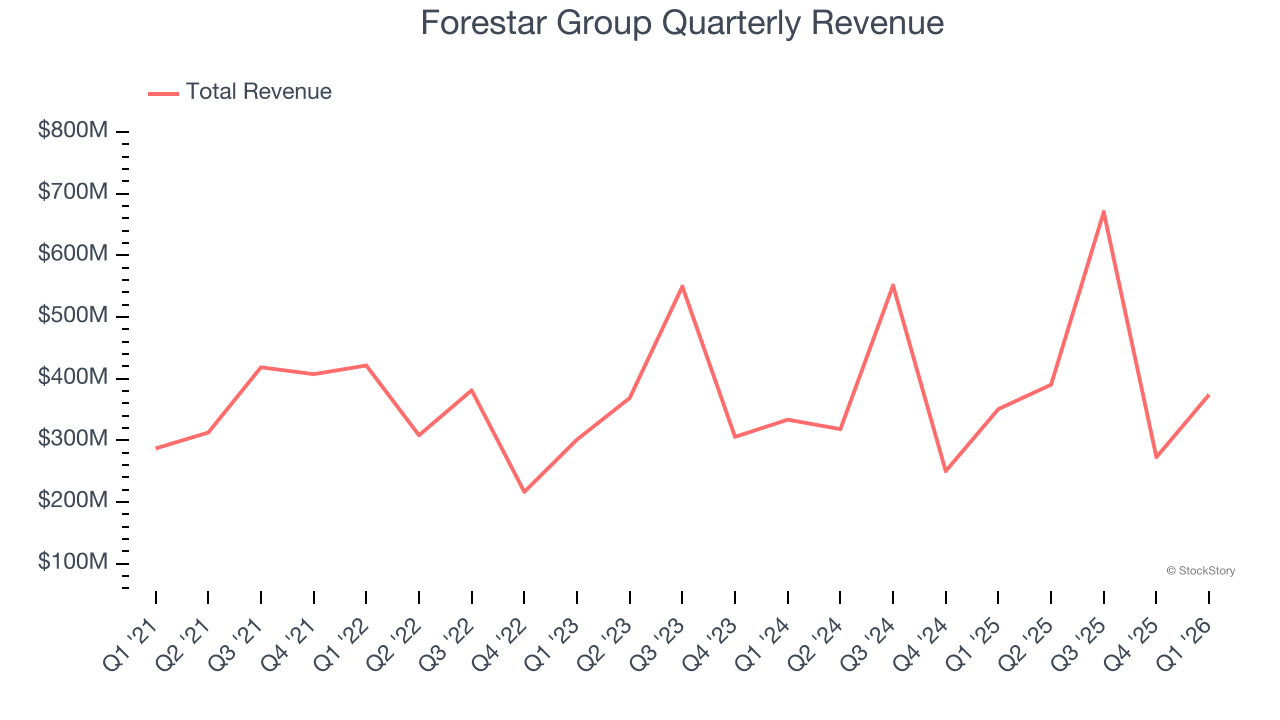

Residential lot developer Forestar Group (NYSE: FOR) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 6.6% year on year to $374.3 million. The company’s outlook for the full year was close to analysts’ estimates with revenue guided to $1.65 billion at the midpoint. Its GAAP profit of $0.63 per share was in line with analysts’ consensus estimates.

Is now the time to buy Forestar Group? Find out by accessing our full research report, it’s free.

Forestar Group (FOR) Q1 CY2026 Highlights:

- Revenue: $374.3 million vs analyst estimates of $374.1 million (6.6% year-on-year growth, in line)

- EPS (GAAP): $0.63 vs analyst estimates of $0.63 (in line)

- Adjusted Operating Income: $42.3 million vs analyst estimates of $41.69 million (11.3% margin, 1.5% beat)

- The company reconfirmed its revenue guidance for the full year of $1.65 billion at the midpoint

- Operating Margin: 11.3%, in line with the same quarter last year

- Sales Volumes fell 13.9% year on year (3.7% in the same quarter last year)

- Market Capitalization: $1.35 billion

Donald J. Tomnitz, Chairman of the Board, said, “The Forestar team achieved solid second quarter results including a 7% increase in revenues and an 8% increase in pre-tax income. Liquidity increased to $1.0 billion driven by financial discipline despite ongoing affordability constraints and cautious consumer sentiment that continue to impact the pace of new home sales. We continue to focus on maximizing returns in each of our projects by aligning the pace and price of lot sales with the timing of our investments to meet demand.

Company Overview

As a majority-owned subsidiary of homebuilding giant D.R. Horton, Forestar Group (NYSE: FOR) develops and sells finished residential lots to homebuilders, focusing primarily on land acquisition and development for single-family homes.

Revenue Growth

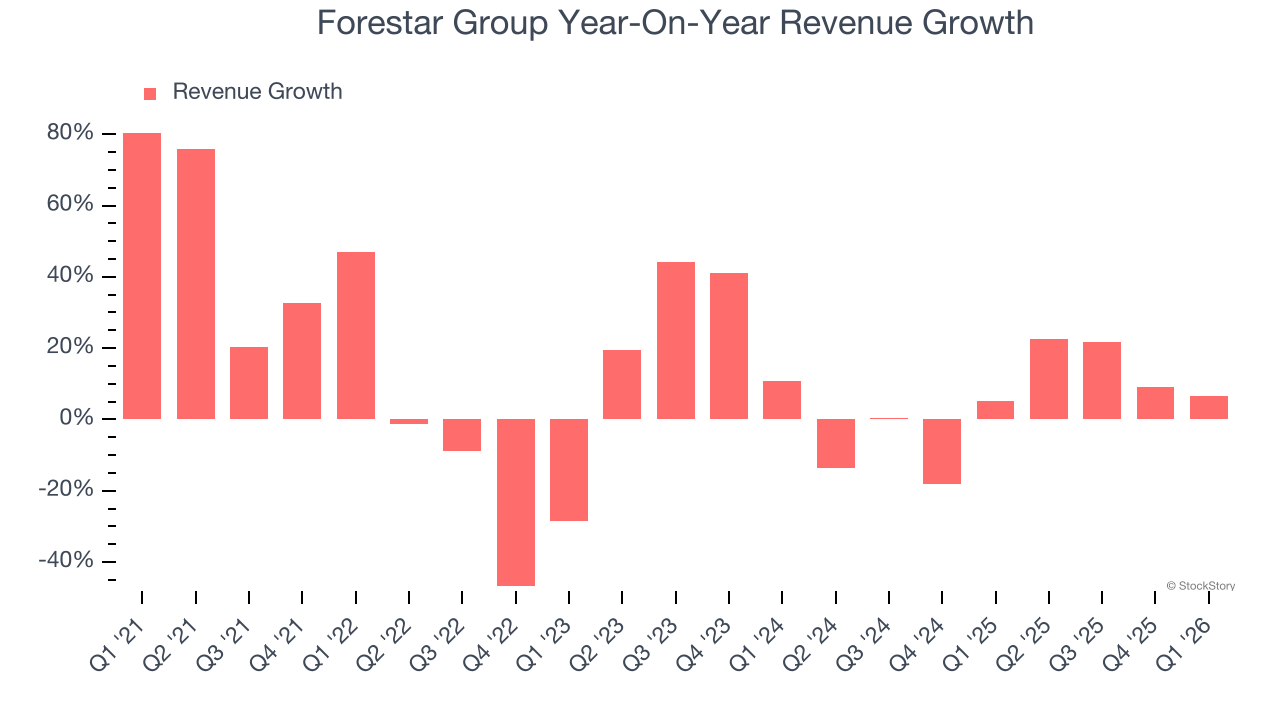

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Forestar Group’s sales grew at a weak 8.8% compounded annual growth rate over the last five years. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Forestar Group’s recent performance shows its demand has slowed as its annualized revenue growth of 4.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Forestar Group grew its revenue by 6.6% year on year, and its $374.3 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 2.2% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and indicates its products and services will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

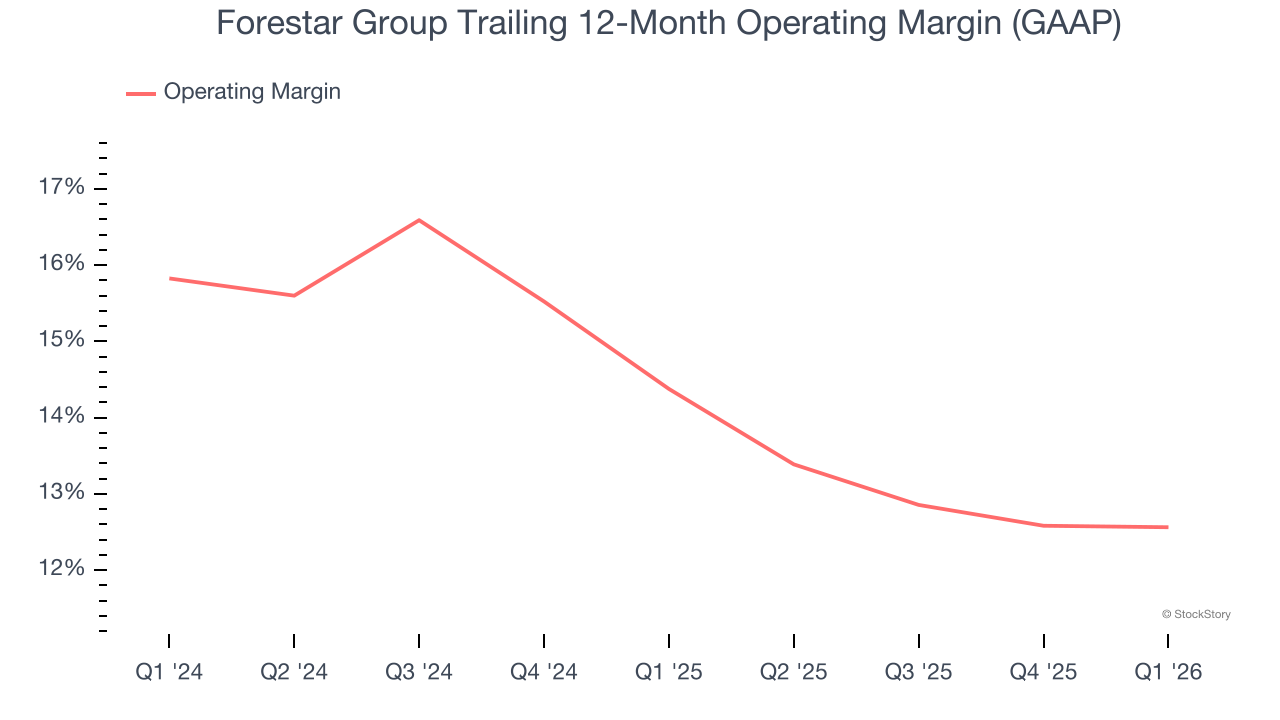

Forestar Group’s operating margin has shrunk over the last 12 months and averaged 13.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q1, Forestar Group generated an operating margin profit margin of 11.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

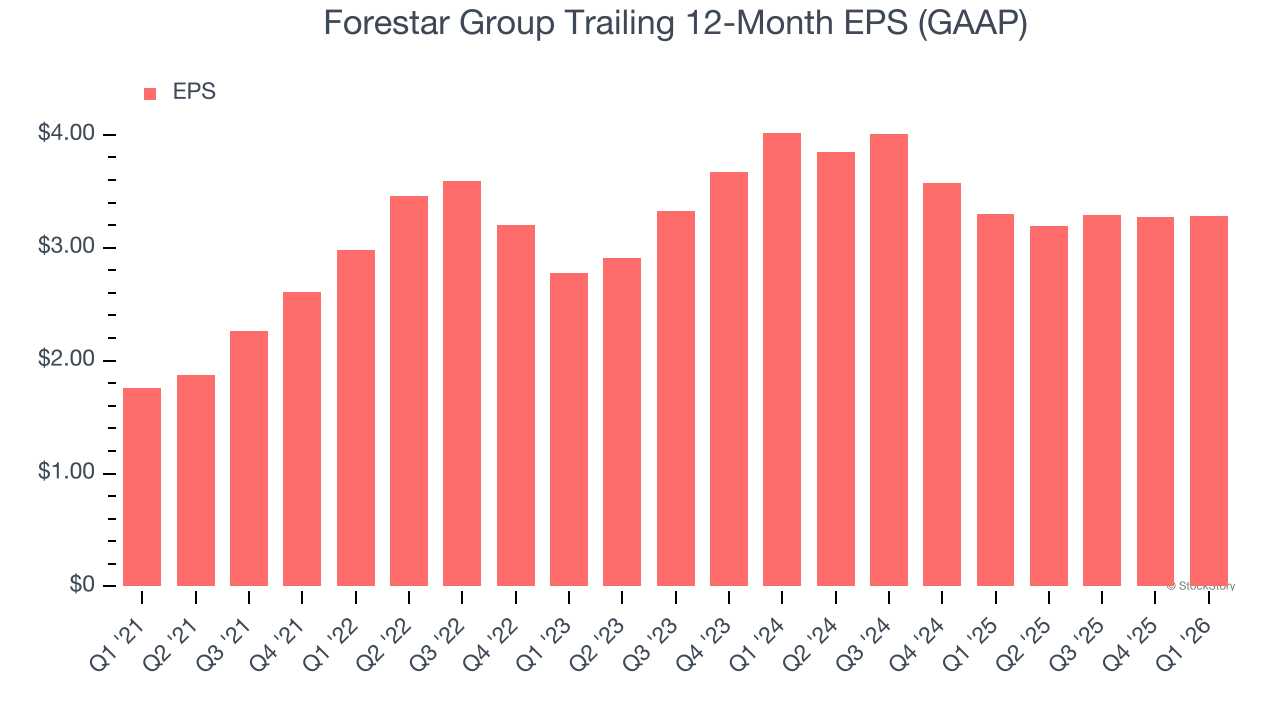

Forestar Group’s EPS grew at 13.3% compounded annual growth rate over the last five years. This performance was better than its revenue growth, but we take it with a grain of salt because its operating margin improvement was less than peers and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

In Q1, Forestar Group reported EPS of $0.63, up from $0.62 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Forestar Group’s full-year EPS of $3.28 to shrink by 8.1%.

Key Takeaways from Forestar Group’s Q1 Results

This quarter was without surprises. Revenue and EPS were both in line, and the company reaffirmed full-year guidance. On the positive side, operating income beat. Overall, this quarter wasn't overly exciting, but it was solid. The stock traded up 2.7% to $27.17 immediately after reporting.

So do we think Forestar Group is an attractive buy at the current price? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).