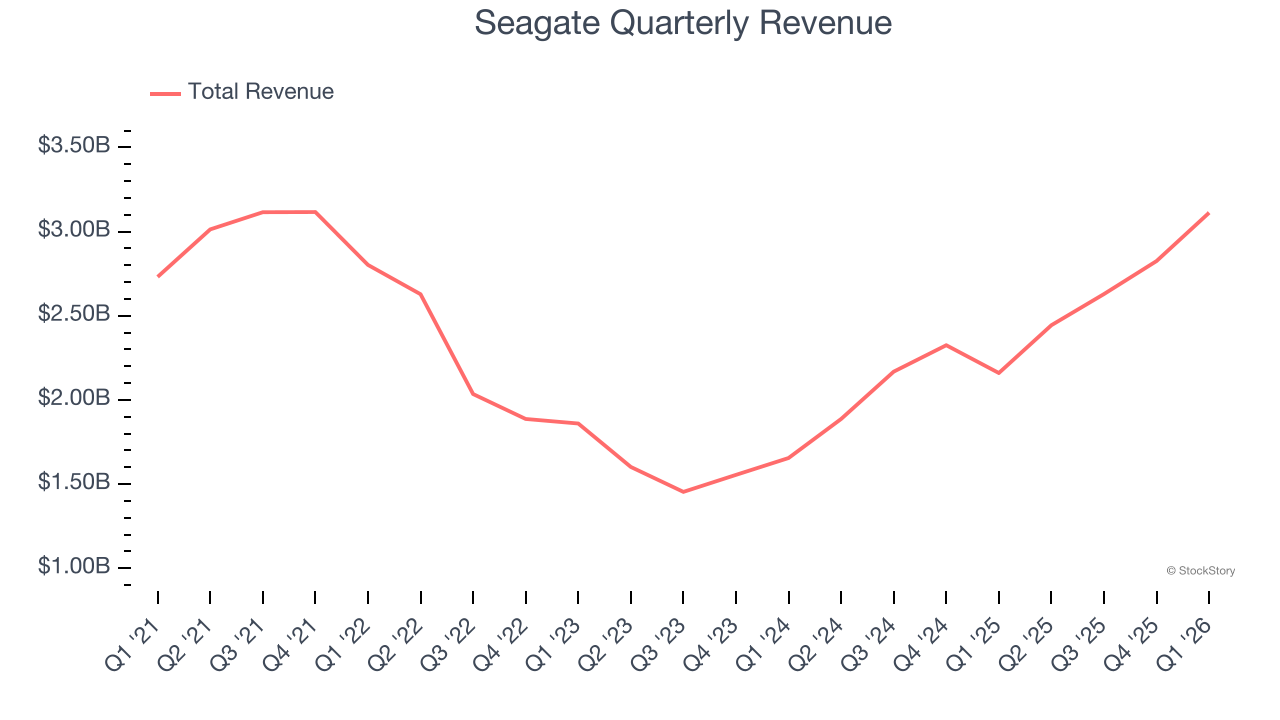

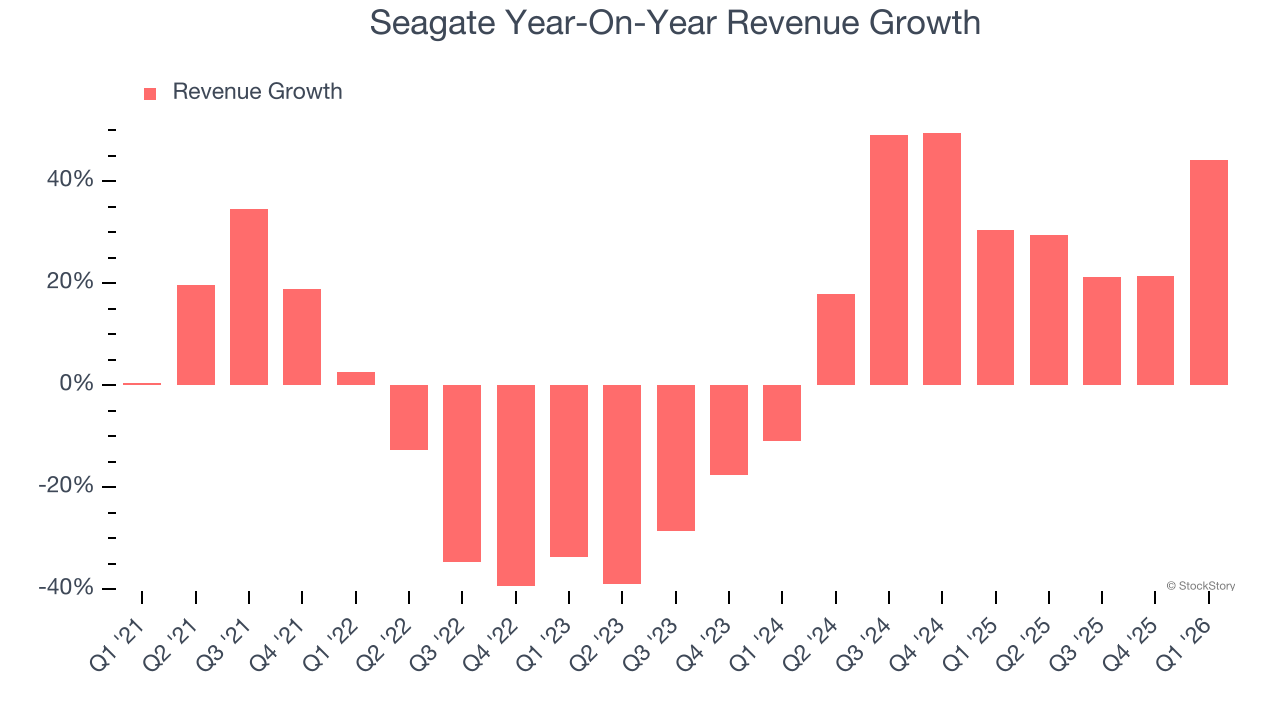

Data storage manufacturer Seagate (NASDAQ: STX) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 44.1% year on year to $3.11 billion. Its non-GAAP profit of $4.10 per share was 17.1% above analysts’ consensus estimates.

Is now the time to buy Seagate? Find out by accessing our full research report, it’s free.

Seagate (STX) Q1 CY2026 Highlights:

- Revenue: $3.11 billion vs analyst estimates of $2.95 billion (44.1% year-on-year growth, 5.4% beat)

- Adjusted EPS: $4.10 vs analyst estimates of $3.50 (17.1% beat)

- Adjusted EBITDA: $1.23 billion vs analyst estimates of $1.10 billion (39.6% margin, 12.2% beat)

- Operating Margin: 32.1%, up from 20% in the same quarter last year

- Free Cash Flow Margin: 30.6%, up from 10% in the same quarter last year

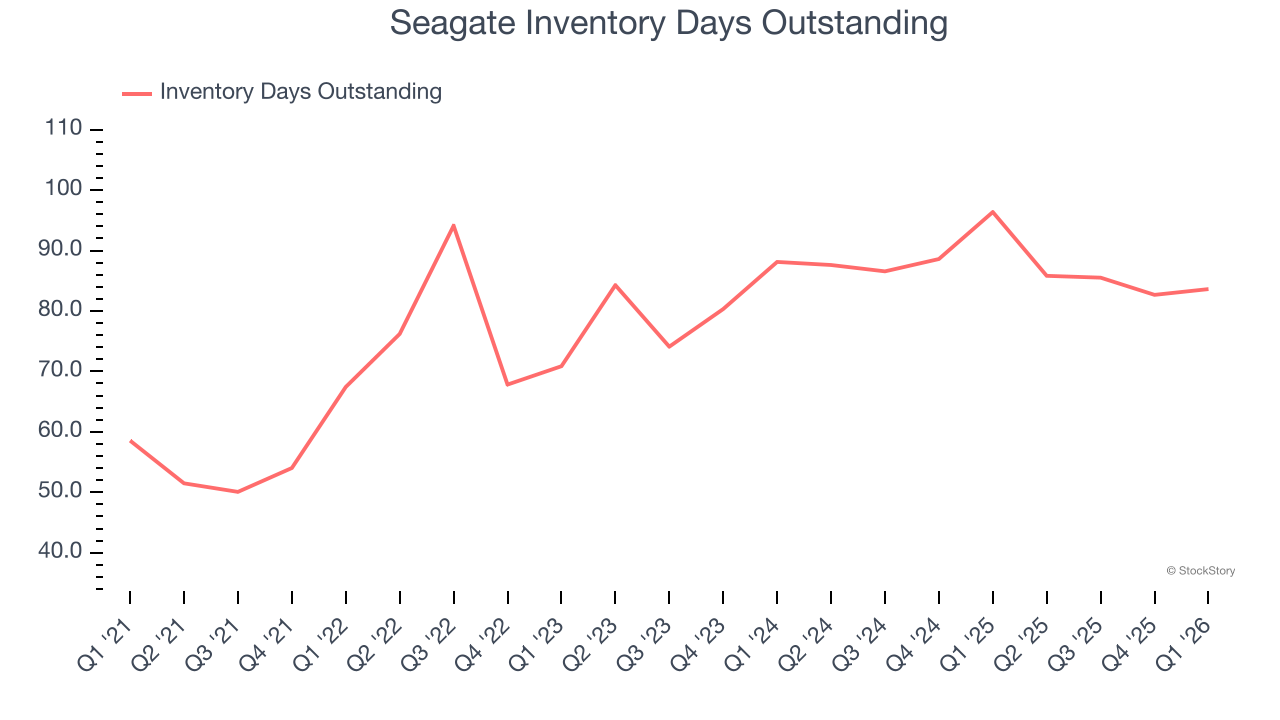

- Inventory Days Outstanding: 84, in line with the previous quarter

- Market Capitalization: $133.5 billion

Company Overview

One of two remaining major hard drive manufacturers after decades of industry consolidation, Seagate (NASDAQ: STX) manufactures hard disk drives and solid state drives that store data in data centers, cloud systems, and consumer devices.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Seagate’s sales grew at a tepid 1.6% compounded annual growth rate over the last five years. This wasn’t a great result, but there are still things to like about Seagate. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

We at StockStory place the most emphasis on long-term growth, but within semiconductors, a half-decade historical view may miss new demand cycles or industry trends like AI. Seagate’s annualized revenue growth of 32.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Seagate reported magnificent year-on-year revenue growth of 44.1%, and its $3.11 billion of revenue beat Wall Street’s estimates by 5.4%. Beyond the beat, this marks 8 straight quarters of growth, showing that the current upcycle has had a good run - a typical upcycle usually lasts 8-10 quarters.

Looking ahead, sell-side analysts expect revenue to grow 24.8% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and indicates the market sees success for its products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Seagate’s DIO came in at 84, which is 6 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Seagate’s Q1 Results

It was good to see Seagate beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 12.1% to $650.88 immediately following the results.

Seagate put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).