Shareholders of GitLab would probably like to forget the past six months even happened. The stock dropped 40.3% and now trades at $25.36. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for GTLB? Find out in our full research report, it’s free.

Why Is GitLab a Good Business?

With its all-remote workforce pioneering a new approach to software development, GitLab (NASDAQ: GTLB) provides a single-application DevSecOps platform that helps development, operations, and security teams collaborate to build, secure, and deploy software faster.

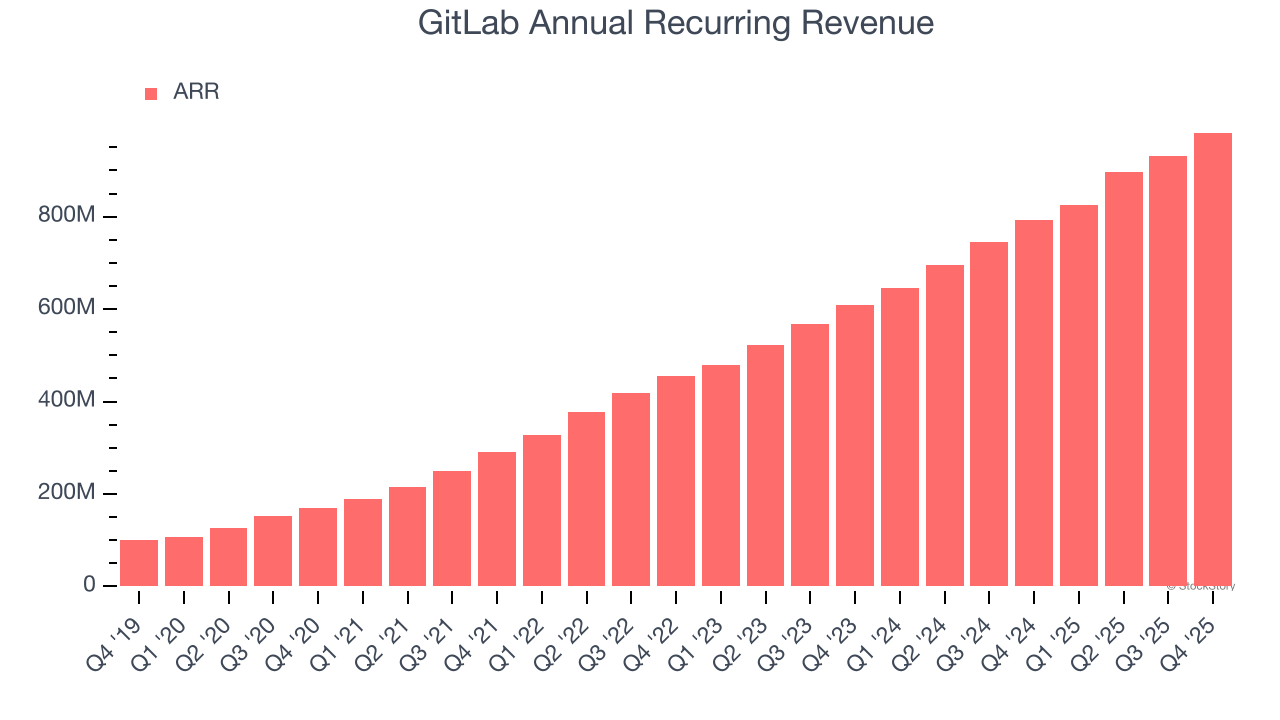

1. ARR Surges as Recurring Revenue Flows In

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

GitLab’s ARR punched in at $981.9 million in Q4, and over the last four quarters, its year-on-year growth averaged 26.4%. This performance was fantastic and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes GitLab a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

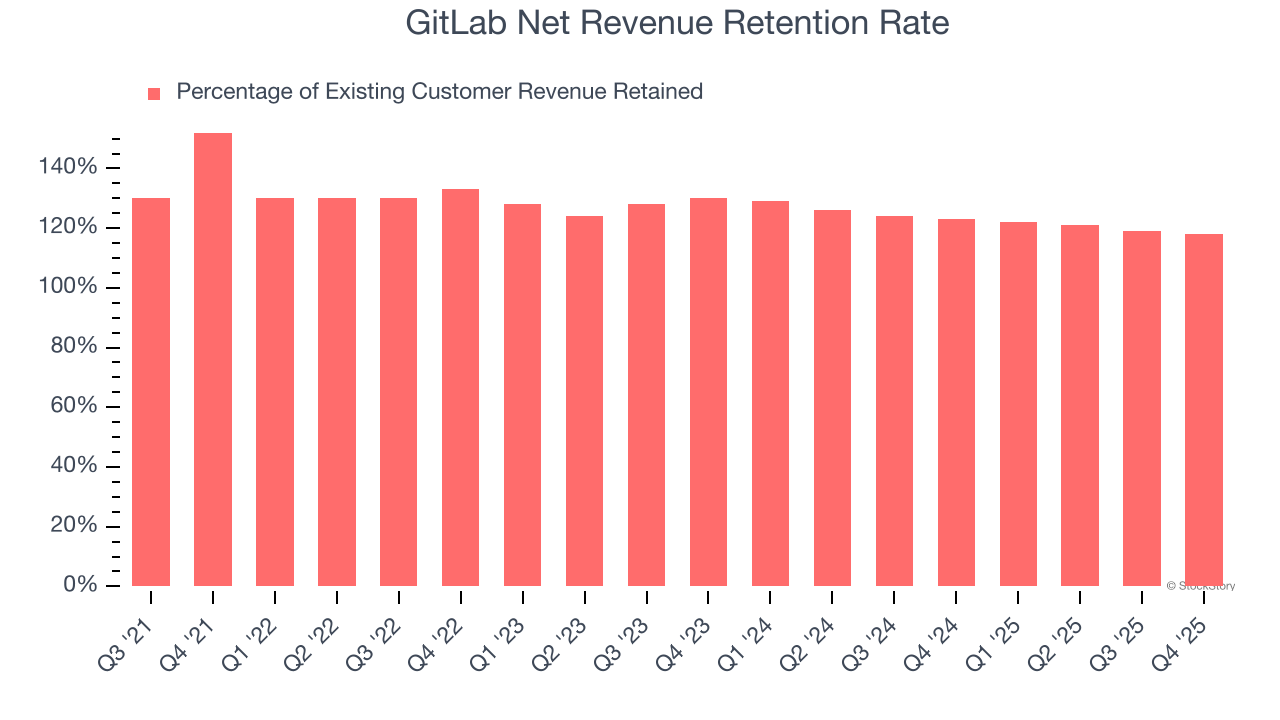

2. Strong Retention Supports Growth and Profitability

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

GitLab’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 120% in Q4. This means GitLab would’ve grown its revenue by 20% even if it didn’t win any new customers over the last 12 months.

Despite falling over the last year, GitLab still has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

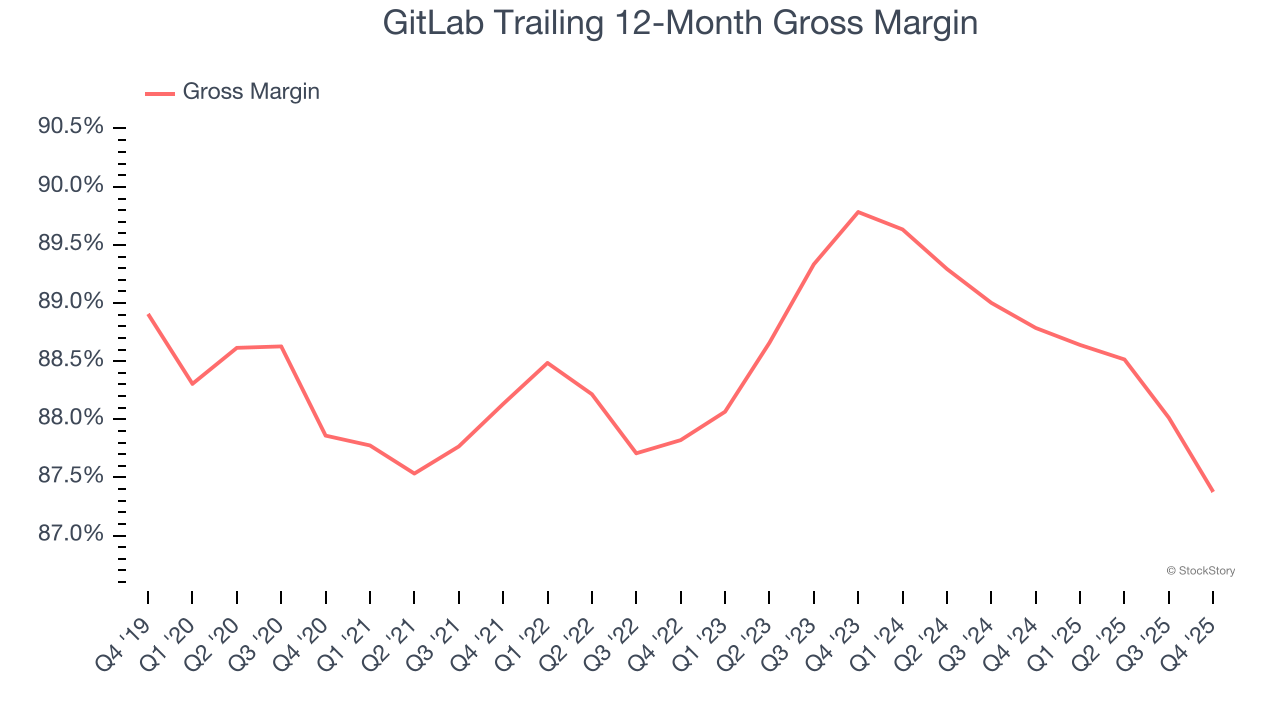

3. Elite Gross Margin Powers Best-In-Class Business Model

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

GitLab’s gross margin is one of the best in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an elite 87.4% gross margin over the last year. Said differently, roughly $87.38 was left to spend on selling, marketing, and R&D for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. GitLab has seen gross margins decline by 2.4 percentage points over the last 2 year, which is among the worst in the software space.

Final Judgment

These are just a few reasons why we think GitLab is a great business. After the recent drawdown, the stock trades at 3.8× forward price-to-sales (or $25.36 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.