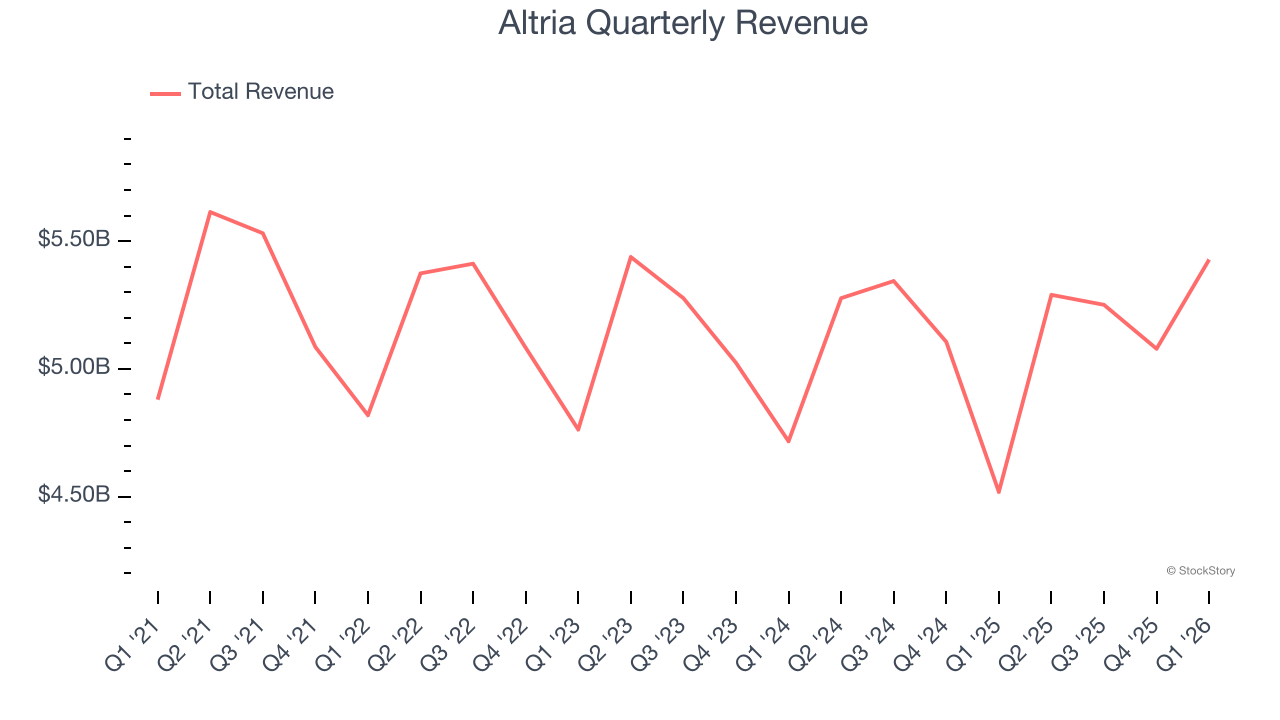

Tobacco company Altria (NYSE: MO) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 20.1% year on year to $5.43 billion. Its non-GAAP profit of $1.32 per share was 5.9% above analysts’ consensus estimates.

Is now the time to buy Altria? Find out by accessing our full research report, it’s free.

Altria (MO) Q1 CY2026 Highlights:

- Revenue: $5.43 billion vs analyst estimates of $4.57 billion (20.1% year-on-year growth, 18.6% beat)

- Adjusted EPS: $1.32 vs analyst estimates of $1.25 (5.9% beat)

- Adjusted Operating Income: $3.03 billion vs analyst estimates of $2.83 billion (55.9% margin, 7.2% beat)

- Management reiterated its full-year Adjusted EPS guidance of $5.64 at the midpoint

- Operating Margin: 55.9%, up from 39.6% in the same quarter last year

- Market Capitalization: $114 billion

“We delivered a strong start to the year, growing adjusted diluted EPS by 7.3% in the first quarter,” said Billy Gifford, Altria’s Chief Executive Officer.

Company Overview

Best known for its Marlboro brand of cigarettes, Altria (NYSE: MO) offers tobacco and nicotine products.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $21.05 billion in revenue over the past 12 months, Altria is one of the most widely recognized consumer staples companies. Its influence over consumers gives it negotiating leverage with distributors, enabling it to pick and choose where it sells its products (a luxury many don’t have). However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To accelerate sales, Altria likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Altria struggled to increase demand as its $21.05 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a poor baseline for our analysis.

This quarter, Altria reported robust year-on-year revenue growth of 20.1%, and its $5.43 billion of revenue topped Wall Street estimates by 18.6%.

Looking ahead, sell-side analysts expect revenue to decline by 3.5% over the next 12 months, a deceleration versus the last three years. This projection doesn't excite us and suggests its products will face some demand challenges. At least the company is tracking well in other measures of financial health.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

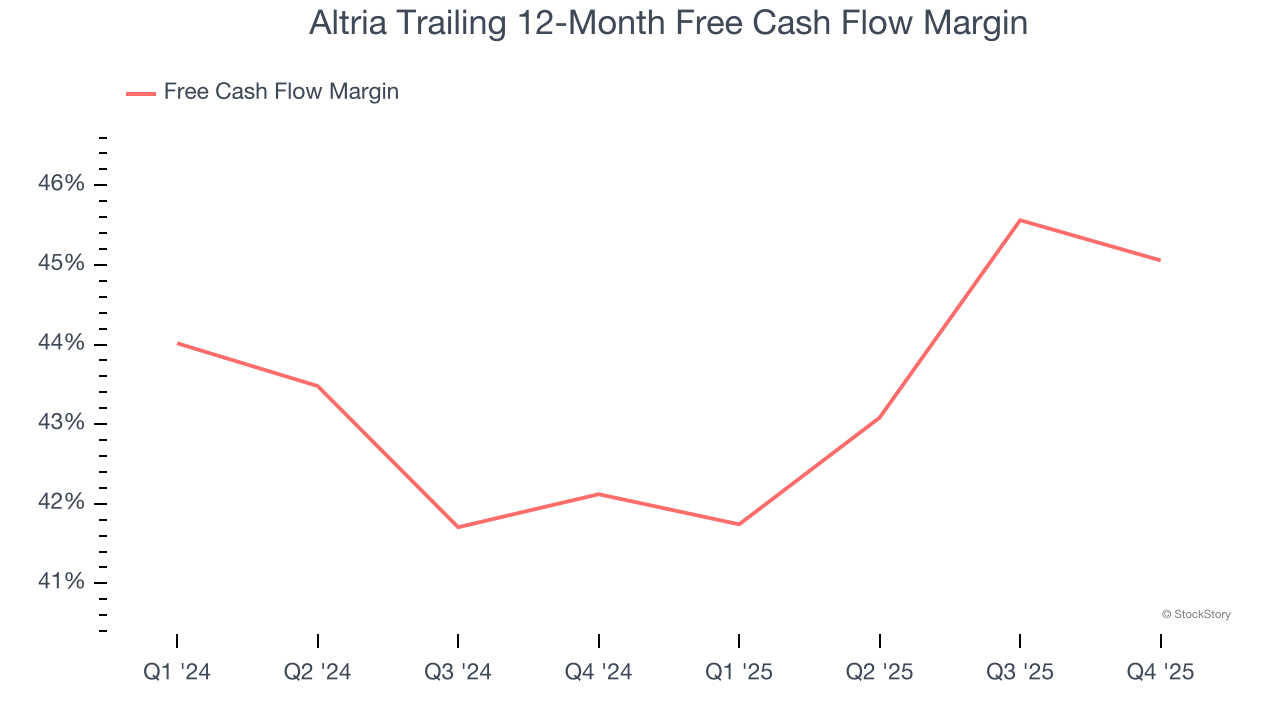

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Altria has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging an eye-popping 41.4% over the last two years.

Key Takeaways from Altria’s Q1 Results

We were impressed by how significantly Altria blew past analysts’ revenue expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 2.1% to $69.62 immediately following the results.

Altria put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).