ABM currently trades at $40.69 per share and has shown little upside over the past six months, posting a small loss of 3.1%. The stock also fell short of the S&P 500’s 7.1% gain during that period.

Is now the time to buy ABM, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is ABM Not Exciting?

We don't have much confidence in ABM. Here are three reasons there are better opportunities than ABM and a stock we'd rather own.

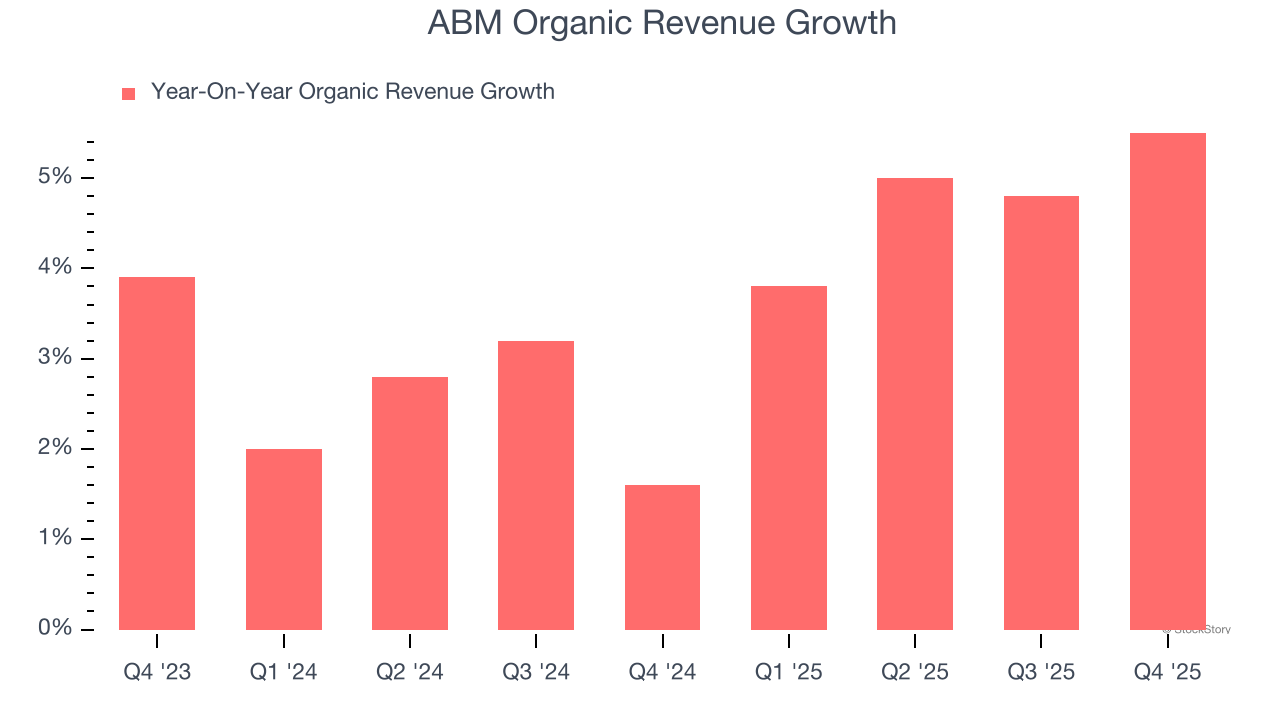

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Industrial & Environmental Services companies. This metric gives visibility into ABM’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, ABM’s organic revenue averaged 3.6% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

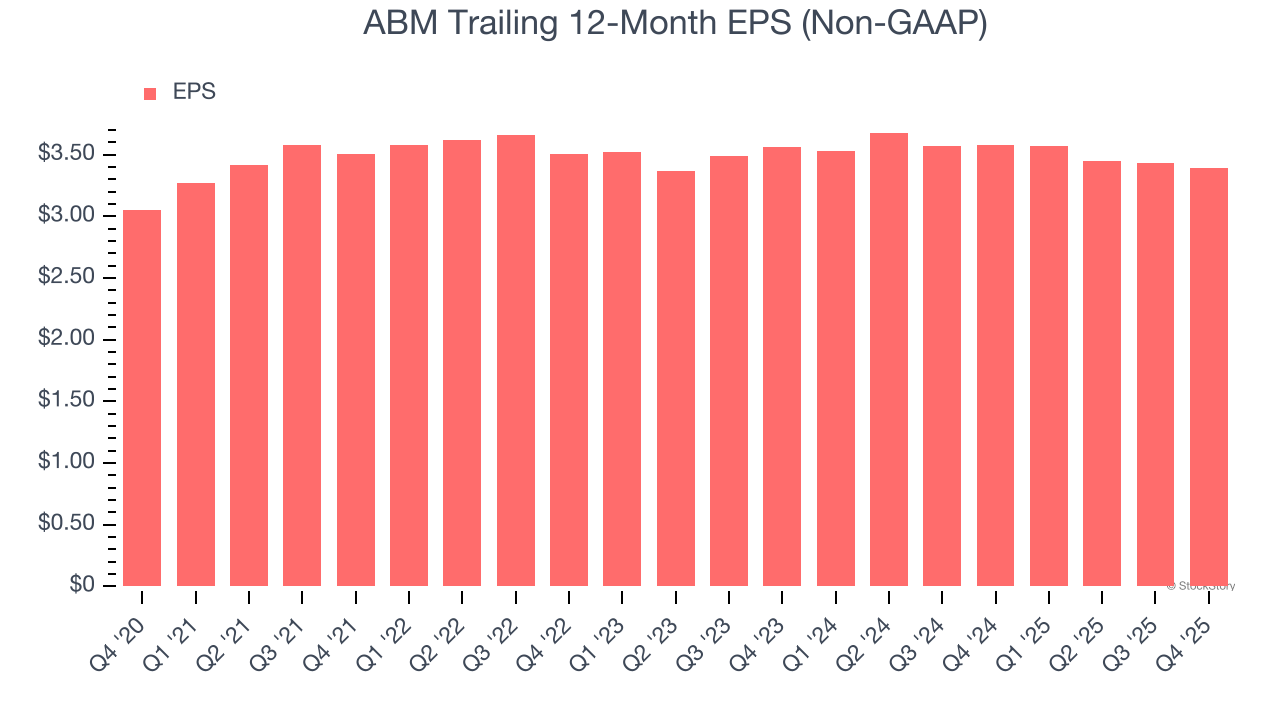

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

ABM’s EPS grew at a weak 2.1% compounded annual growth rate over the last five years, lower than its 8.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

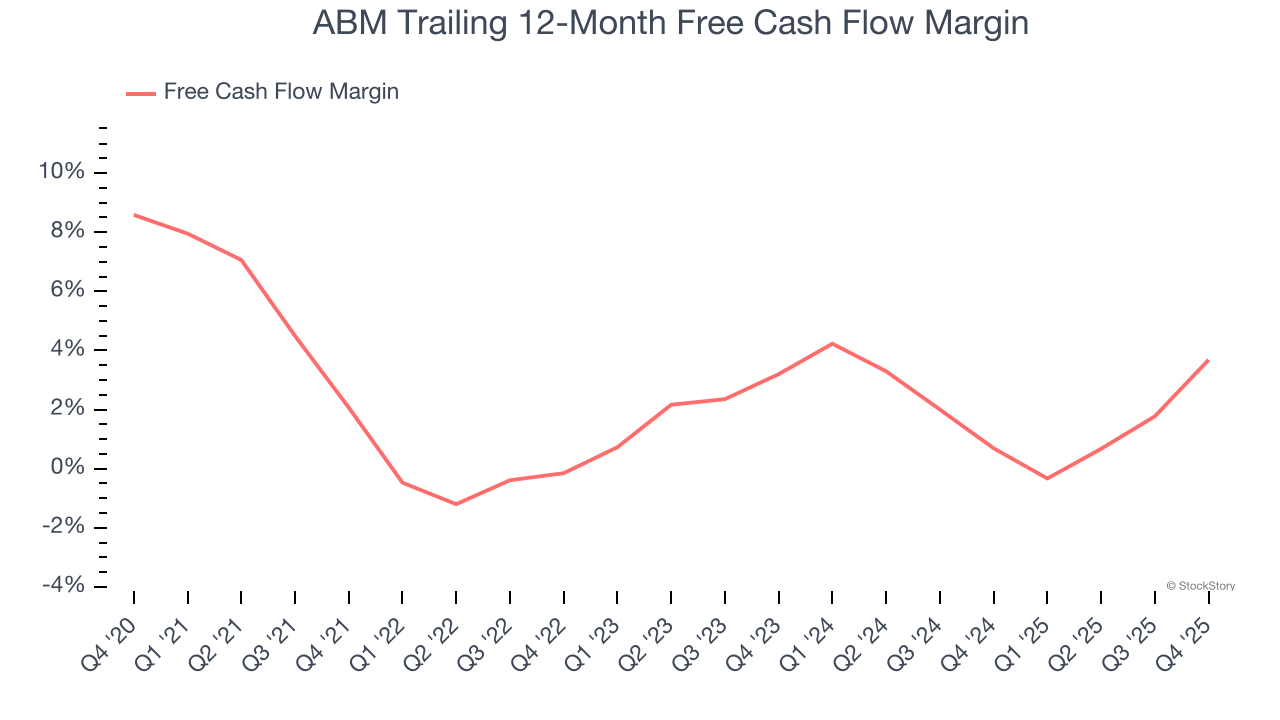

3. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

ABM has shown poor cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.9%, below what we’d expect for a business services business.

Final Judgment

ABM isn’t a terrible business, but it doesn’t pass our bar. With its shares trailing the market in recent months, the stock trades at 9.9× forward P/E (or $40.69 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than ABM

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.