Tax preparation company H&R Block (NYSE: HRB) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 5.3% year on year to $2.40 billion. The company’s full-year revenue guidance of $3.92 billion at the midpoint came in 0.7% above analysts’ estimates. Its non-GAAP profit of $6.02 per share was 4.3% above analysts’ consensus estimates.

Is now the time to buy H&R Block? Find out by accessing our full research report, it’s free.

H&R Block (HRB) Q1 CY2026 Highlights:

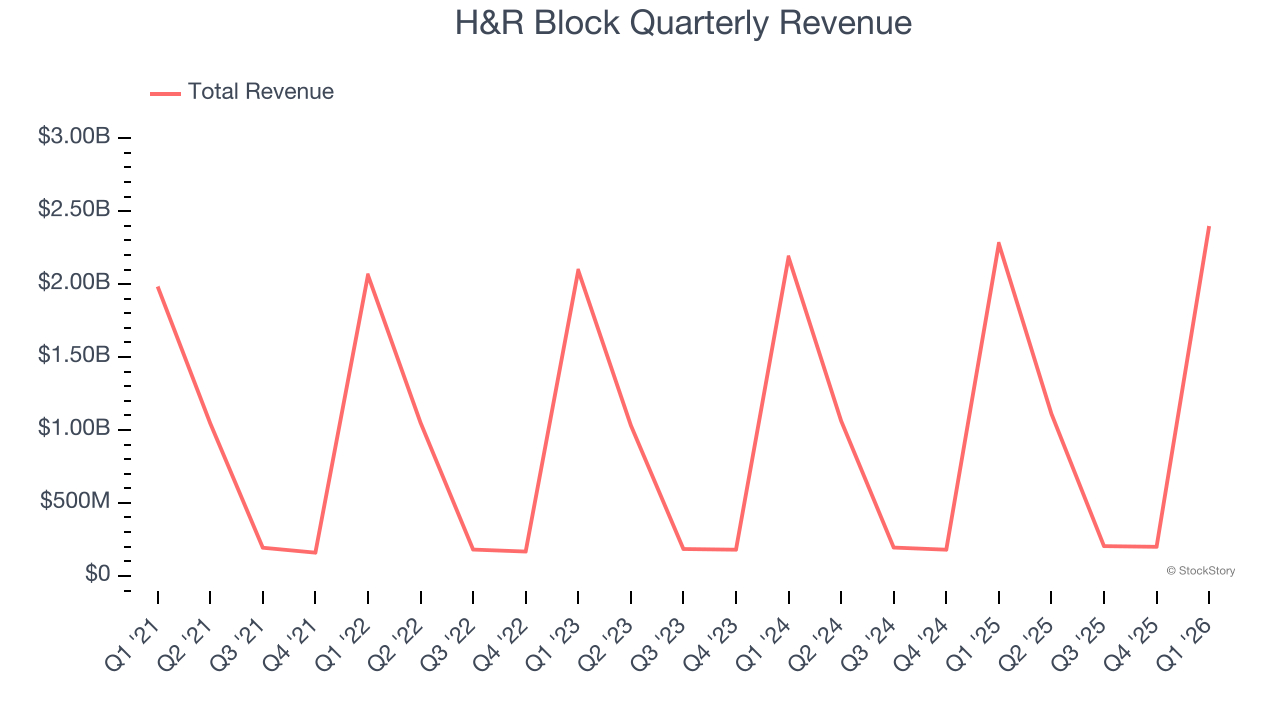

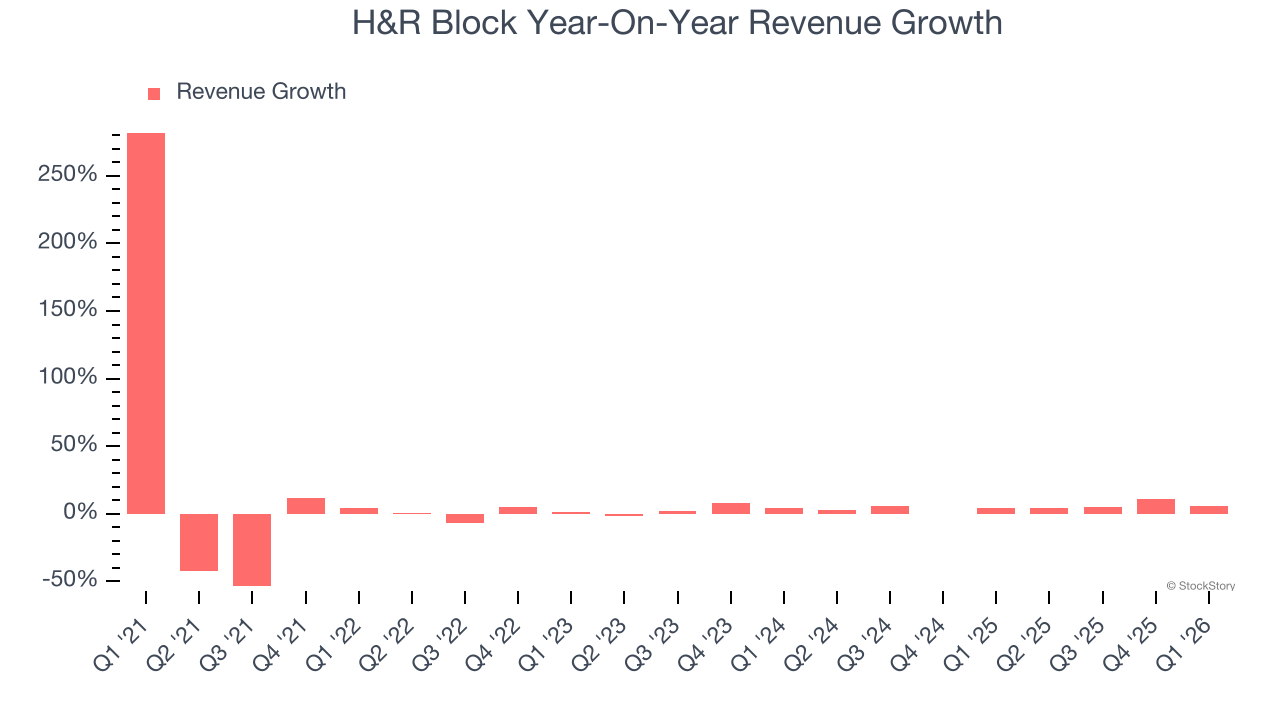

- Revenue: $2.40 billion vs analyst estimates of $2.34 billion (5.3% year-on-year growth, 2.5% beat)

- Adjusted EPS: $6.02 vs analyst estimates of $5.77 (4.3% beat)

- Adjusted EBITDA: $1.07 billion vs analyst estimates of $1.03 billion (44.7% margin, 3.7% beat)

- The company slightly lifted its revenue guidance for the full year to $3.92 billion at the midpoint from $3.89 billion

- Management raised its full-year Adjusted EPS guidance to $5.15 at the midpoint, a 4.6% increase

- Free Cash Flow Margin: 64.2%, up from 57.2% in the same quarter last year

- Market Capitalization: $3.81 billion

"This season marked an important inflection point, demonstrating that our strategy is driving higher-quality business outcomes," said Curtis Campbell, president and chief executive officer.

Company Overview

Founded in 1955 by brothers Henry W. Bloch and Richard A. Bloch, H&R Block (NYSE: HRB) is a tax preparation company offering professional tax assistance and financial solutions to individuals and small businesses.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, H&R Block’s demand was weak and its revenue declined by 2.1% per year. This was below our standards and is a sign of poor business quality. We note H&R Block is a seasonal business because it generates most of its revenue during tax season, so the charts in our report will look a bit lumpy.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. H&R Block’s annualized revenue growth of 4.5% over the last two years is above its five-year trend, which is encouraging.

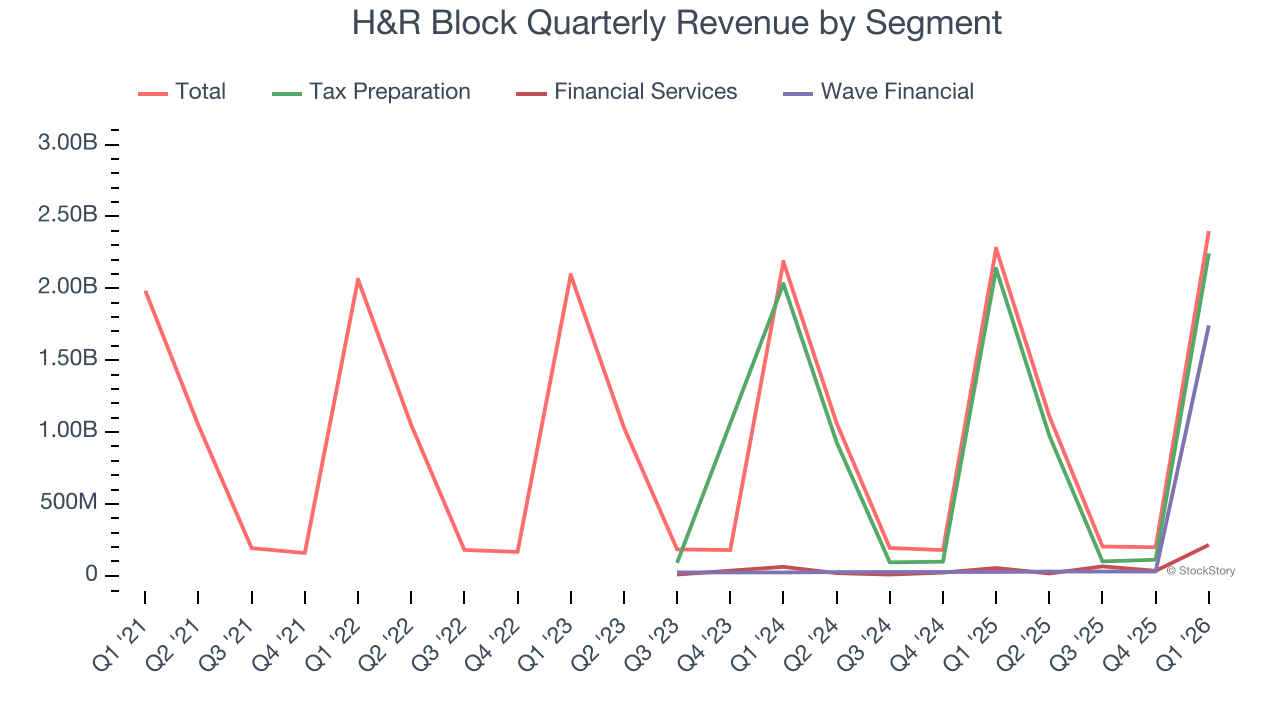

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Tax Preparation, Financial Services, and Wave Financial, which are 93.5%, 9%, and 72.6% of revenue. Over the last two years, H&R Block’s revenues in all three segments increased. Its Tax Preparation revenue (DIY, assisted, add-on services) averaged year-on-year growth of 6.6% while its Financial Services (Emerald Card, Spruce, interest income) and Wave Financial (business software) revenues averaged 161% and 1,081%.

This quarter, H&R Block reported year-on-year revenue growth of 5.3%, and its $2.40 billion of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 1.4% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

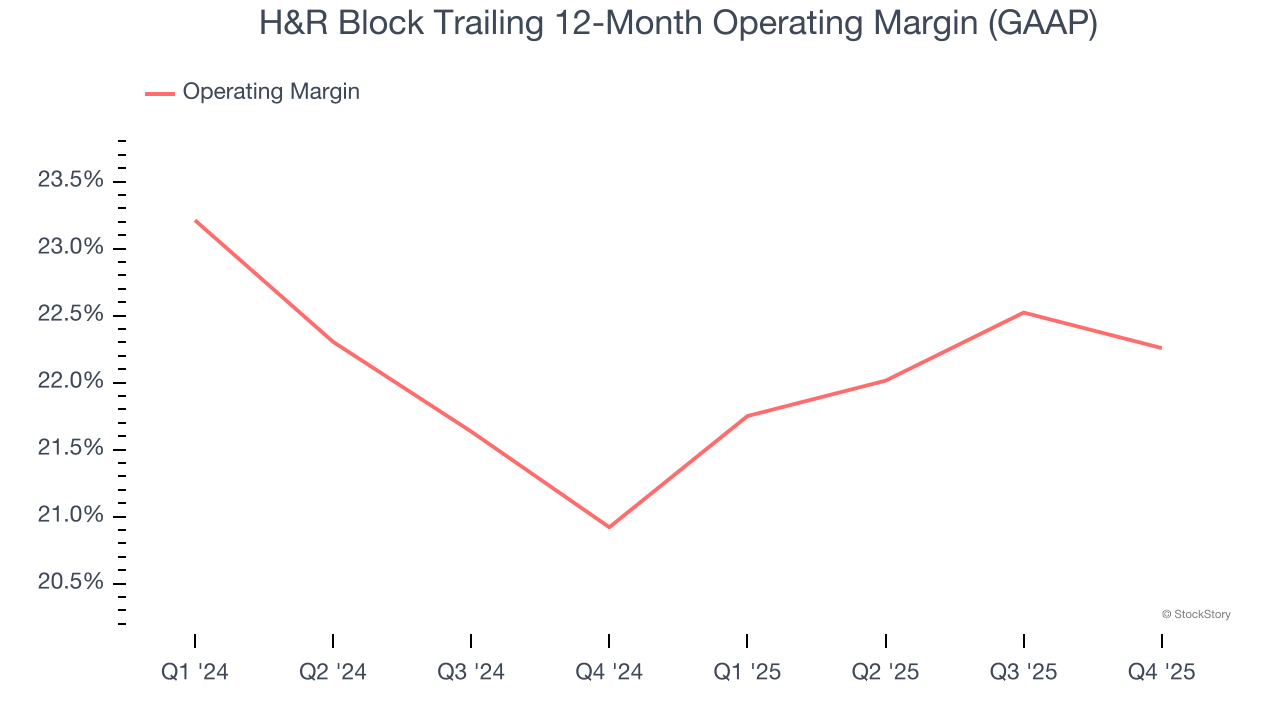

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

in line with the same quarter last year. Because H&R Block is a seasonal business, we prefer to analyze longer-term performance rather than one quarter.

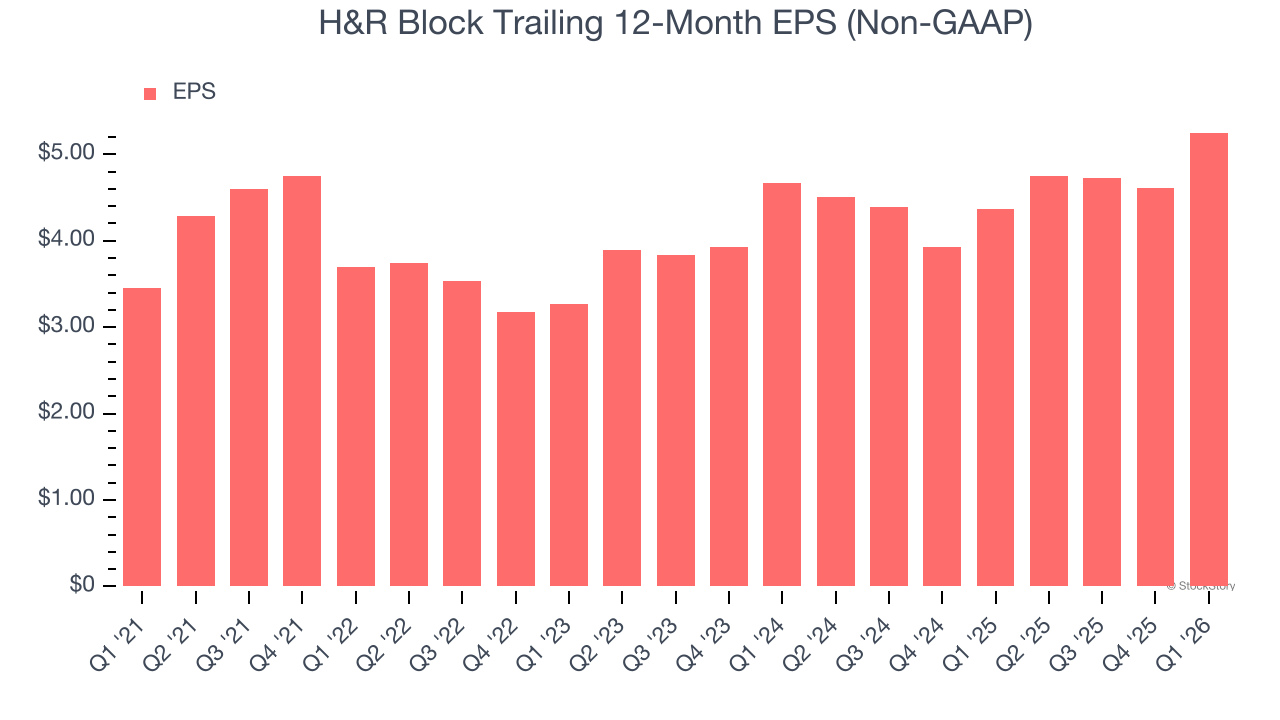

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

H&R Block’s EPS grew at 8.8% compounded annual growth rate over the last five years. This performance was better than its 2.1% annualized revenue declines but doesn’t tell us much about its business quality because its operating margin didn’t improve.

In Q1, H&R Block reported adjusted EPS of $6.02, up from $5.38 in the same quarter last year. This print beat analysts’ estimates by 4.3%. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from H&R Block’s Q1 Results

It was encouraging to see H&R Block beat analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 3% to $30.20 immediately following the results.

Sure, H&R Block had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).