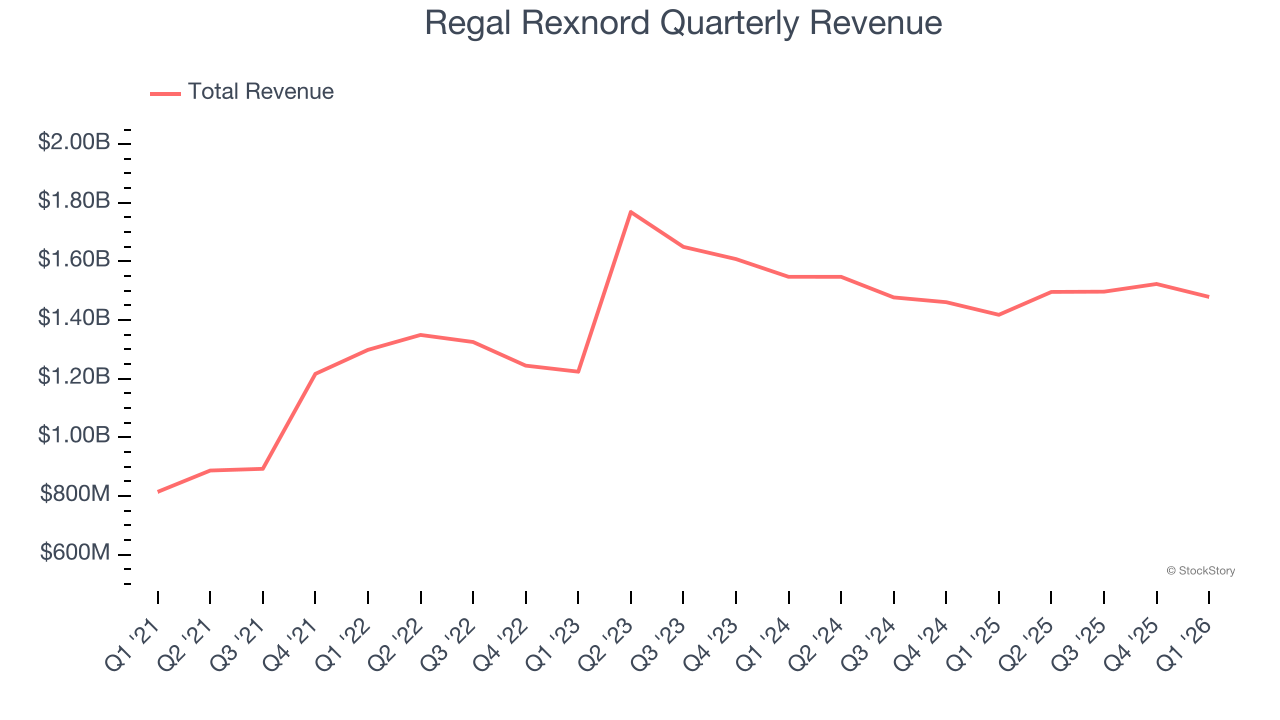

Industrials products and automation company Regal Rexnord (NYSE: RRX). reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 4.3% year on year to $1.48 billion. Its non-GAAP profit of $2.17 per share was 2.7% above analysts’ consensus estimates.

Is now the time to buy Regal Rexnord? Find out by accessing our full research report, it’s free.

Regal Rexnord (RRX) Q1 CY2026 Highlights:

- Revenue: $1.48 billion vs analyst estimates of $1.44 billion (4.3% year-on-year growth, 3% beat)

- Adjusted EPS: $2.17 vs analyst estimates of $2.11 (2.7% beat)

- Adjusted EBITDA: $304.4 million vs analyst estimates of $301 million (20.6% margin, 1.1% beat)

- Management reiterated its full-year Adjusted EPS guidance of $10.60 at the midpoint

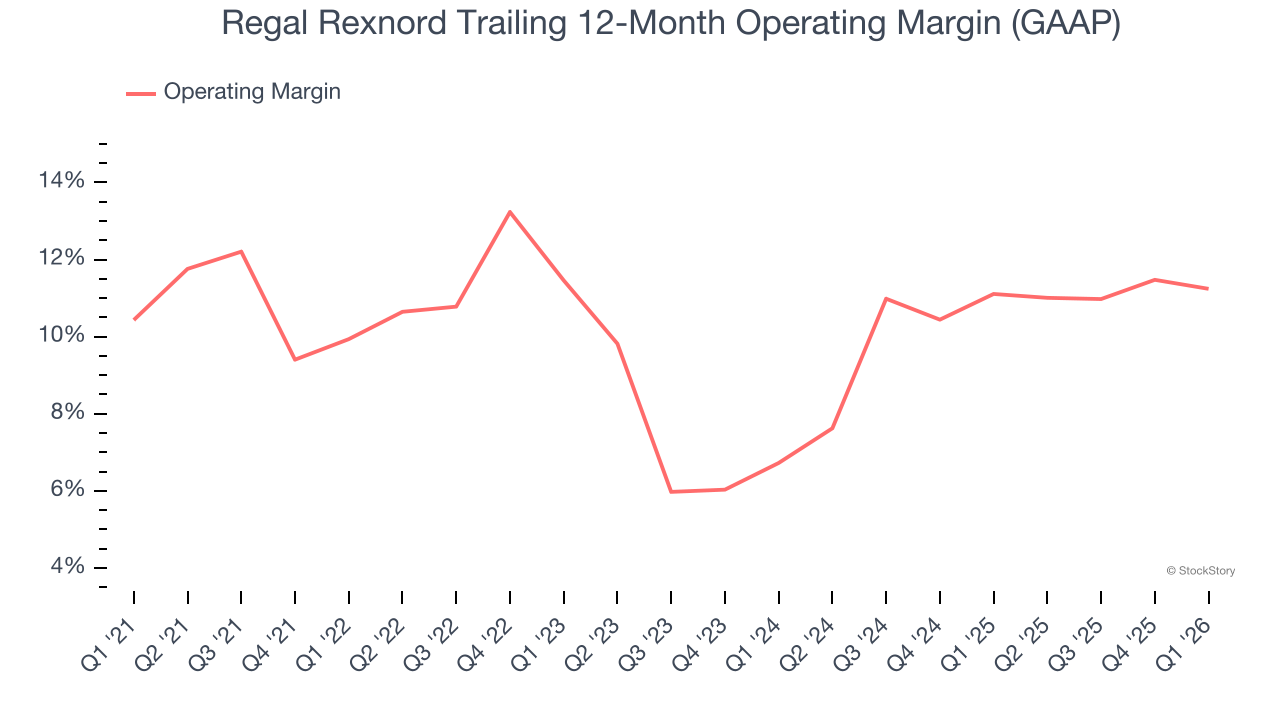

- Operating Margin: 10.3%, in line with the same quarter last year

- Free Cash Flow was -$2.5 million, down from $85.5 million in the same quarter last year

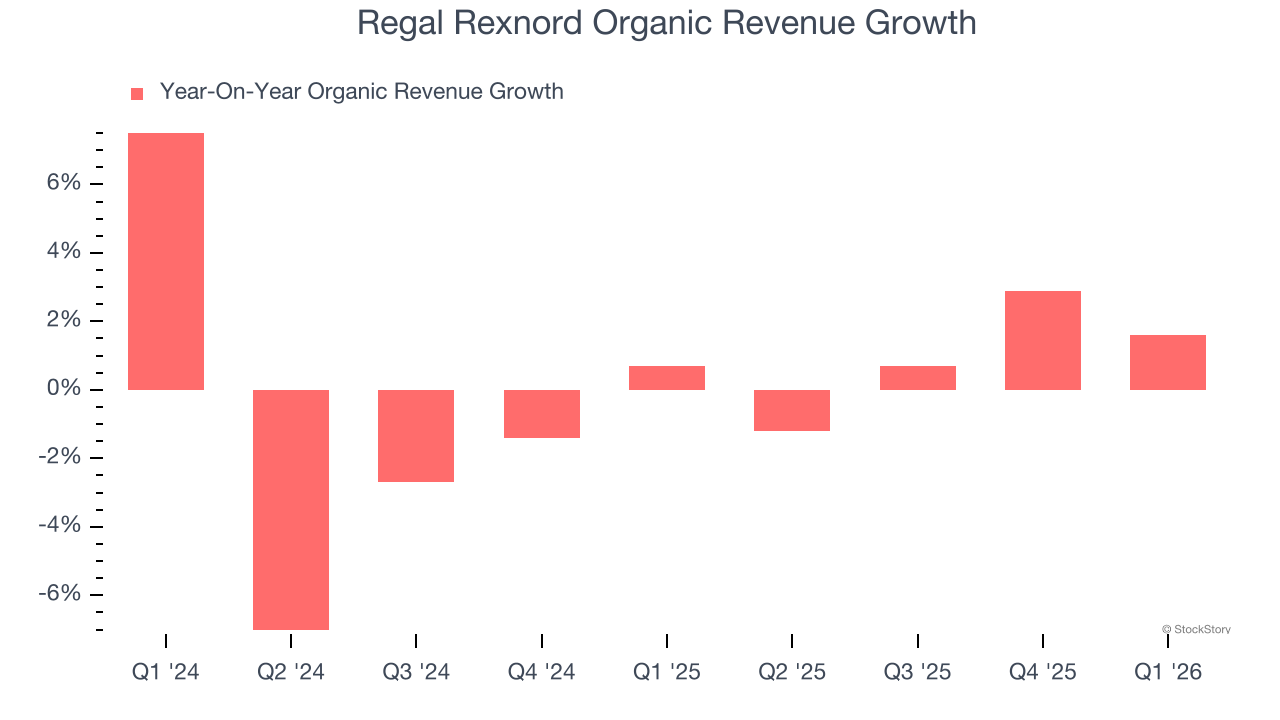

- Organic Revenue rose 1.6% year on year (beat)

- Market Capitalization: $14.78 billion

CEO Louis Pinkham commented, "Our growth outlook continued to strengthen during the first quarter, with enterprise daily orders up 8.5% versus the prior year. Our AMC segment led the way, with orders up over 34%, aided by growth across all markets, but particularly in aerospace & defense, discrete automation, data center and medical. Our IPS business also saw order acceleration in its distribution business and high single digit growth in its short cycle OEM business, consistent with improving industrial macro metrics, such as the ISM. PES orders were down as expected, but less severely, as residential HVAC markets show tentative signs of normalizing. We also saw continued strength in commercial HVAC, primarily driven by data center demand. While some of the enterprise order strength is tied to improving industrial and automation markets, our growth investments are also paying off, and our cross-sell initiatives continue to contribute nicely."

Company Overview

Headquartered in Milwaukee, Regal Rexnord (NYSE: RRX) provides power transmission and industrial automation products.

Revenue Growth

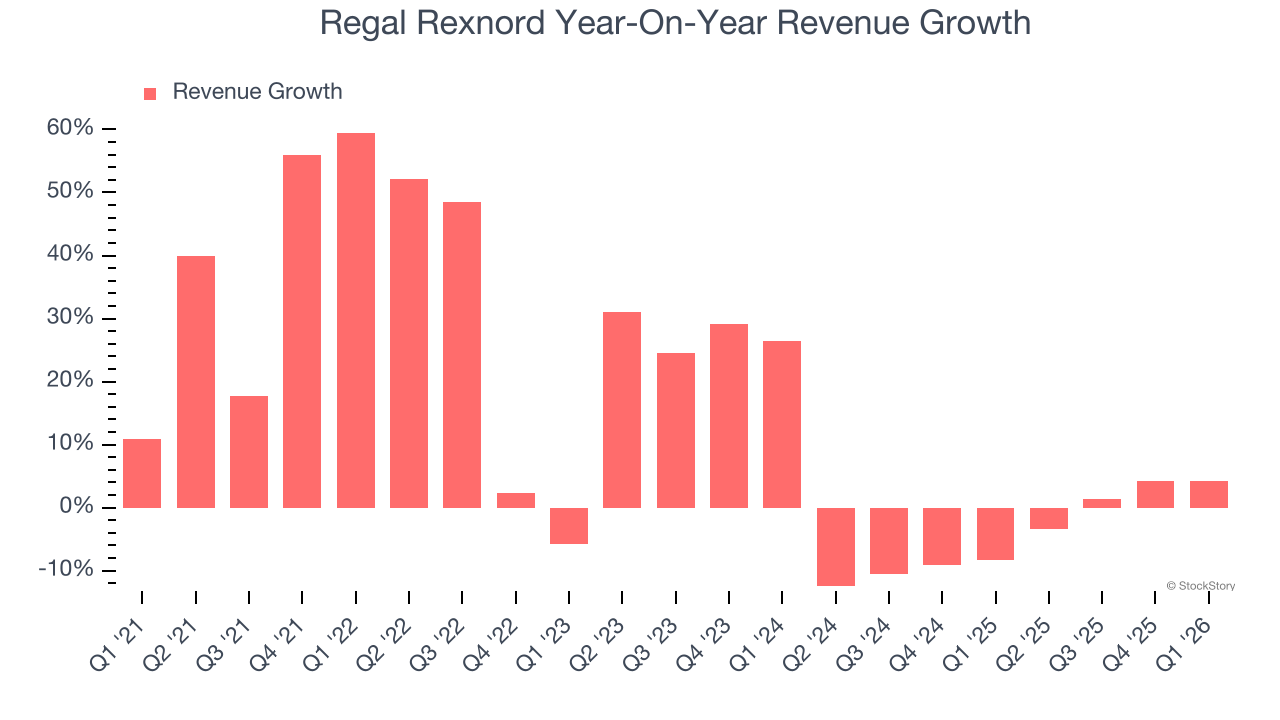

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Regal Rexnord’s 15% annualized revenue growth over the last five years was exceptional. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Regal Rexnord’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 4.5% over the last two years.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Regal Rexnord’s organic revenue was flat. Because this number is better than its two-year revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Regal Rexnord reported modest year-on-year revenue growth of 4.3% but beat Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 5.4% over the next 12 months. Although this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Regal Rexnord has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Regal Rexnord’s operating margin rose by 1.3 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Regal Rexnord generated an operating margin profit margin of 10.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

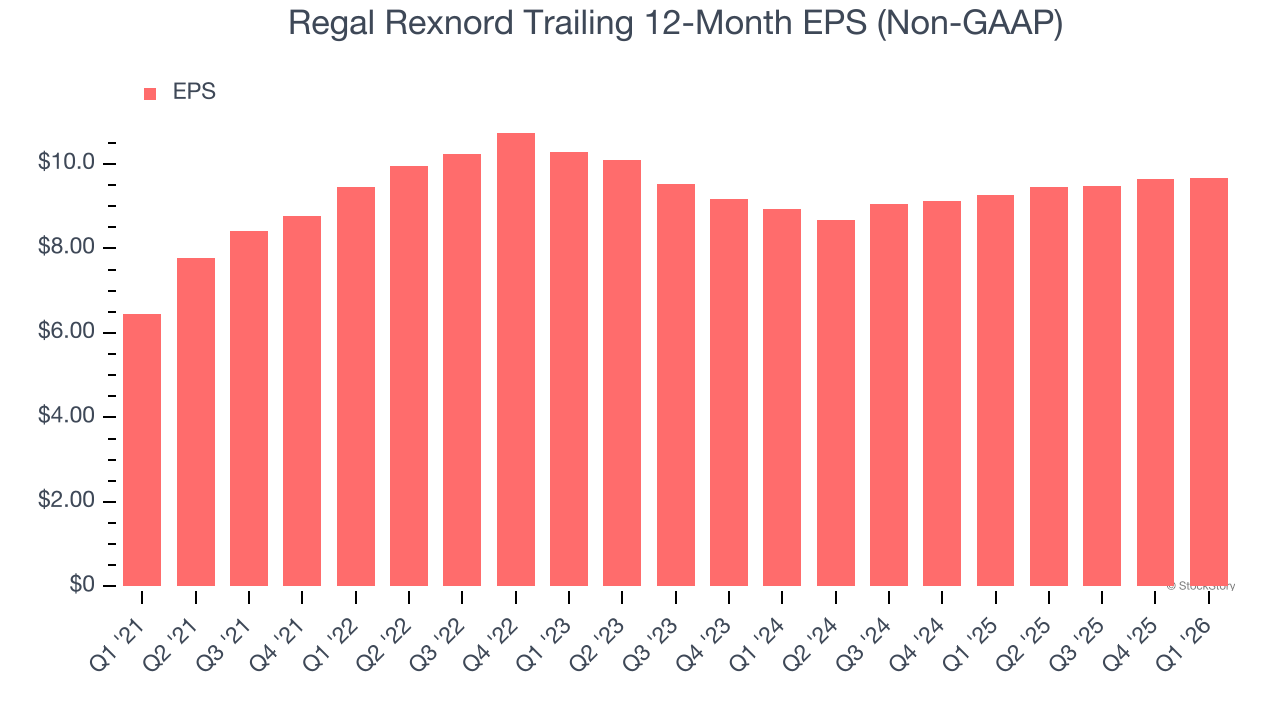

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Regal Rexnord’s EPS grew at a decent 8.5% compounded annual growth rate over the last five years. Despite its operating margin improvement during that time, this performance was lower than its 15% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

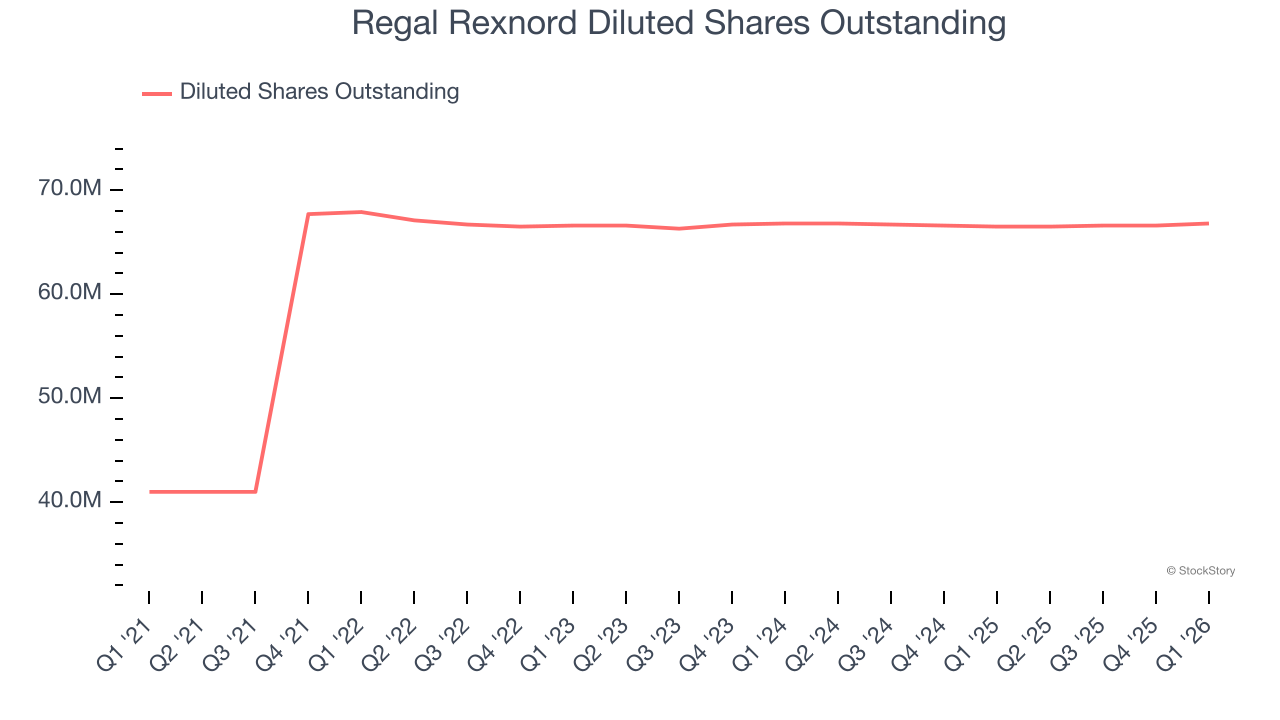

Diving into the nuances of Regal Rexnord’s earnings can give us a better understanding of its performance. A five-year view shows Regal Rexnord has diluted its shareholders, growing its share count by 62.9%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Regal Rexnord, its two-year annual EPS growth of 4% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q1, Regal Rexnord reported adjusted EPS of $2.17, up from $2.15 in the same quarter last year. This print beat analysts’ estimates by 2.7%. Over the next 12 months, Wall Street expects Regal Rexnord’s full-year EPS of $9.67 to grow 16.2%.

Key Takeaways from Regal Rexnord’s Q1 Results

We enjoyed seeing Regal Rexnord beat analysts’ revenue expectations this quarter. We were also glad its organic revenue outperformed Wall Street’s estimates. On the other hand, its adjusted operating income missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed. The market seemed to be hoping for more, and the stock traded down 3.5% to $217.58 immediately after reporting.

Big picture, is Regal Rexnord a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).