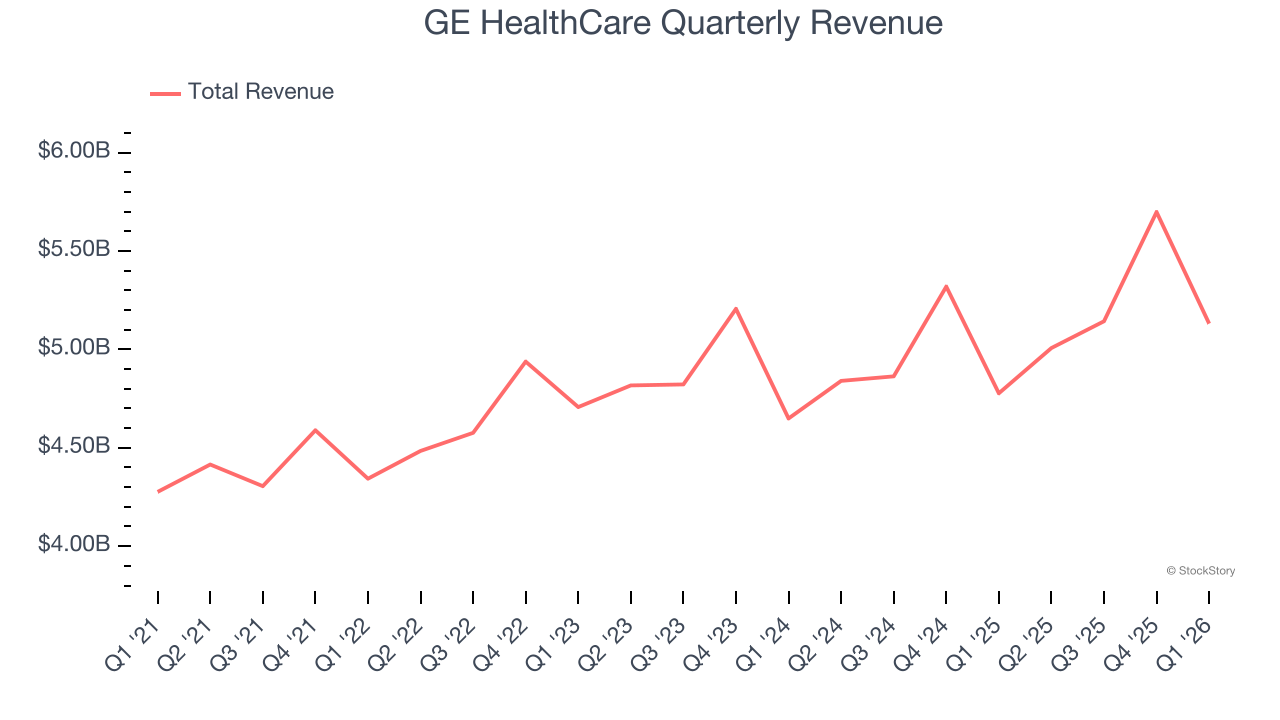

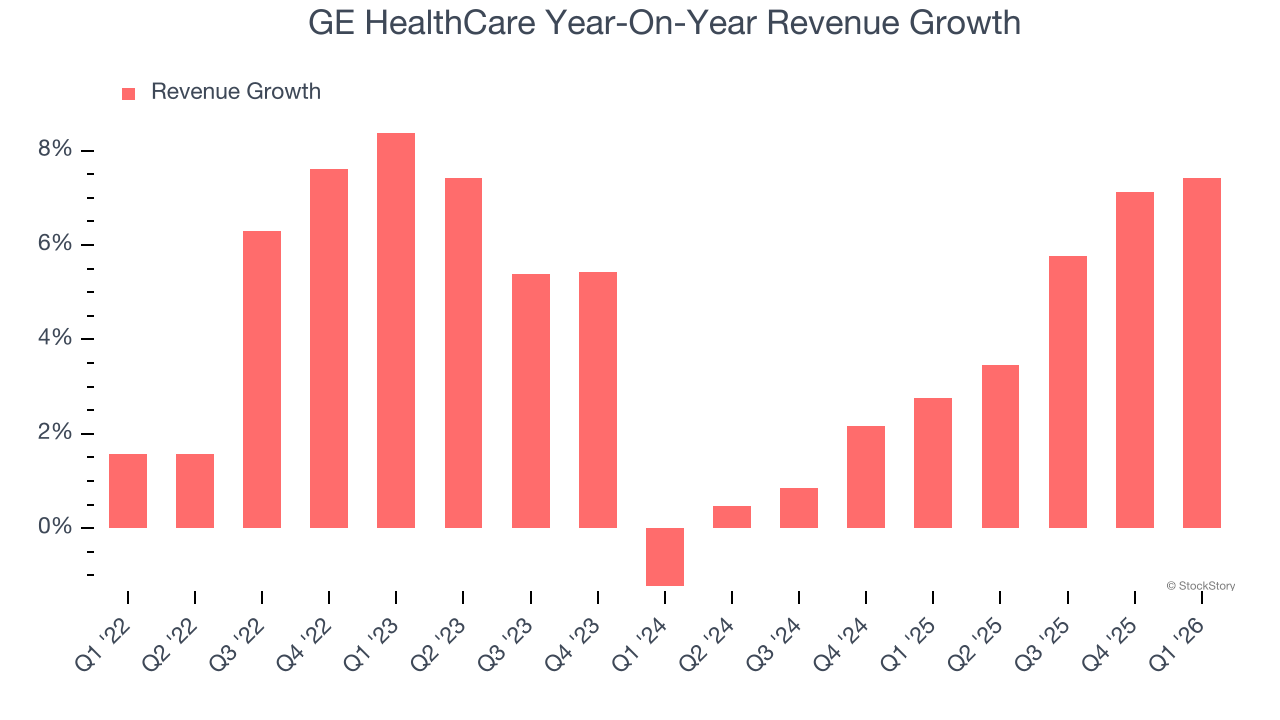

Healthcare technology company GE HealthCare Technologies (NASDAQ: GEHC) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 7.4% year on year to $5.13 billion. Its non-GAAP profit of $0.99 per share was 5.7% below analysts’ consensus estimates.

Is now the time to buy GE HealthCare? Find out by accessing our full research report, it’s free.

GE HealthCare (GEHC) Q1 CY2026 Highlights:

- Revenue: $5.13 billion vs analyst estimates of $5.02 billion (7.4% year-on-year growth, 2.1% beat)

- Adjusted EPS: $0.99 vs analyst expectations of $1.05 (5.7% miss)

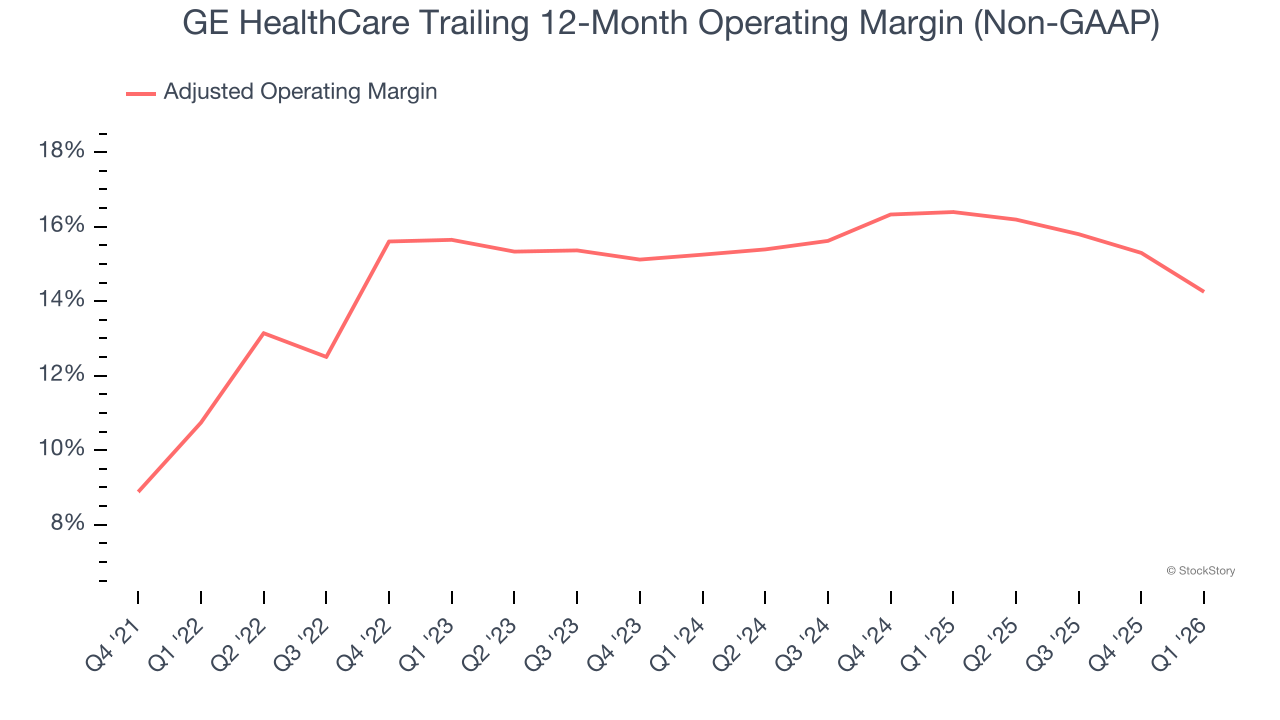

- Adjusted Operating Income: $550 million vs analyst estimates of $726.7 million (10.7% margin, 24.3% miss)

- Management lowered its full-year Adjusted EPS guidance to $4.90 at the midpoint, a 3% decrease

- Operating Margin: 10%, down from 13.2% in the same quarter last year

- Free Cash Flow Margin: 2.2%, similar to the same quarter last year

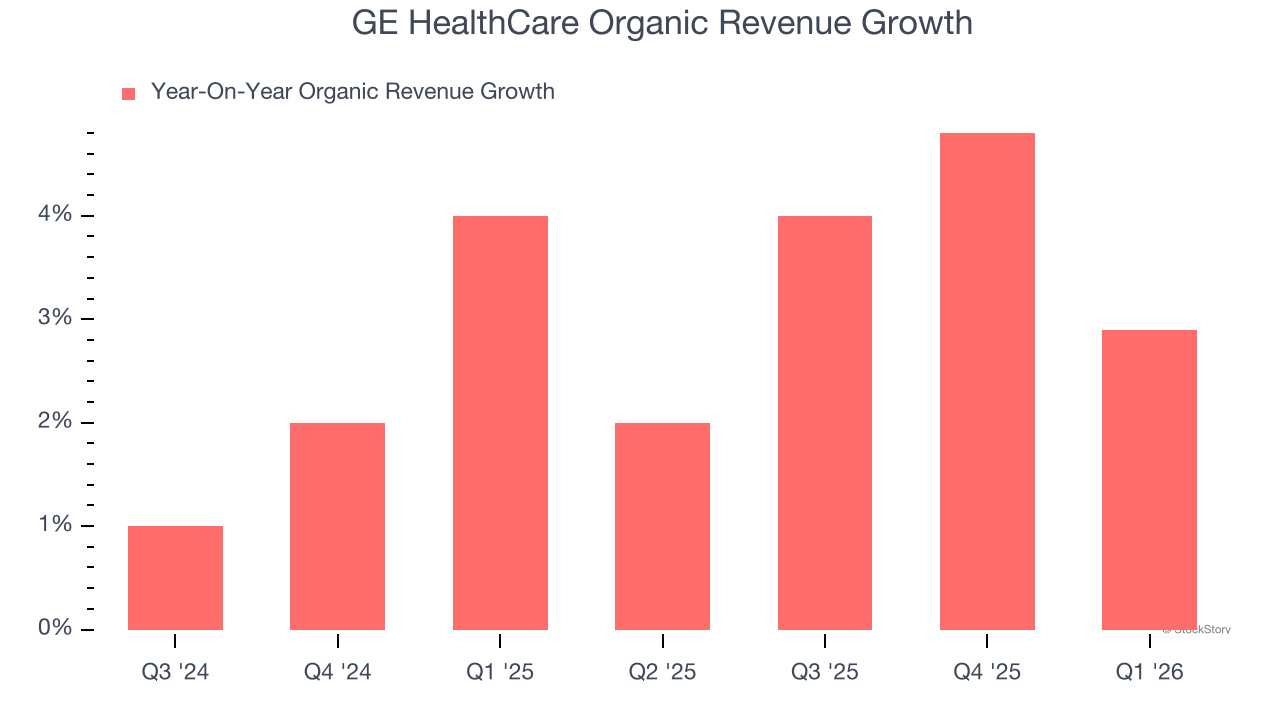

- Organic Revenue rose 2.9% year on year (beat)

- Market Capitalization: $31.26 billion

GE HealthCare President and CEO Peter Arduini said, “As we start the year, we’re pleased with topline performance, which came in at the high end of our expectations. Growth was driven by strong commercial execution in Pharmaceutical Diagnostics, including Flyrcado, Advanced Visualization Solutions, and Imaging, as well as services. We are maintaining our topline growth guidance driven by healthy customer demand globally.

Company Overview

Spun off from industrial giant General Electric in 2023 after over a century as its healthcare division, GE HealthCare (NASDAQ: GEHC) provides medical imaging equipment, patient monitoring systems, diagnostic pharmaceuticals, and AI-enabled healthcare solutions to hospitals and clinics worldwide.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, GE HealthCare’s sales grew at a mediocre 4.4% compounded annual growth rate over the last four years. This fell short of our benchmark for the healthcare sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. GE HealthCare’s annualized revenue growth of 3.7% over the last two years aligns with its four-year trend, suggesting its demand was consistently weak.

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, GE HealthCare’s organic revenue averaged 3% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, GE HealthCare reported year-on-year revenue growth of 7.4%, and its $5.13 billion of revenue exceeded Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

GE HealthCare has done a decent job managing its cost base over the last five years. The company has produced an average adjusted operating margin of 14.5%, higher than the broader healthcare sector.

Analyzing the trend in its profitability, GE HealthCare’s adjusted operating margin rose by 3.5 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, GE HealthCare generated an adjusted operating margin profit margin of 10.7%, down 4.2 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

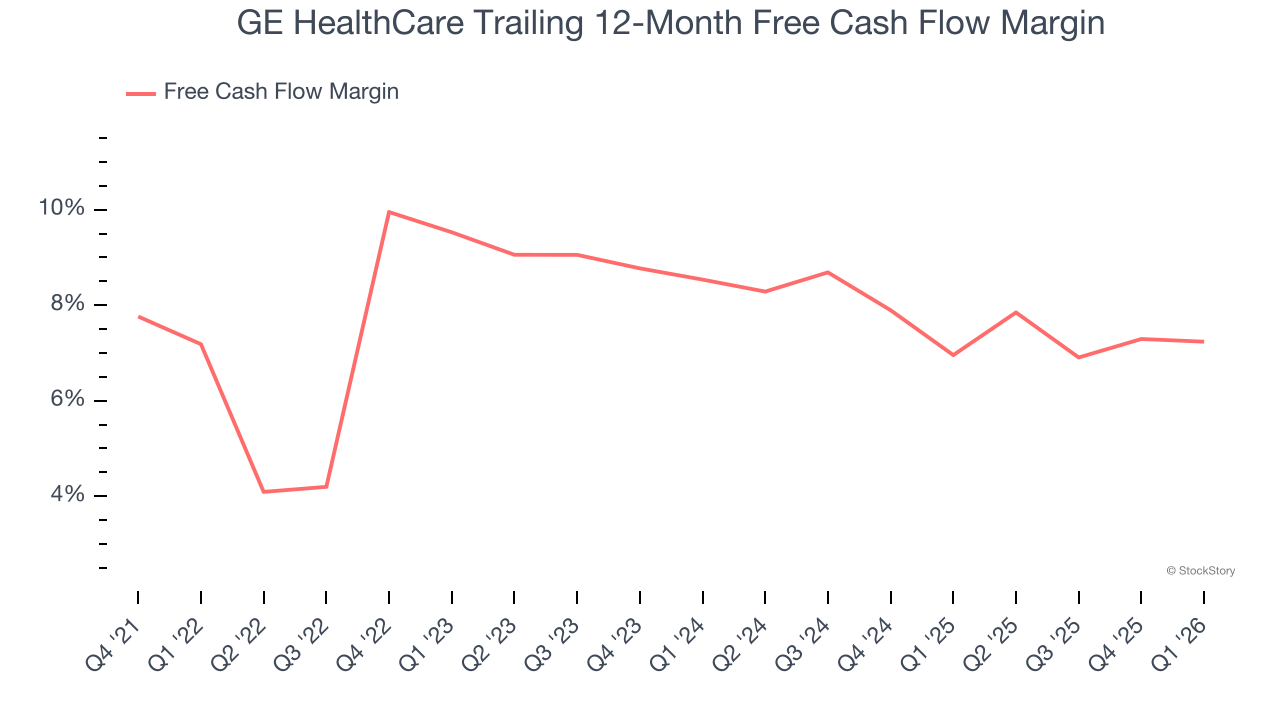

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

GE HealthCare has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.9% over the last five years, slightly better than the broader healthcare sector.

GE HealthCare’s free cash flow clocked in at $112 million in Q1, equivalent to a 2.2% margin. This cash profitability was in line with the comparable period last year but below its five-year average. In a silo, this isn’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from GE HealthCare’s Q1 Results

It was encouraging to see GE HealthCare beat analysts’ revenue expectations this quarter. We were also happy its organic revenue was in line with Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.1% to $65.02 immediately after reporting.

GE HealthCare’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).