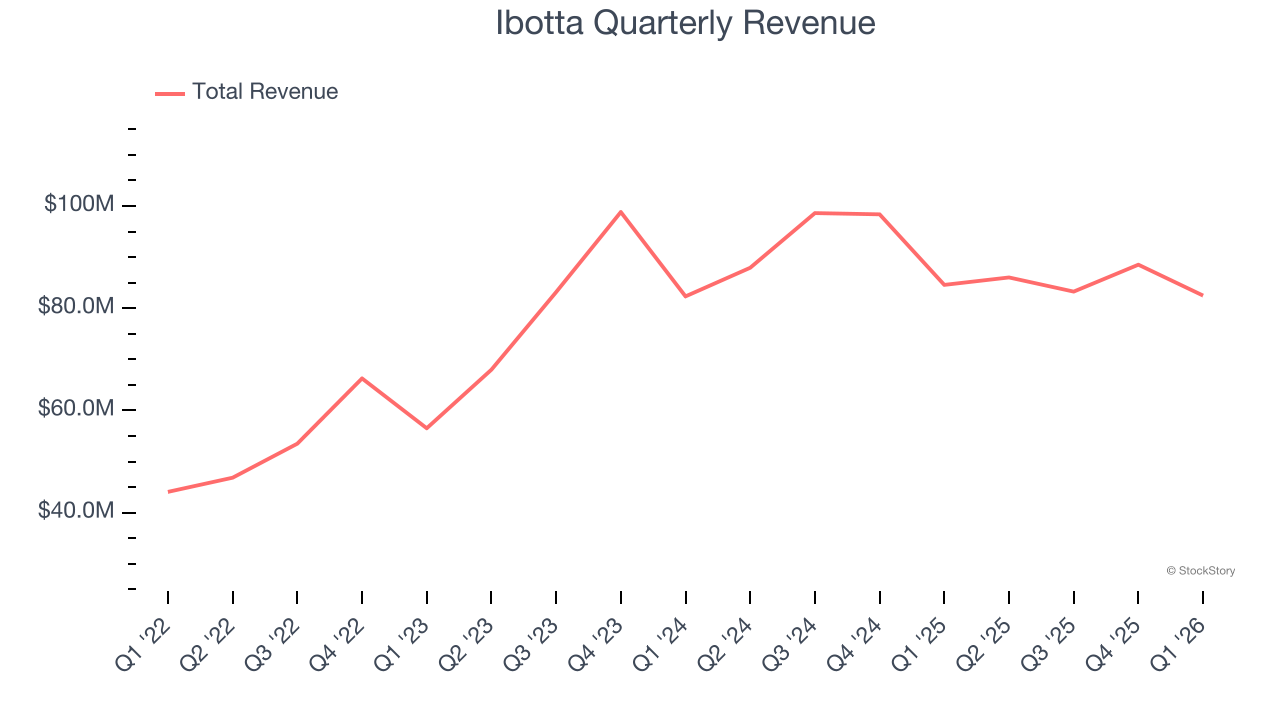

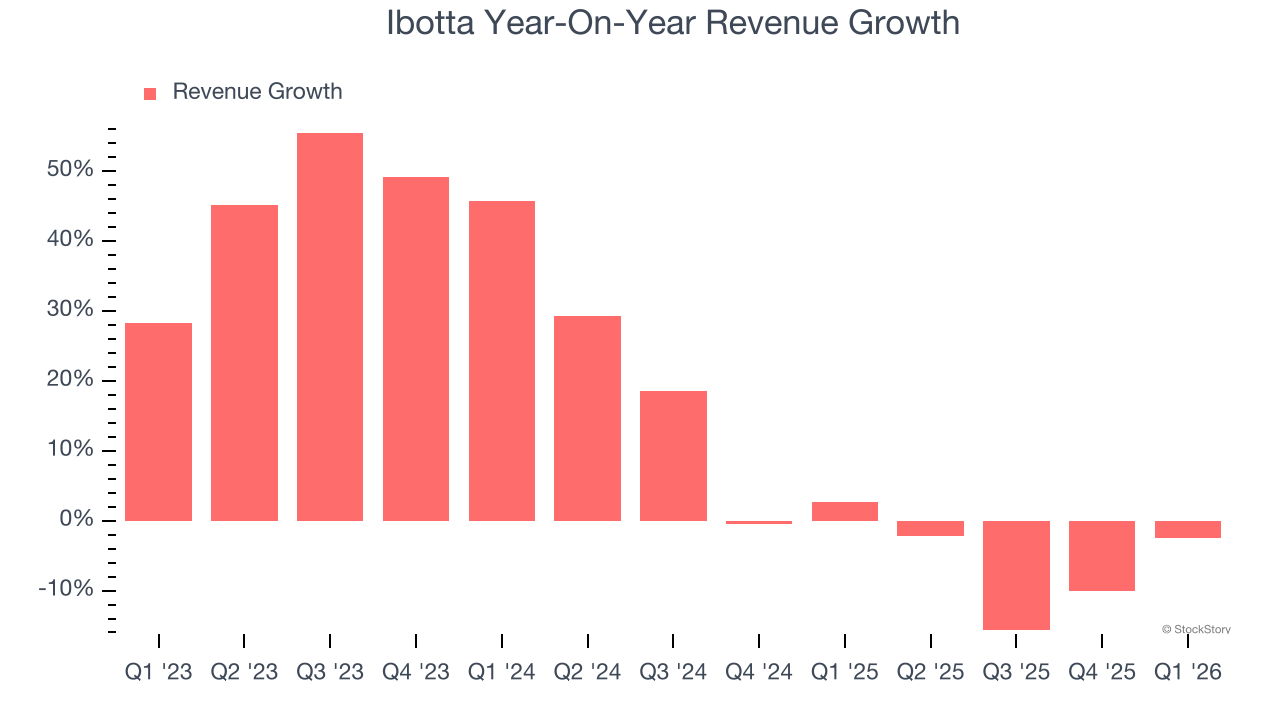

Cash-back rewards platform Ibotta (NYSE: IBTA) beat Wall Street’s revenue expectations in Q1 CY2026, but sales fell by 2.5% year on year to $82.48 million. Guidance for next quarter’s revenue was better than expected at $84 million at the midpoint, 0.8% above analysts’ estimates. Its non-GAAP profit of $0.24 per share was 6.6% below analysts’ consensus estimates.

Is now the time to buy Ibotta? Find out by accessing our full research report, it’s free.

Ibotta (IBTA) Q1 CY2026 Highlights:

- Revenue: $82.48 million vs analyst estimates of $80.95 million (2.5% year-on-year decline, 1.9% beat)

- Adjusted EPS: $0.24 vs analyst expectations of $0.26 (6.6% miss)

- Adjusted EBITDA: $8.72 million vs analyst estimates of $7.18 million (10.6% margin, 21.5% beat)

- Revenue Guidance for Q2 CY2026 is $84 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q2 CY2026 is $10.5 million at the midpoint, above analyst estimates of $9.88 million

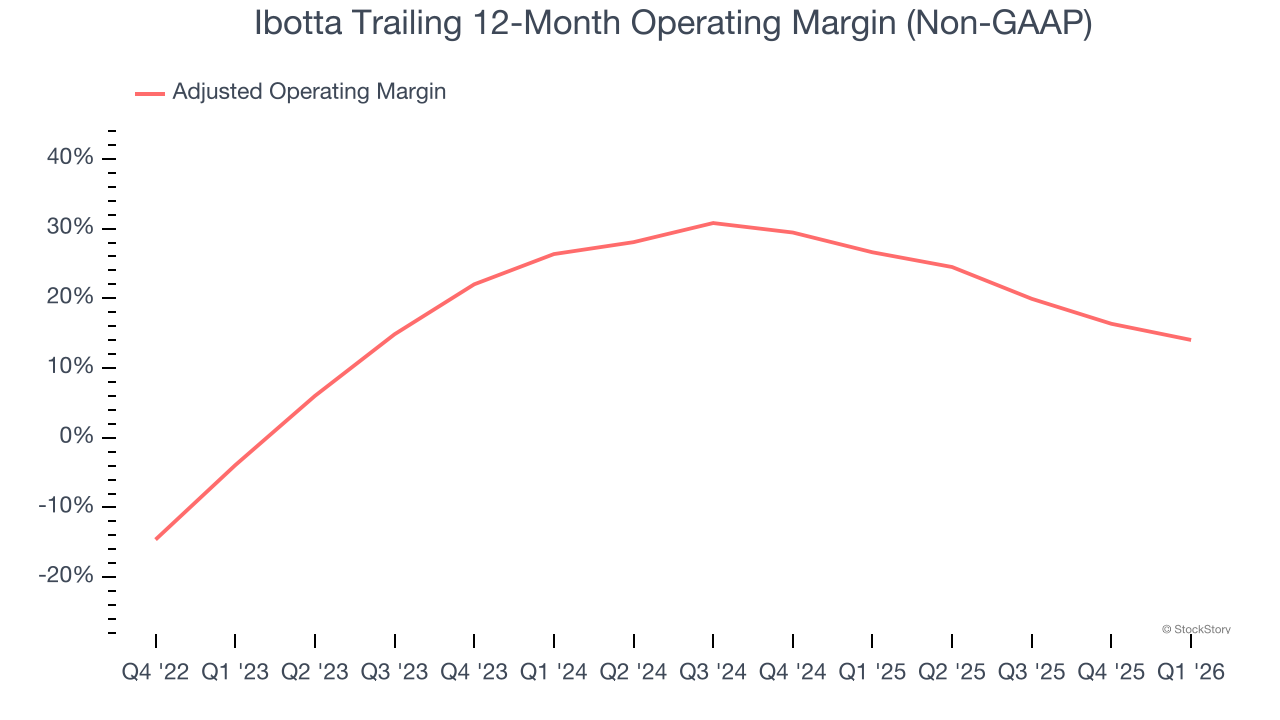

- Operating Margin: -13.1%, down from -3.3% in the same quarter last year

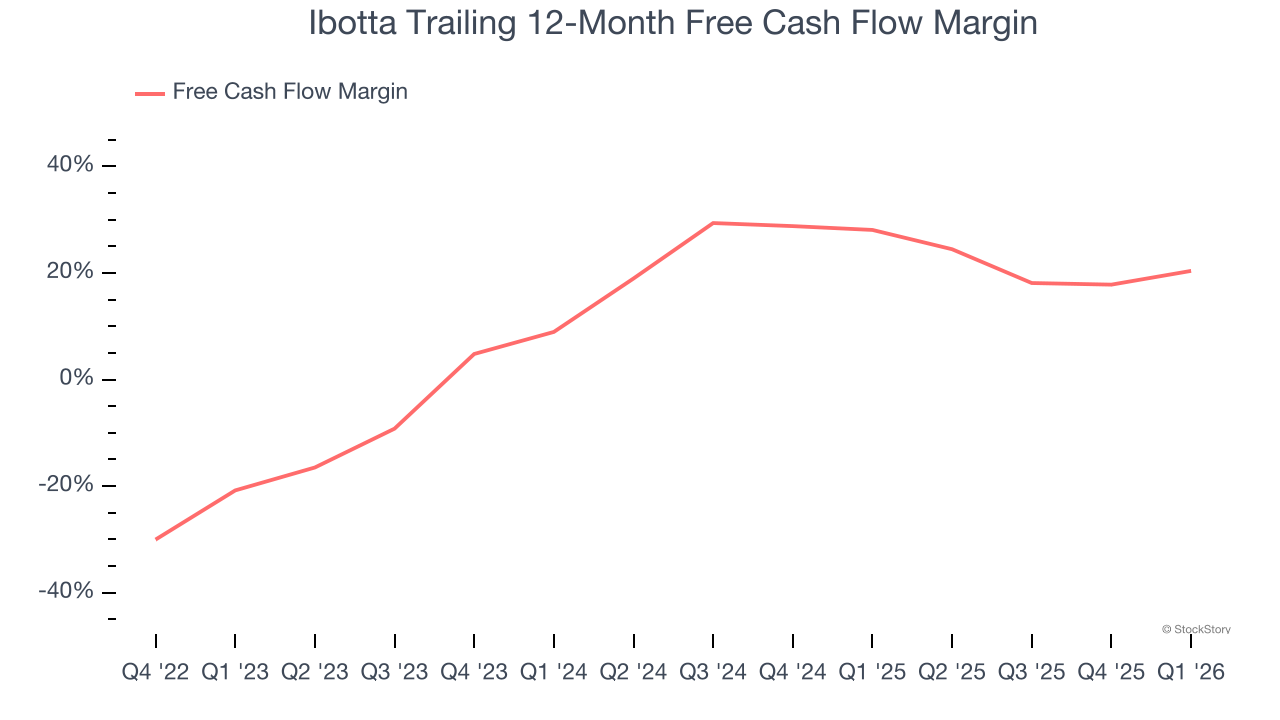

- Free Cash Flow Margin: 28.2%, up from 17.6% in the same quarter last year

- Total Redemptions: down 12.11 million year on year

- Market Capitalization: $878.7 million

Company Overview

Originally launched as a way to make grocery shopping more rewarding for budget-conscious consumers, Ibotta (NYSE: IBTA) is a mobile shopping app that allows consumers to earn cash back on everyday purchases by completing tasks and submitting receipts.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $340.3 million in revenue over the past 12 months, Ibotta is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Ibotta grew its sales at an incredible 19% compounded annual growth rate over the last three years. This is an encouraging starting point for our analysis because it shows Ibotta’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. Ibotta’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 1.2% over the last two years was well below its three-year trend.

This quarter, Ibotta’s revenue fell by 2.5% year on year to $82.48 million but beat Wall Street’s estimates by 1.9%. Company management is currently guiding for a 2.4% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months, similar to its two-year rate. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

Ibotta has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average adjusted operating margin of 15.6%.

Looking at the trend in its profitability, Ibotta’s adjusted operating margin rose by 18 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Ibotta generated an adjusted operating margin profit margin of 4.5%, down 9.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Ibotta has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.8% over the last five years, quite impressive for a business services business.

Taking a step back, we can see that Ibotta’s margin expanded by 41.2 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Ibotta’s free cash flow clocked in at $23.29 million in Q1, equivalent to a 28.2% margin. This result was good as its margin was 10.6 percentage points higher than in the same quarter last year, building on its favorable historical trend.

Key Takeaways from Ibotta’s Q1 Results

It was encouraging to see Ibotta beat analysts’ revenue expectations this quarter. We were also glad its revenue guidance for next quarter slightly exceeded Wall Street’s estimates. On the other hand, its EPS missed. Overall, this was a weaker quarter. The stock remained flat at $36.69 immediately after reporting.

Ibotta didn’t show it’s best hand this quarter, but does that create an opportunity to buy the stock right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).