Icahn Enterprises currently trades at $7.45 per share and has shown little upside over the past six months, posting a small loss of 3.6%. The stock also fell short of the S&P 500’s 10.7% gain during that period.

Is now the time to buy Icahn Enterprises, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Icahn Enterprises Will Underperform?

We don’t have much confidence in Icahn Enterprises. Here are three reasons you should be careful with IEP, plus one stock we’d rather own.

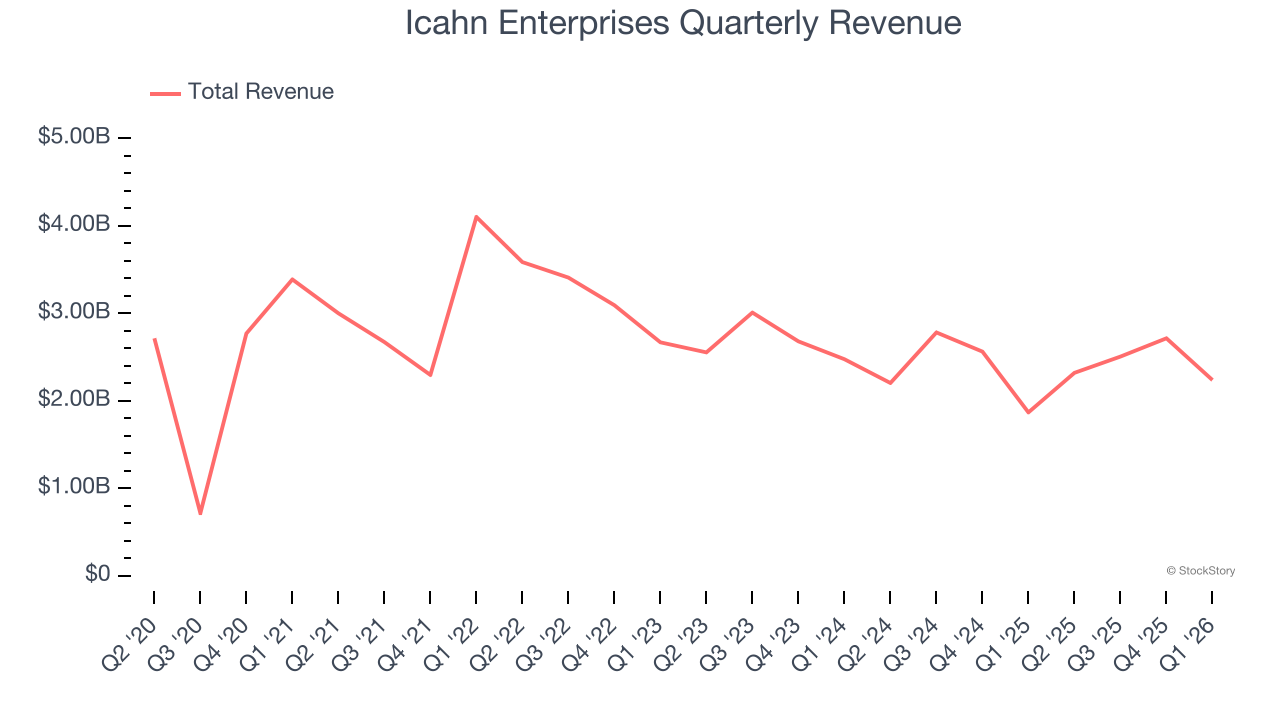

1. Long-Term Revenue Growth Flatter Than a Pancake

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Icahn Enterprises struggled to consistently increase demand as its $9.78 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and is a sign of poor business quality.

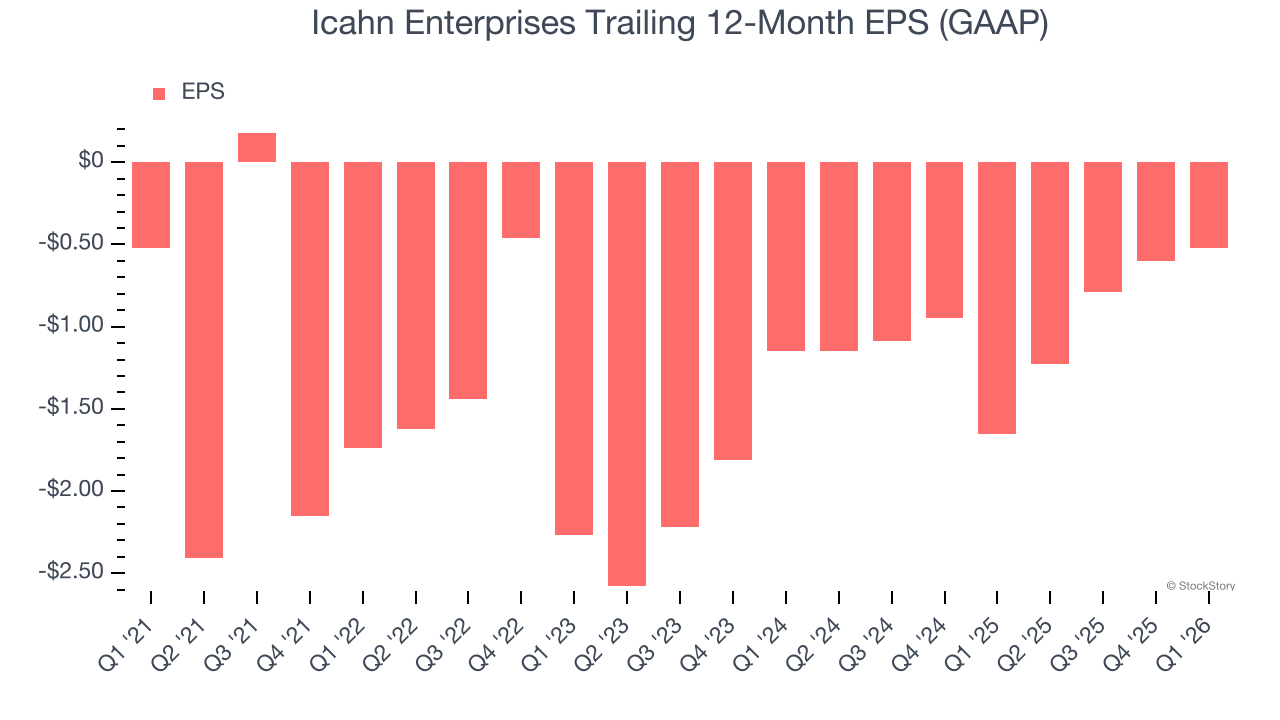

2. EPS Barely Budging

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Icahn Enterprises’s full-year EPS was flat over the last five years. This performance was underwhelming across the board.

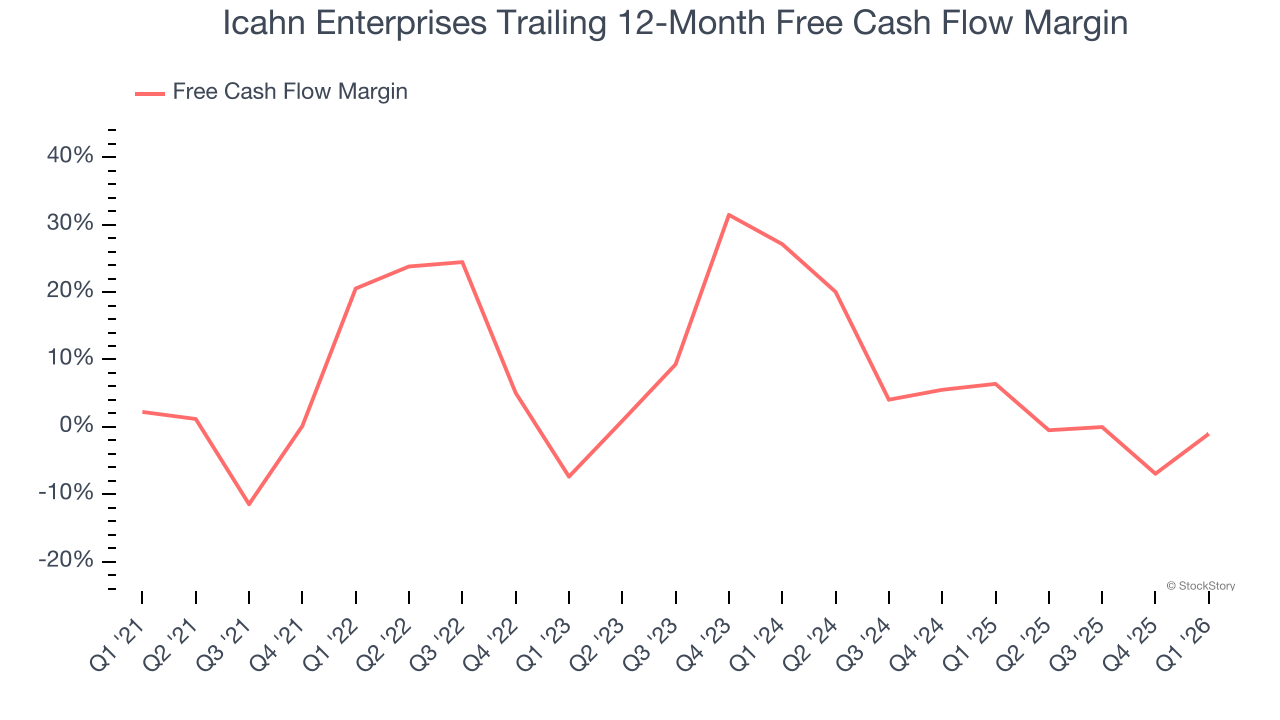

3. Free Cash Flow Margin Dropping

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Icahn Enterprises’s margin dropped by 21.6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Icahn Enterprises’s free cash flow margin for the trailing 12 months was negative 1%.

Final Judgment

We see the value of companies helping their customers, but in the case of Icahn Enterprises, we’re out. With its shares lagging the market recently, the stock trades at $7.45 per share (or a trailing 12-month price-to-sales ratio of 0.5×). The market typically values companies like Icahn Enterprises based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.