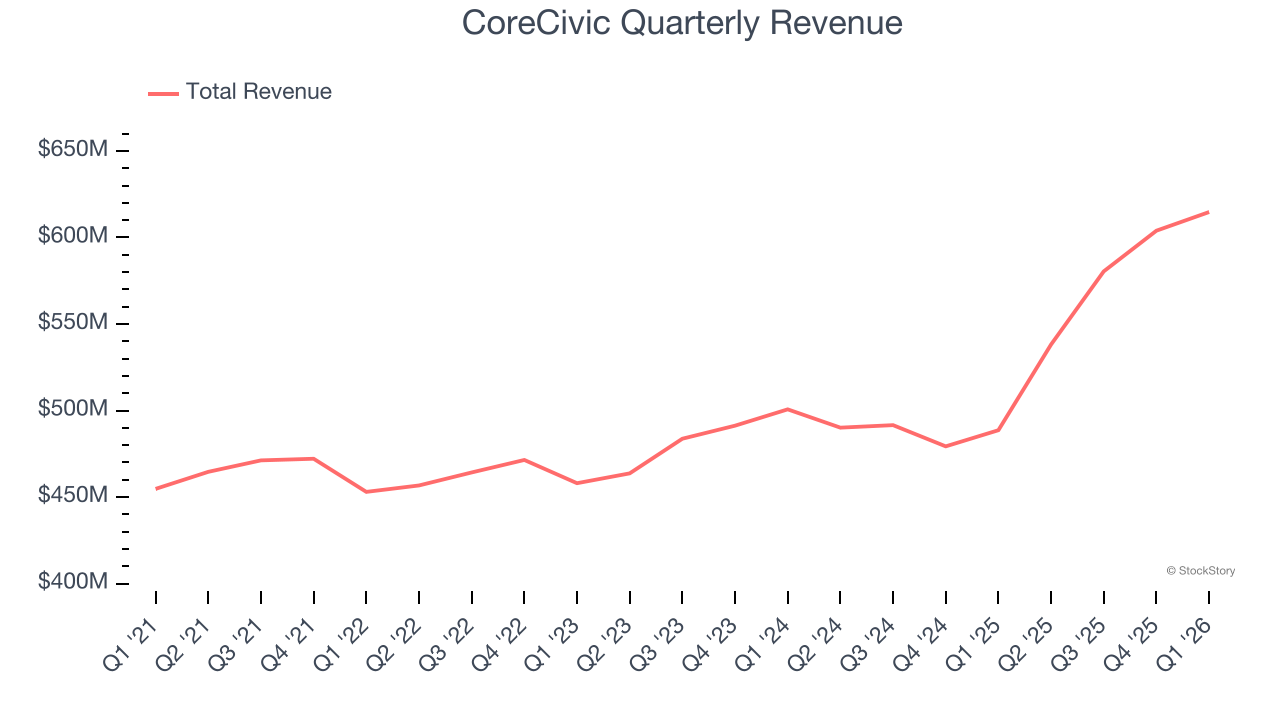

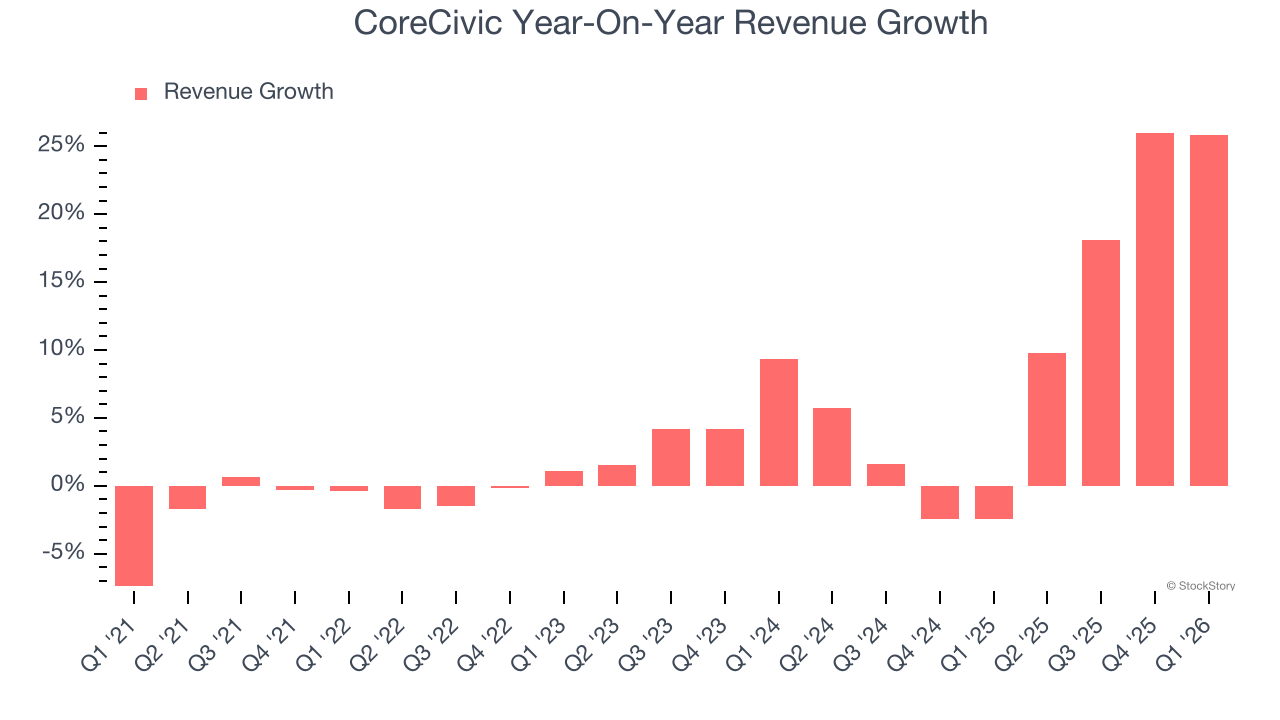

Private prison operator CoreCivic (NYSE: CXW) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 25.8% year on year to $614.7 million. Its non-GAAP profit of $0.40 per share was 35.6% above analysts’ consensus estimates.

Is now the time to buy CoreCivic? Find out by accessing our full research report, it’s free.

CoreCivic (CXW) Q1 CY2026 Highlights:

- Revenue: $614.7 million vs analyst estimates of $603.4 million (25.8% year-on-year growth, 1.9% beat)

- Adjusted EPS: $0.40 vs analyst estimates of $0.30 (35.6% beat)

- Adjusted EBITDA: $110.1 million vs analyst estimates of $96.75 million (17.9% margin, 13.8% beat)

- Adjusted EPS guidance for the full year is $1.58 at the midpoint, missing analyst estimates by 2%

- EBITDA guidance for the full year is $455.3 million at the midpoint, above analyst estimates of $446.2 million

- Market Capitalization: $1.92 billion

Company Overview

Originally founded in 1983 as the first private prison company in the United States, CoreCivic (NYSE: CXW) operates correctional facilities, detention centers, and residential reentry programs for government agencies across the United States.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $2.34 billion in revenue over the past 12 months, CoreCivic is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, CoreCivic grew its sales at a mediocre 4.6% compounded annual growth rate over the last five years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. CoreCivic’s annualized revenue growth of 9.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, CoreCivic reported robust year-on-year revenue growth of 25.8%, and its $614.7 million of revenue topped Wall Street estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 13.3% over the next 12 months, an improvement versus the last two years. This projection is admirable and suggests its newer products and services will catalyze better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

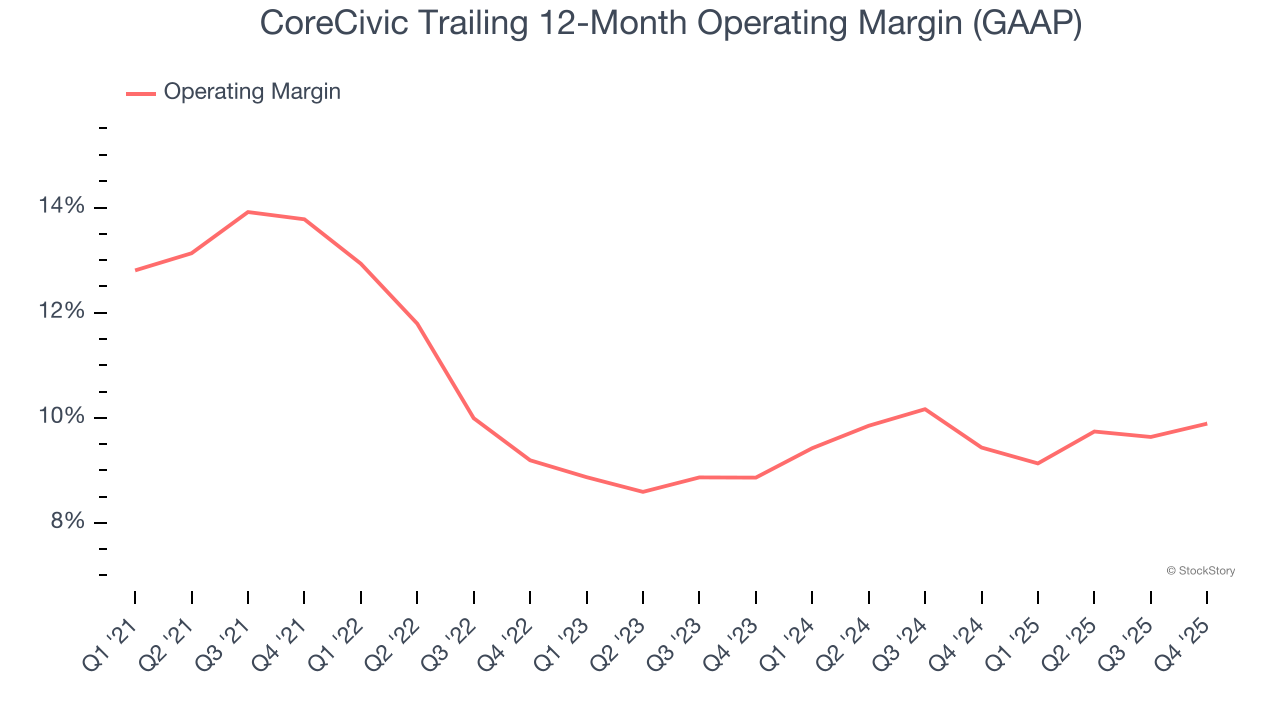

Operating Margin

CoreCivic has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.1%, higher than the broader business services sector.

Looking at the trend in its profitability, CoreCivic’s operating margin decreased by 3.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

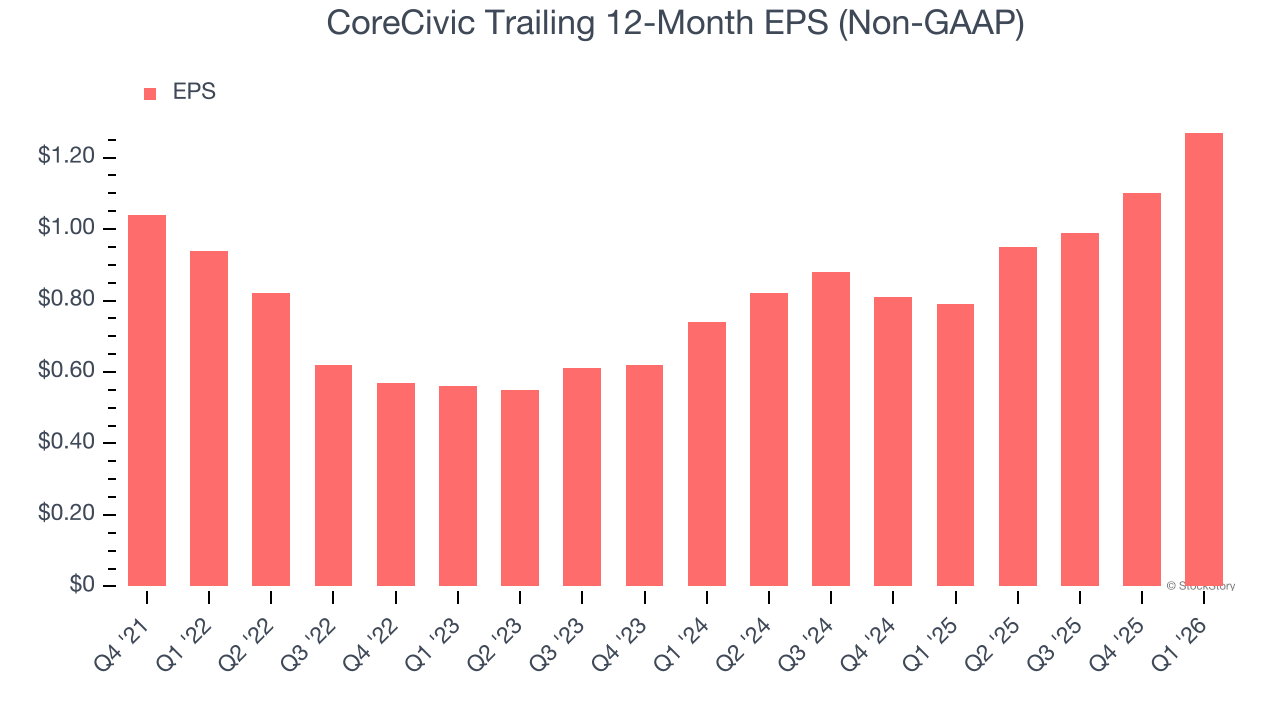

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

CoreCivic’s full-year EPS grew at a decent 7.8% compounded annual growth rate over the last four years, in line with the broader business services sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

CoreCivic’s EPS grew at an astounding 31% compounded annual growth rate over the last two years, higher than its 9.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

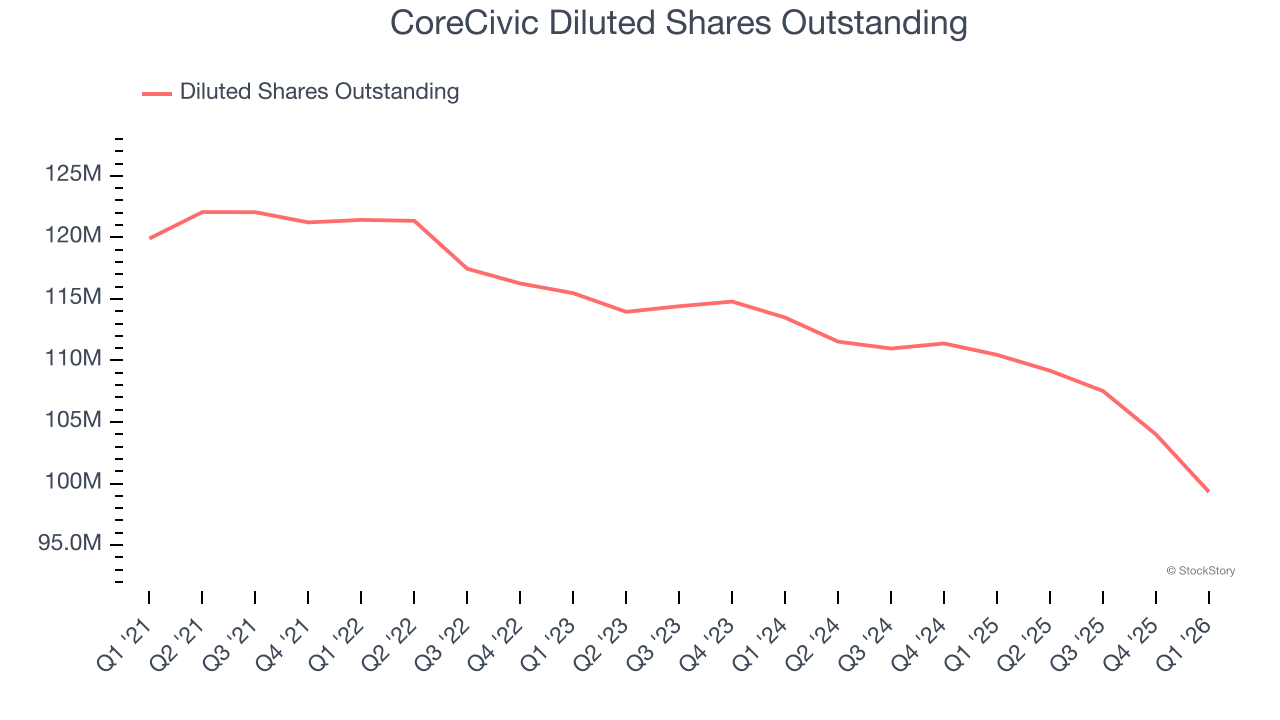

We can take a deeper look into CoreCivic’s earnings to better understand the drivers of its performance. A two-year view shows that CoreCivic has repurchased its stock, shrinking its share count by 12.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, CoreCivic reported adjusted EPS of $0.40, up from $0.23 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from CoreCivic’s Q1 Results

It was good to see CoreCivic beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Overall, this print had some key positives. The stock traded up 4% to $22.01 immediately after reporting.

Indeed, CoreCivic had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).