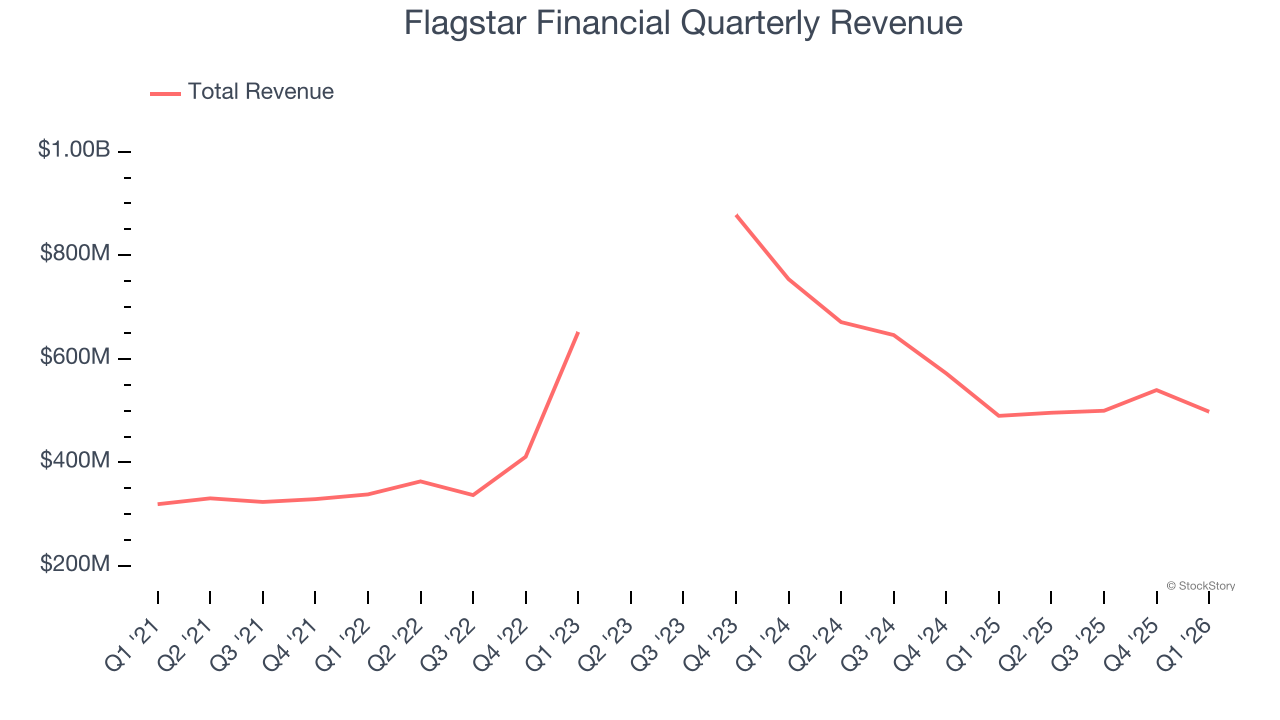

Sales Growth

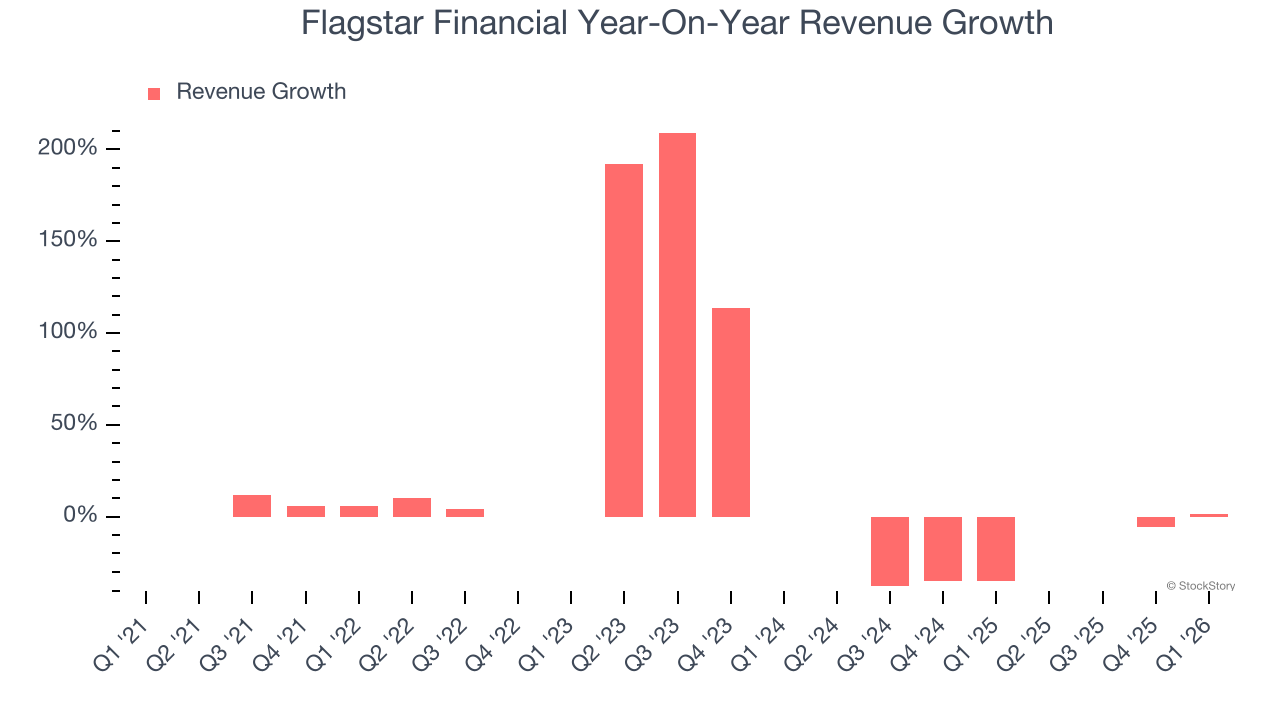

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Luckily, Flagstar Financial’s revenue grew at a decent 11.3% compounded annual growth rate over the last five years. Its growth was slightly above the average banking company and shows its offerings resonate with customers.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Flagstar Financial’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 26.2% over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Flagstar Financial’s revenue grew by 1.6% year on year to $498 million, falling short of Wall Street’s estimates.

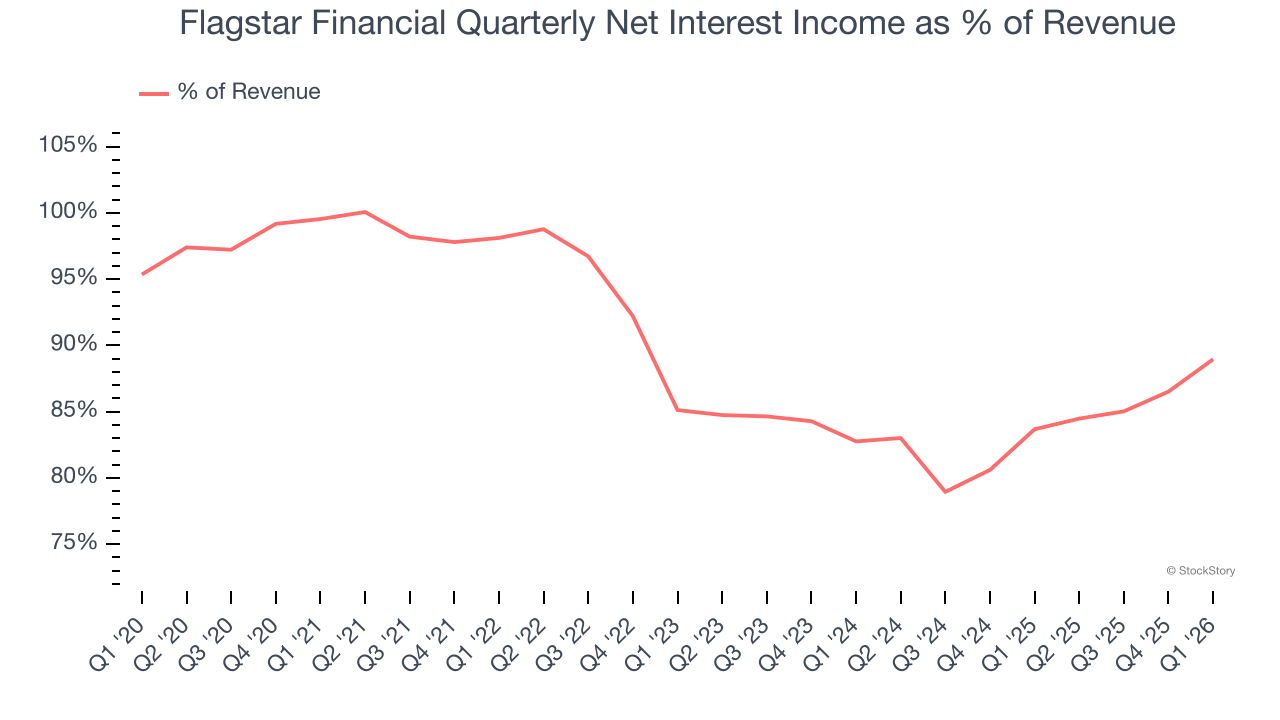

Net interest income made up 88.7% of the company’s total revenue during the last five years, meaning Flagstar Financial barely relies on non-interest income to drive its overall growth.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Flagstar Financial’s TBVPS declined at a 6.9% annual clip over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 20% annually over the last two years ($27.22 to $17.42 per share).

Over the next 12 months, Consensus estimates call for Flagstar Financial’s TBVPS to grow by 5.3% to $18.34, lousy growth rate.

Key Takeaways from Flagstar Financial’s Q1 Results

It was encouraging to see Flagstar Financial meet analysts’ EPS expectations this quarter. We were also happy its tangible book value per share narrowly outperformed Wall Street’s estimates. On the other hand, its revenue missed and its net interest income fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $14.35 immediately after reporting.

Should you buy the stock or not? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).