Industrial technology company Fortive (NYSE: FTV) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 7.7% year on year to $1.07 billion. Its non-GAAP profit of $0.70 per share was 8.9% above analysts’ consensus estimates.

Is now the time to buy Fortive? Find out by accessing our full research report, it’s free.

Fortive (FTV) Q1 CY2026 Highlights:

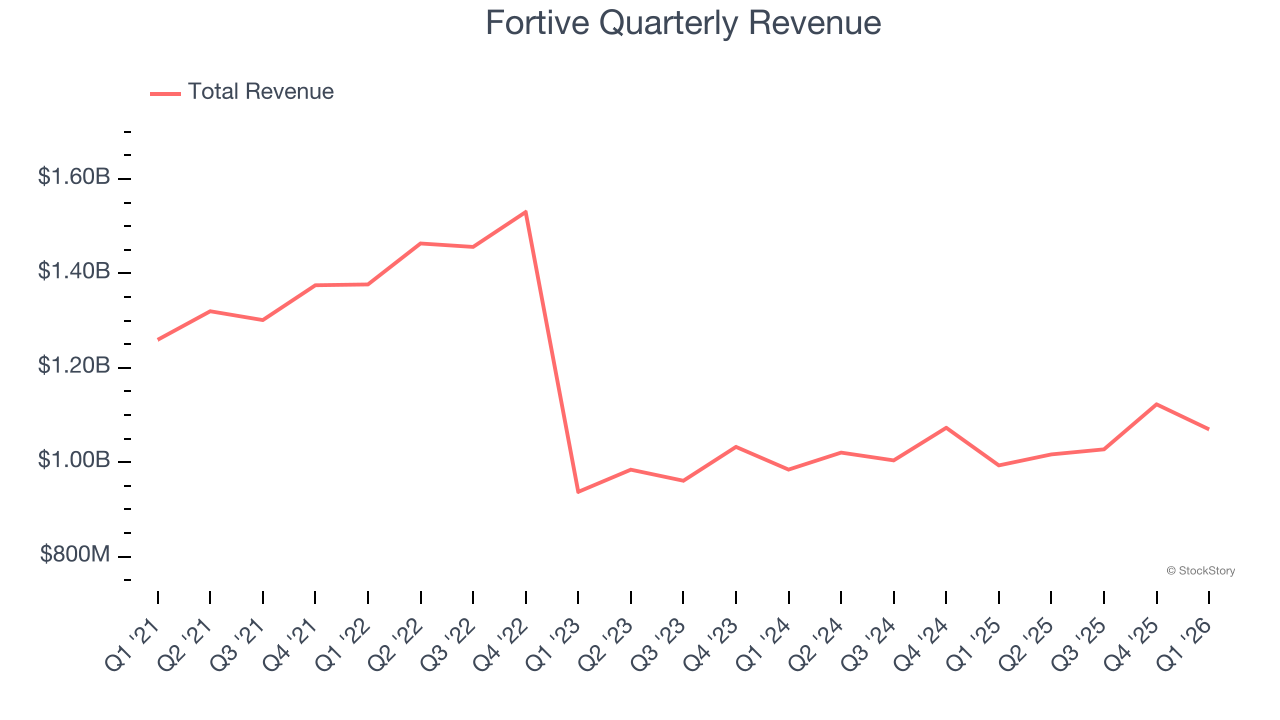

- Revenue: $1.07 billion vs analyst estimates of $1.04 billion (7.7% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.70 vs analyst estimates of $0.64 (8.9% beat)

- Adjusted EBITDA: $313.7 million vs analyst estimates of $296.9 million (29.3% margin, 5.7% beat)

- Management reiterated its full-year Adjusted EPS guidance of $2.95 at the midpoint

- Operating Margin: 17.9%, up from 16.6% in the same quarter last year

- Free Cash Flow Margin: 19.5%, up from 17.2% in the same quarter last year

- Market Capitalization: $19.01 billion

Company Overview

Taking its name from the Latin root of "strong", Fortive (NYSE: FTV) manufactures products and develops industrial software for numerous industries.

Revenue Growth

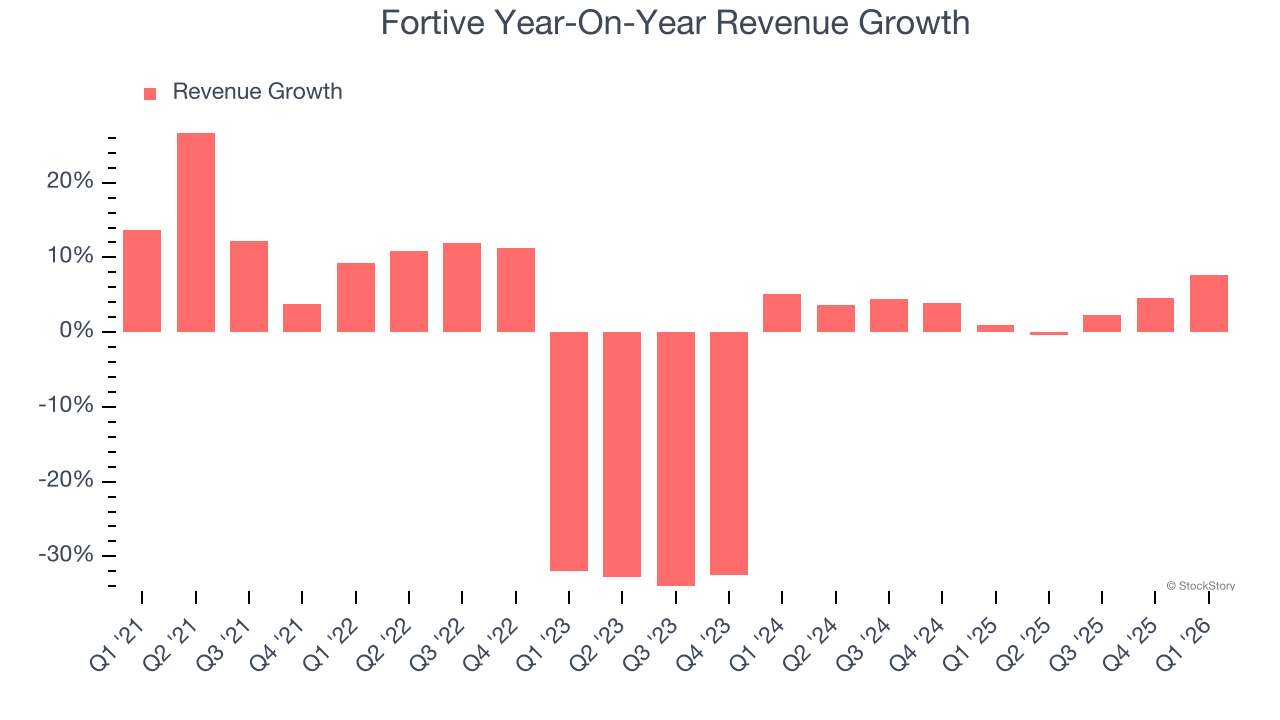

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Fortive’s demand was weak over the last five years as its sales fell at a 2.4% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Fortive’s annualized revenue growth of 3.4% over the last two years is above its five-year trend, which is encouraging.

This quarter, Fortive reported year-on-year revenue growth of 7.7%, and its $1.07 billion of revenue exceeded Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 2.9% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not catalyze better top-line performance yet.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

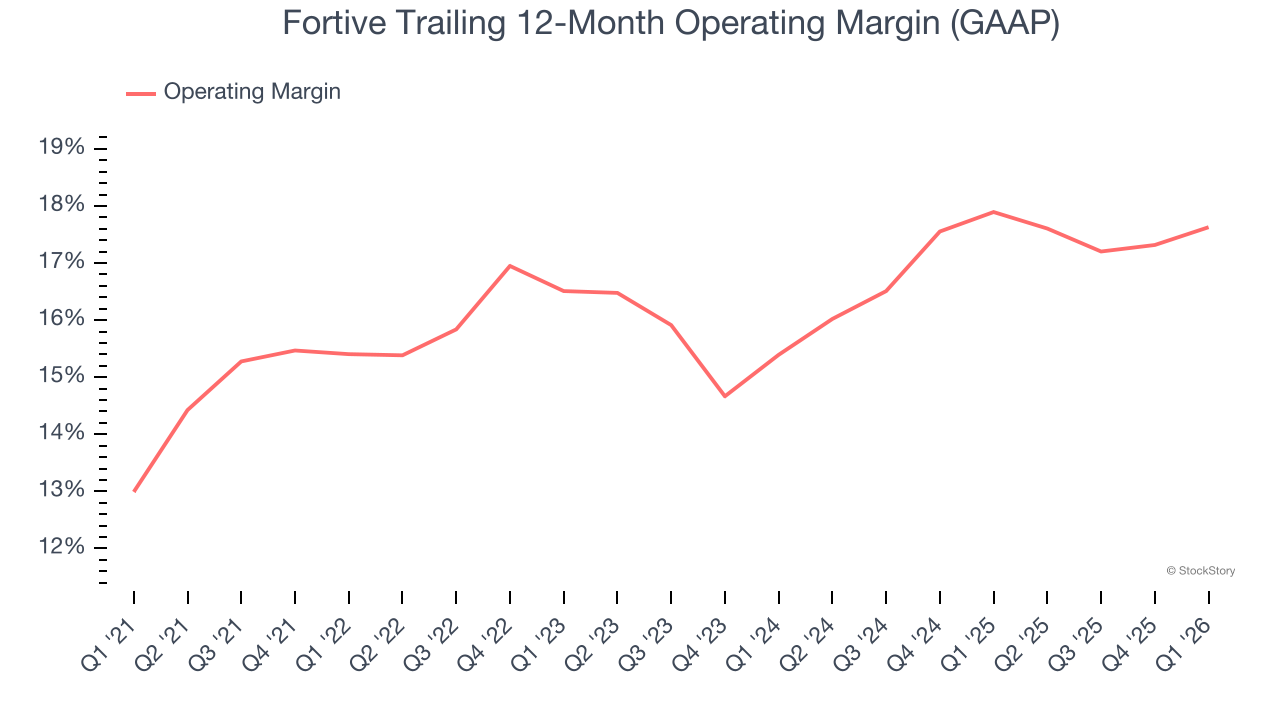

Fortive has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.5%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Fortive’s operating margin rose by 2.2 percentage points over the last five years, showing its efficiency has improved.

In Q1, Fortive generated an operating margin profit margin of 17.9%, up 1.3 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

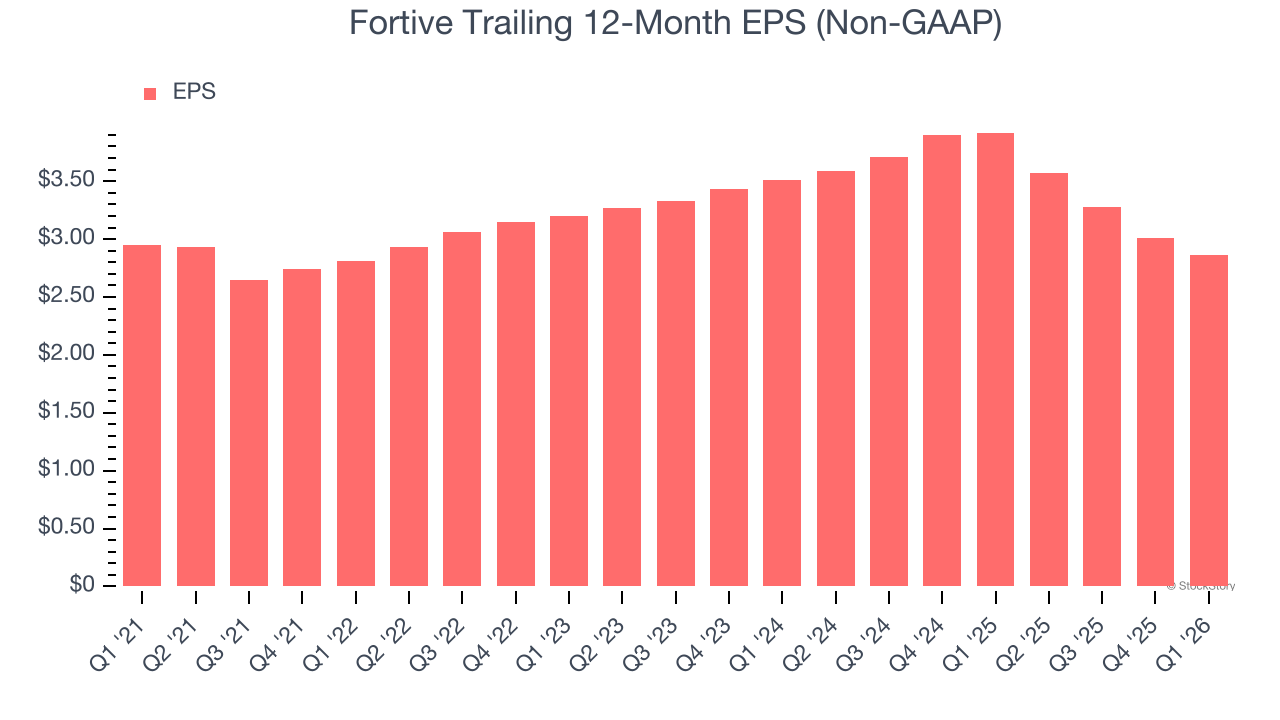

Fortive’s flat EPS over the last five years was weak but better than its 2.4% annualized revenue declines. This tells us management adapted its cost structure.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Fortive, its two-year annual EPS declines of 9.7% show its recent history was to blame for its underperformance over the last five years. These results were bad no matter how you slice the data.

In Q1, Fortive reported adjusted EPS of $0.70, down from $0.85 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.9%. Over the next 12 months, Wall Street expects Fortive’s full-year EPS of $2.86 to grow 5.5%.

Key Takeaways from Fortive’s Q1 Results

We were impressed by how significantly Fortive blew past analysts’ adjusted operating income expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance was in line. Zooming out, we think this was a solid print. The stock remained flat at $61.90 immediately following the results.

Fortive put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).