While artificial intelligence (AI) is one of the biggest disruptive technologies of this generation, it also poses a challenge to some established companies, including cybersecurity firms and software companies.

In short, AI-powered programs are developing quickly enough that they can perhaps duplicate the actions of some software, including tools that automate workflows or provide analytics. For cybersecurity firms, it’s more of a double-edged sword. AI can help cybersecurity companies expand their reach by monitoring more endpoints, but it can also eat into the bottom line. Companies can use AI to embed security directly into their platforms, reducing the need for cybersecurity companies like Palo Alto Networks (PANW).

That’s one of the reasons why PANW stock is down 19% in the last month alone. But CEO Nikesh Arora is trying to stop the bleeding, telling analysts during the company’s most recent earnings call that AI isn’t a viable replacement for cybersecurity.

“I’m still confused why the market is treating AI as a threat to at least cybersecurity,” Arora said. “I can’t speak for all of software, but one thing we’re definitely seeing is that customers have figured out that they need to drive more consistency in their security stack to be able to respond faster using AI.”

Should investors be backing away from Palo Alto Networks now? Or is the recent weakness in PANW stock and cybersecurity stocks a golden opportunity to buy the dip?

About Palo Alto Networks Stock

Headquartered in Santa Clara, California, Palo Alto Networks provides network security products to clients and government agencies around the world. The company provides an AI-powered network security platform and offers next-generation firewalls, as well as products that support Virtual Private Network (VPN) technologies, and intrusion detection and prevention.

Shares of PANW are down 25% in the last 12 months as part of a sector-wide slump that is also affecting companies like Zscaler (ZS) and Fortinet (FTNT). Palo Alto is badly underperforming the S&P 500 ($SPX), which is up 13% in the last year.

However, the drop is also making the stock more affordable right now. PANW stock currently has a forward price-to-sales (P/S) ratio of 13.3 times, which is just above its five-year P/S mean of 12.1. The forward price-to-earnings (P/E) ratio of 72 times is also more reasonable compared to Palo Alto's historical average.

Palo Alto Stock Beats on Earnings

Investors may not realize that PANW stock is struggling just by looking at the earnings report, as the company had strong results for the fiscal second quarter of 2026 (the period ending Jan. 31). Revenue was $2.6 billion, up 15% year-over-year (YOY). The company also saw a 22% improvement in its product revenue to $514 million, and 13% revenue growth for its subscription and support services.

Net income was $432 million, up 61% YOY. EPS came in at $0.61, beating analysts’ expectations of $0.49.

"We saw continued strength in platformizations, a trend that is accelerating due to AI — customers are keen to both modernize and normalize their cybersecurity stack, aligning them to our approach,” said Arora.

Palo Alto is also expanding, having announced a $3.35 billion acquisition of Chronosphere, which operates an AI platform, and having finalized its $25 billion purchase of the cybersecurity company CyberArk. The company plans to incorporate CyberArk’s identity security platform into its security suite.

Management issued guidance for the third quarter to include revenue of $2.941 billion to $2.945 billion, up about 28% from a year ago, and net income per share in a range of $0.78 and $0.80.

What Do Analysts Expect for PANW Stock?

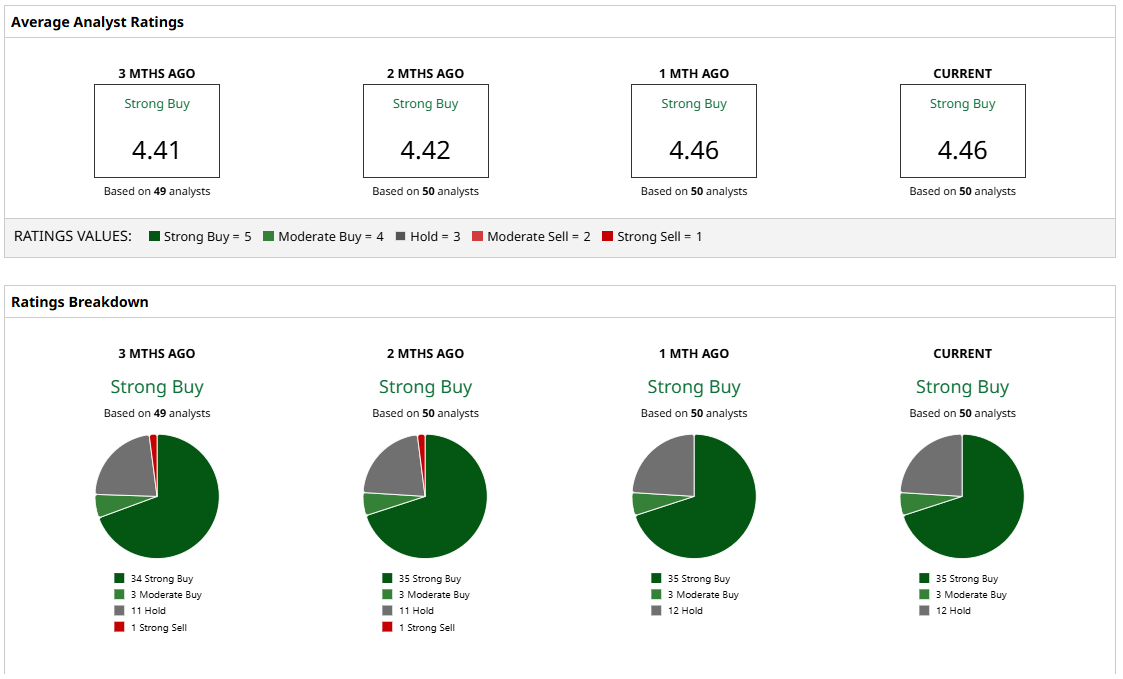

In general, analysts have long been bullish on the cybersecurity company. Of the 50 analysts with coverage of PANW stock, 35 give it a “Strong Buy” rating, three have a ”Moderate Buy," and 12 suggest a “Hold” rating. Analysts have a mean price target of $209.40, which implies 41% potential upside for the stock.

That may be changing, however. For instance, BMO Capital analyst Keith Bachman recently maintained an “Outperform” rating on PANW stock but lowered his price target from $230 to $200. Bachman expects the company to deliver YOY organic growth in the double-digits for the foreseeable future, but lowered his target in light of “uncertainty surrounding the broader software segment.”

With that in mind, it makes sense for Palo Alto's CEO to try to shore up the stock price with a bullish outlook. The company’s earnings report and outlook back up the rosy sentiment. However, considering the short-term weakness in software stocks right now, I would only consider PANW stock as an investment if I planned to buy and hold for several years. In the short term, I’m expecting continued volatility and weakness.

On the date of publication, Patrick Sanders did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart