Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Powell (NASDAQ: POWL) and the best and worst performers in the electrical systems industry.

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

The 13 electrical systems stocks we track reported a slower Q4. As a group, revenues beat analysts’ consensus estimates by 0.6% while next quarter’s revenue guidance was 6.1% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 18.3% since the latest earnings results.

Powell (NASDAQ: POWL)

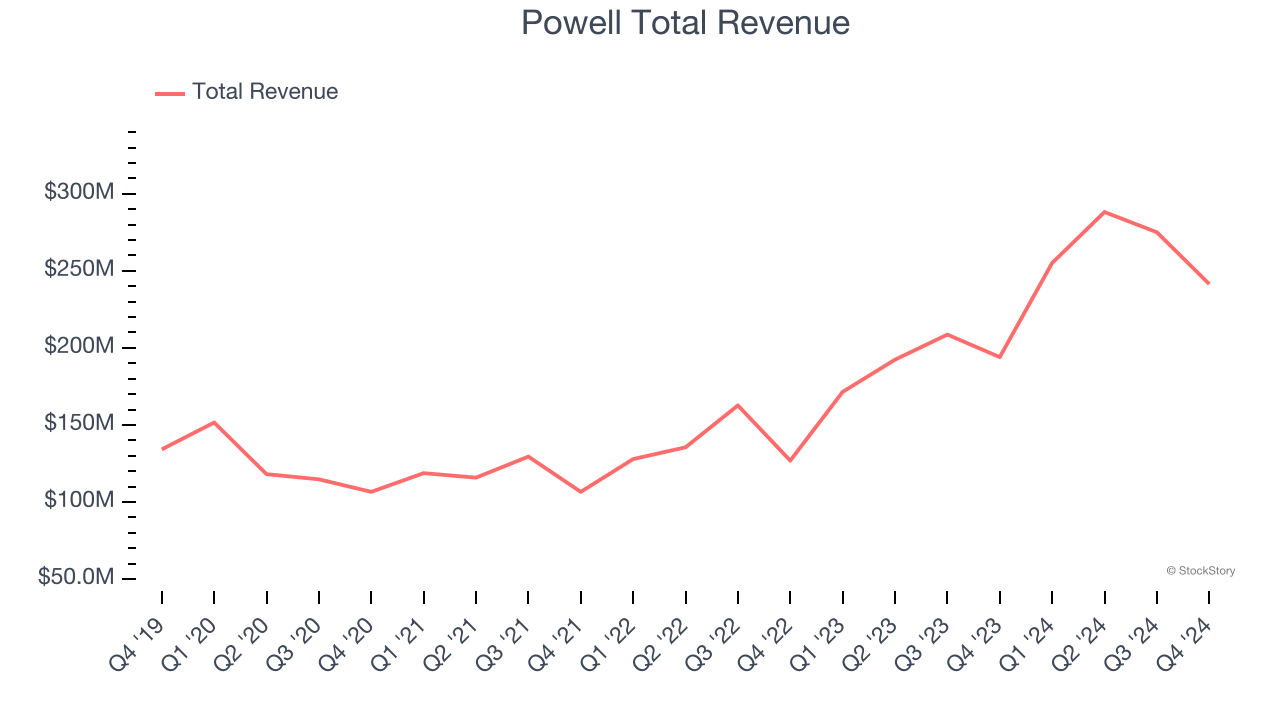

Originally a metal-working shop supporting local petrochemical facilities, Powell (NYSE: POWL) has grown from a small Houston manufacturer to a global provider of electrical systems.

Powell reported revenues of $241.4 million, up 24.4% year on year. This print exceeded analysts’ expectations by 3.8%. Overall, it was a satisfactory quarter for the company with a decent beat of analysts’ EPS estimates but a significant miss of analysts’ EBITDA estimates.

Brett A. Cope, Powell’s Chairman and Chief Executive Officer, stated, “Powell recorded a strong start to Fiscal 2025 highlighted by new order growth of 36%. We saw strong order activity across each of our market sectors, as our Electric Utility and Oil & Gas markets continue to benefit from robust tailwinds that support our expectation for volume growth in 2025. We were awarded a large LNG project situated along the U.S. Gulf Coast during the quarter as we expect this market sector to see improved activity levels relative to Fiscal 2024. Revenue also grew 24% and we delivered earnings per diluted share of $2.86 despite what is typically a seasonally softer first quarter. Overall, we remain very encouraged by both our backlog as well as the volume and composition of projects in our pipeline.”

The stock is down 31.3% since reporting and currently trades at $168.06.

Is now the time to buy Powell? Access our full analysis of the earnings results here, it’s free.

Best Q4: LSI (NASDAQ: LYTS)

Enhancing commercial environments, LSI (NASDAQ: LYTS) provides lighting and display solutions for businesses and retailers.

LSI reported revenues of $147.7 million, up 35.5% year on year, outperforming analysts’ expectations by 14.3%. The business had an incredible quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

LSI pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared to its peers, the market seems unhappy with the results as the stock is down 13.9% since reporting. It currently trades at $17.04.

Is now the time to buy LSI? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Methode Electronics (NYSE: MEI)

Founded in 1946, Methode Electronics (NYSE: MEI) is a global supplier of custom-engineered solutions for Original Equipment Manufacturers (OEMs).

Methode Electronics reported revenues of $239.9 million, down 7.6% year on year, falling short of analysts’ expectations by 8.9%. It was a disappointing quarter as it posted revenue guidance for next quarter missing analysts’ expectations significantly and a significant miss of analysts’ EBITDA estimates.

Methode Electronics delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 37.5% since the results and currently trades at $6.14.

Read our full analysis of Methode Electronics’s results here.

Thermon (NYSE: THR)

Creating the first packaged tracing systems, Thermon (NYSE: THR) is a leading provider of engineered industrial process heating solutions for process industries.

Thermon reported revenues of $134.4 million, down 1.5% year on year. This print lagged analysts' expectations by 3.3%. Overall, it was a slower quarter as it also recorded full-year EBITDA guidance meeting analysts’ expectations and EBITDA in line with analysts’ estimates.

Thermon delivered the highest full-year guidance raise among its peers. The stock is up 2.9% since reporting and currently trades at $27.72.

Read our full, actionable report on Thermon here, it’s free.

Atkore (NYSE: ATKR)

Protecting the things that power our world, Atkore (NYSE: ATKR) designs and manufactures electrical safety products.

Atkore reported revenues of $661.6 million, down 17.1% year on year. This result came in 2.1% below analysts' expectations. It was a softer quarter as it also produced full-year EBITDA guidance missing analysts’ expectations.

The stock is down 21.9% since reporting and currently trades at $62.04.

Read our full, actionable report on Atkore here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.