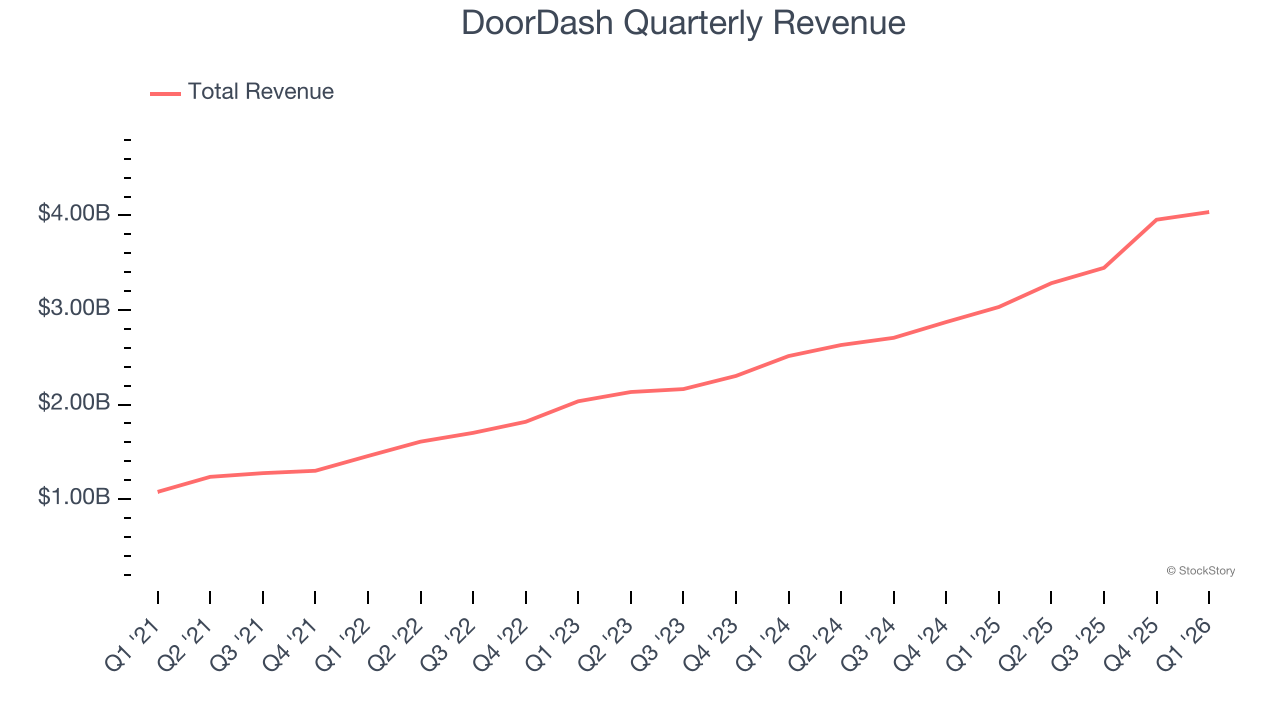

On-demand food delivery service DoorDash (NASDAQ: DASH) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 33.1% year on year to $4.04 billion. Its GAAP profit of $0.42 per share was 15.4% above analysts’ consensus estimates.

Is now the time to buy DoorDash? Find out by accessing our full research report, it’s free.

DoorDash (DASH) Q1 CY2026 Highlights:

- Revenue: $4.04 billion vs analyst estimates of $4.15 billion (33.1% year-on-year growth, 2.8% miss)

- EPS (GAAP): $0.42 vs analyst estimates of $0.36 (15.4% beat)

- Adjusted EBITDA: $754 million vs analyst estimates of $741.5 million (18.7% margin, 1.7% beat)

- Marketplace GOV guidance for Q2 CY2026 is $32.9 billion at the midpoint, above analyst estimates of $32.4 billion

- EBITDA guidance for Q2 CY2026 is $820 million at the midpoint, below analyst estimates of $825.9 million

- Operating Margin: 3.7%, down from 5.1% in the same quarter last year

- Free Cash Flow Margin: 10.4%, up from 6.4% in the previous quarter

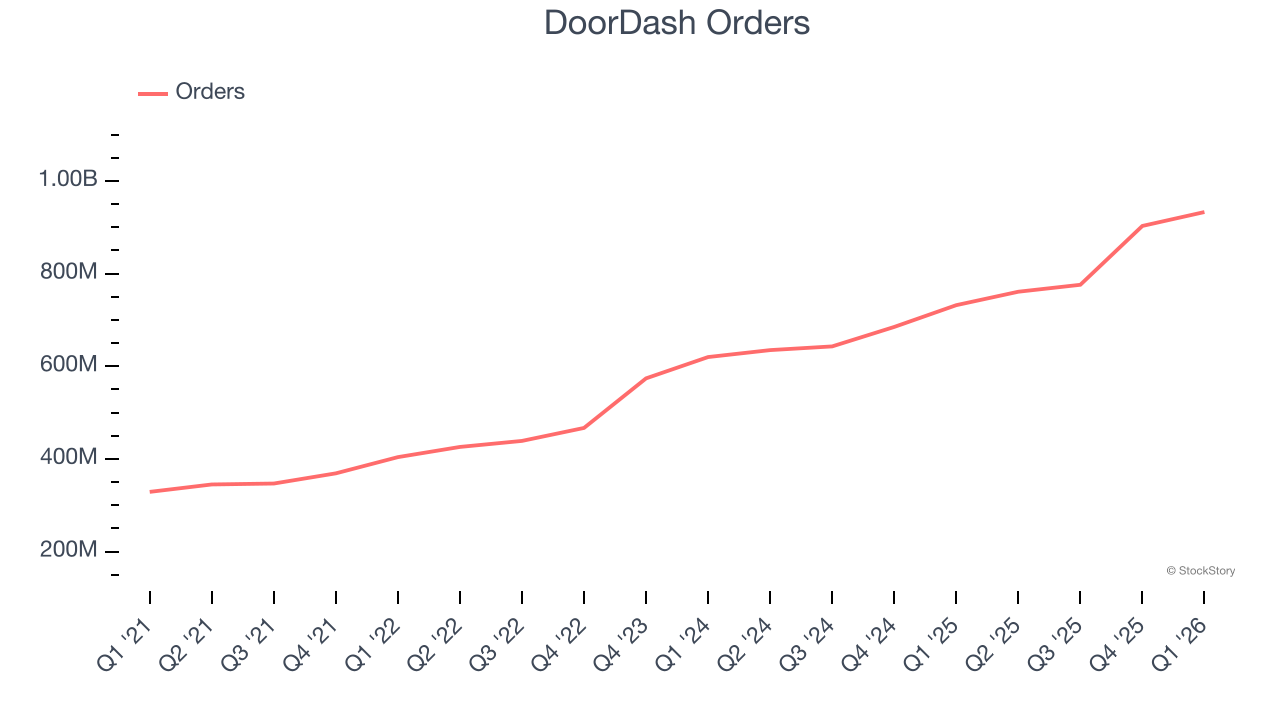

- Orders: 933 million, up 201 million year on year

- Market Capitalization: $72.39 billion

Company Overview

Founded by Stanford students with the intent to build “the local, on-demand FedEx", DoorDash (NASDAQ: DASH) operates an on-demand food delivery platform.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last three years, DoorDash grew its sales at an exceptional 27.1% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, DoorDash pulled off a wonderful 33.1% year-on-year revenue growth rate, but its $4.04 billion of revenue fell short of Wall Street’s rosy estimates.

Looking ahead, sell-side analysts expect revenue to grow 27% over the next 12 months, similar to its three-year rate. This projection is eye-popping for a company of its scale and suggests the market is baking in success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Orders

Request Growth

As a gig economy marketplace, DoorDash generates revenue growth by expanding the number of services on its platform (e.g. rides, deliveries, freelance jobs) and raising the commission fee from each service provided.

Over the last two years, DoorDash’s orders, a key performance metric for the company, increased by 22.9% annually to 933 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q1, DoorDash added 201 million orders, leading to 27.5% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating request growth.

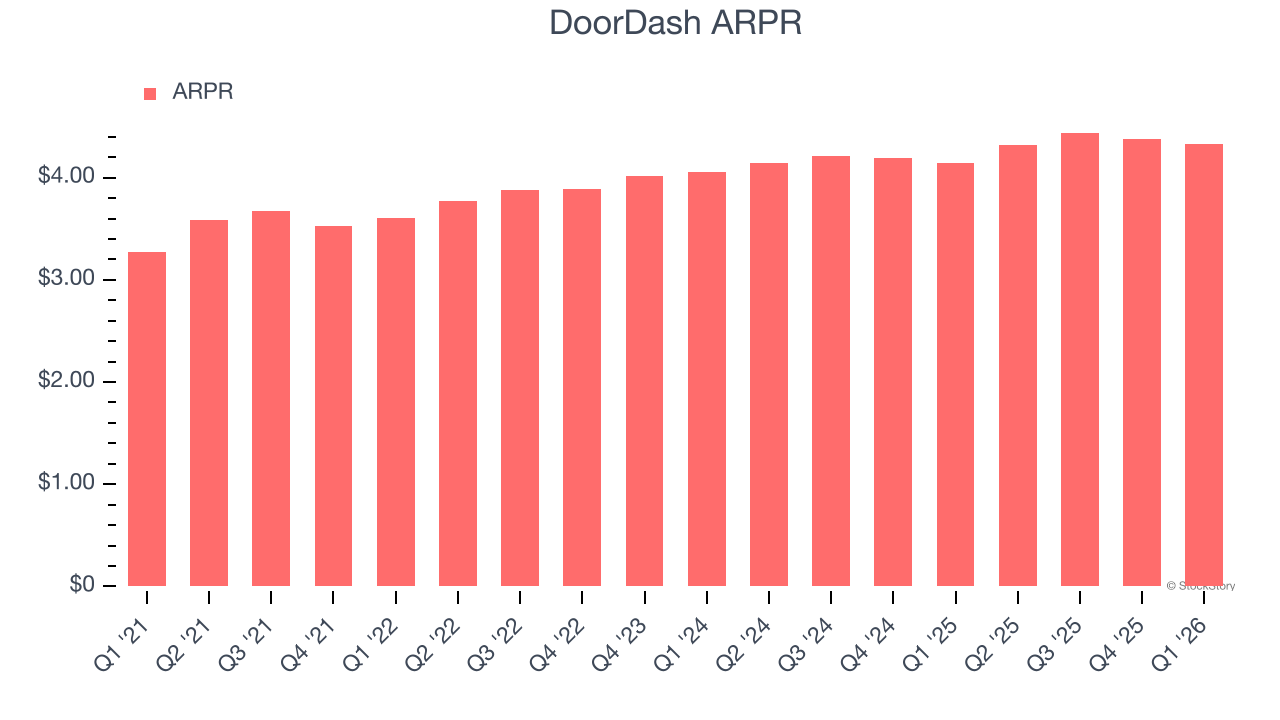

Revenue Per Request

Average revenue per request (ARPR) is a critical metric to track because it measures how much the company earns in transaction fees from each request. This number also informs us about DoorDash’s take rate, which represents its pricing leverage over the ecosystem, or "cut" from each transaction.

DoorDash’s ARPR growth has been mediocre over the last two years, averaging 4.2%. This isn’t great, but the increase in orders is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if DoorDash tries boosting ARPR by taking a more aggressive approach to monetization, it’s unclear whether requests can continue growing at the current pace.

This quarter, DoorDash’s ARPR clocked in at $4.33. It grew by 4.4% year on year, slower than its request growth.

Key Takeaways from DoorDash’s Q1 Results

We enjoyed seeing DoorDash increase its number of requests this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Looking ahead, GOV guidance for next quarter was above expectations. On the other hand, its revenue missed and its EBITDA guidance for next quarter fell slightly short of Wall Street’s estimates. Overall, this was a mixed quarter. Still, the stock traded up 10.2% to $185.56 immediately after reporting due to low expectations about the health of the consumer with the war in Iran and higher energy prices acting as headwinds to discretionary spending.

Big picture, is DoorDash a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).