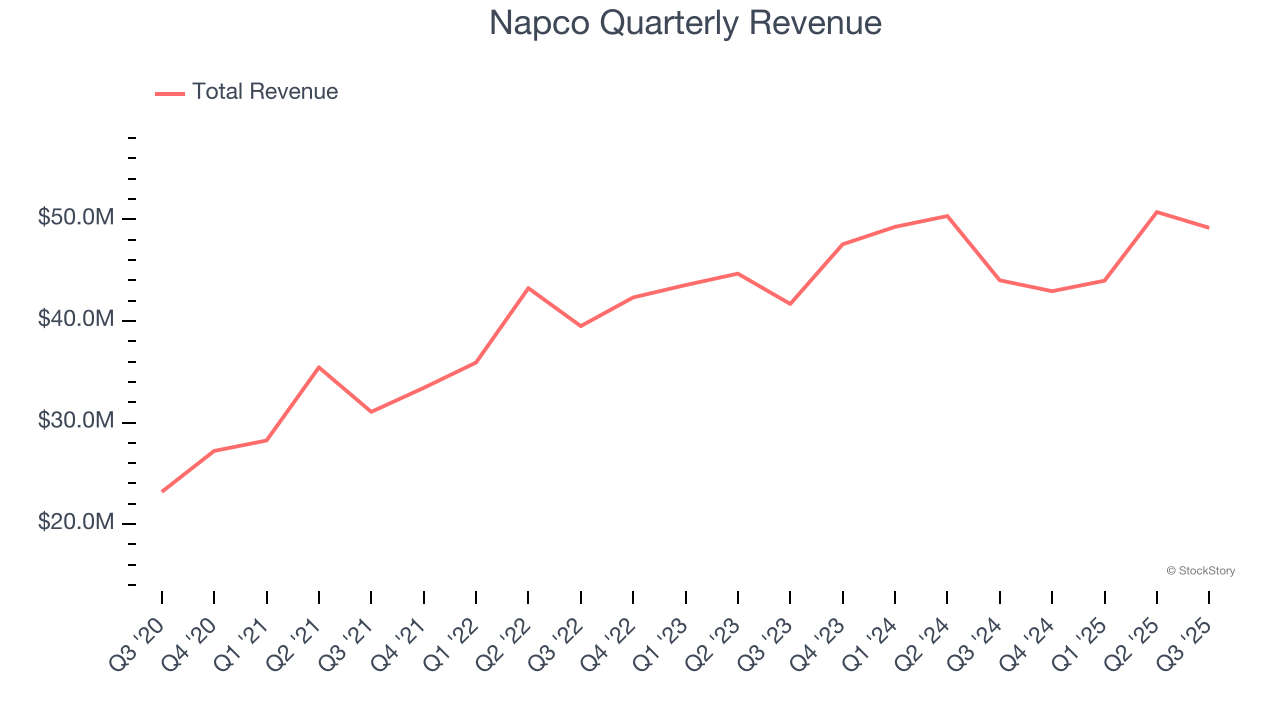

Security systems manufacturer Napco (NASDAQ: NSSC) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 11.7% year on year to $49.17 million. Its GAAP profit of $0.34 per share was 11.1% above analysts’ consensus estimates.

Is now the time to buy Napco? Find out by accessing our full research report, it’s free for active Edge members.

Napco (NSSC) Q3 CY2025 Highlights:

- Revenue: $49.17 million vs analyst estimates of $46.91 million (11.7% year-on-year growth, 4.8% beat)

- EPS (GAAP): $0.34 vs analyst estimates of $0.31 (11.1% beat)

- Adjusted EBITDA: $14.94 million vs analyst estimates of $13.46 million (30.4% margin, 11% beat)

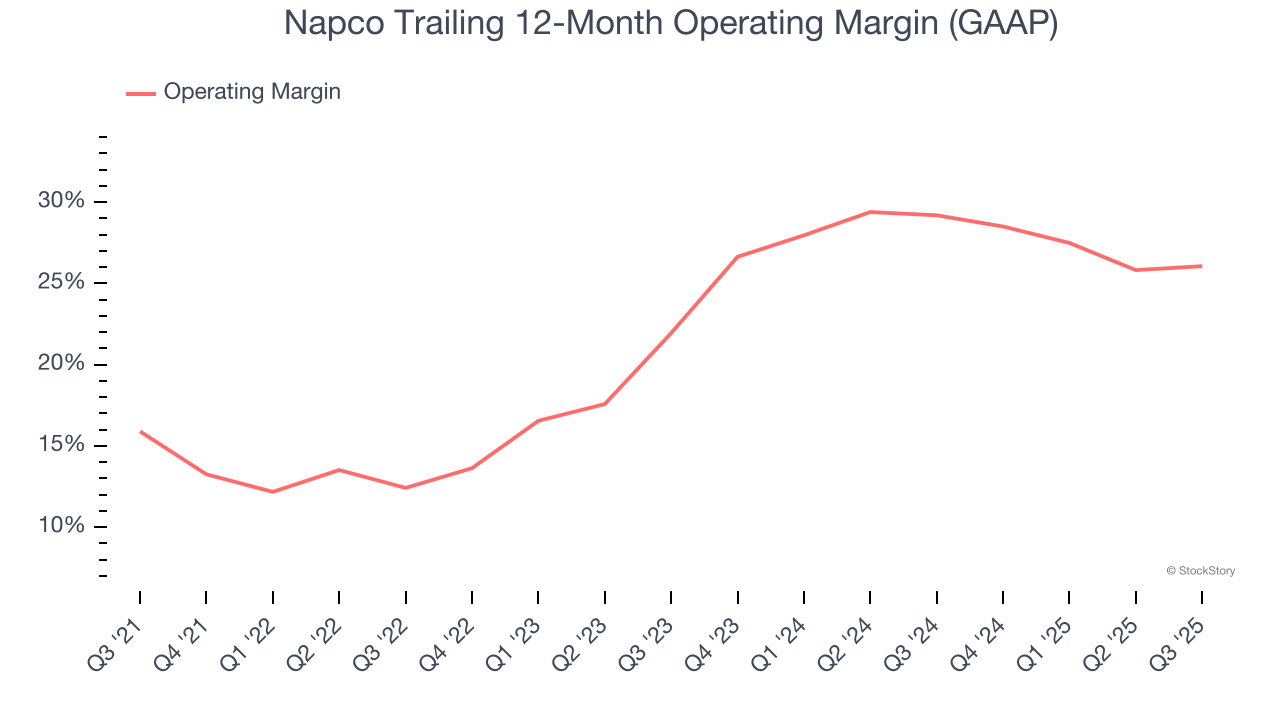

- Operating Margin: 27.7%, in line with the same quarter last year

- Free Cash Flow Margin: 23.3%, down from 25.8% in the same quarter last year

- Market Capitalization: $1.57 billion

Richard Soloway, Chairman and CEO, commented, "With the completion of the first quarter of Fiscal 2026, we experienced year over year double digit growth in both our equipment and service revenue. Strong demand for our door-locking products has driven the growth in our equipment revenue and improved equipment gross margins, and our RSR continues to see growth quarter over quarter with sustained gross margins of over 90%. RSR represents 48% of total revenue in Q1, and our RSR has a prospective run rate of approximately $95 million based on our October 2025 recurring service revenue. As a result of our revenue growth, net income increased 8.8% year over year to a Q1 record of $12.2 million and our adjusted EBITDA margin was 30.4% as compared to 28.0% in Q1 of Fiscal 2025.

Company Overview

Protecting everything from schools to government facilities since 1969, Napco Security Technologies (NASDAQ: NSSC) manufactures electronic security devices, access control systems, and communication services for intrusion and fire alarm systems.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $186.8 million in revenue over the past 12 months, Napco is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Napco grew its sales at an exceptional 13.7% compounded annual growth rate over the last five years. This is an encouraging starting point for our analysis because it shows Napco’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Napco’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.2% over the last two years was well below its five-year trend.

This quarter, Napco reported year-on-year revenue growth of 11.7%, and its $49.17 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 8.6% over the next 12 months, an improvement versus the last two years. This projection is healthy and indicates its newer products and services will catalyze better top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Napco has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 21.9%.

Looking at the trend in its profitability, Napco’s operating margin rose by 10.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Napco generated an operating margin profit margin of 27.7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

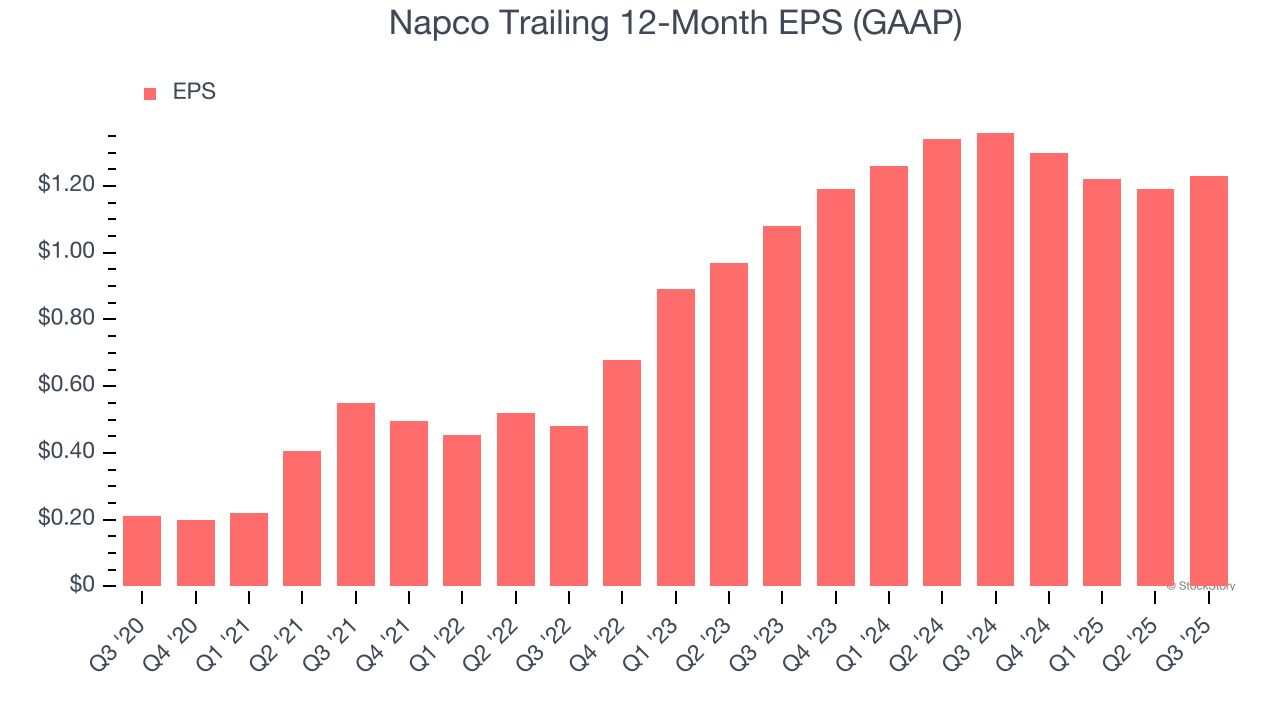

Napco’s EPS grew at an astounding 42.4% compounded annual growth rate over the last five years, higher than its 13.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

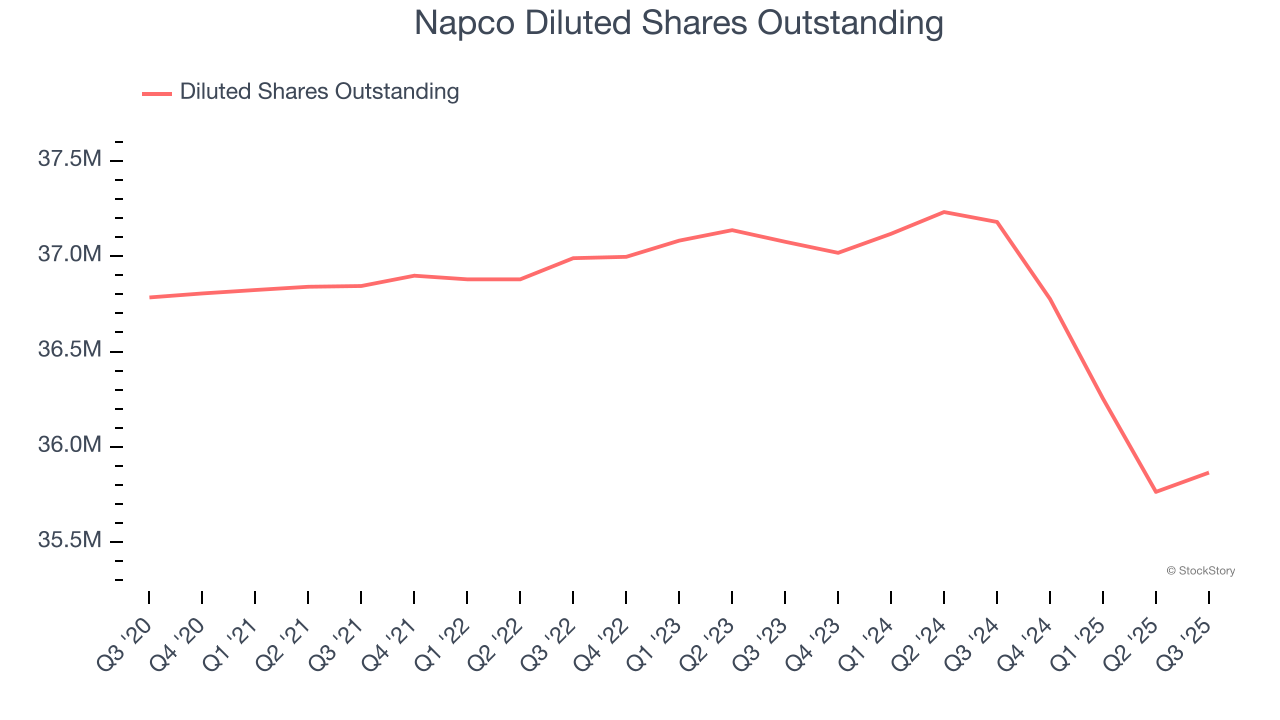

We can take a deeper look into Napco’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Napco’s operating margin was flat this quarter but expanded by 10.2 percentage points over the last five years. On top of that, its share count shrank by 2.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Napco, its two-year annual EPS growth of 6.7% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q3, Napco reported EPS of $0.34, up from $0.30 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Napco’s full-year EPS of $1.23 to grow 10.2%.

Key Takeaways from Napco’s Q3 Results

We enjoyed seeing Napco beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.9% to $45.36 immediately following the results.

Napco had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.