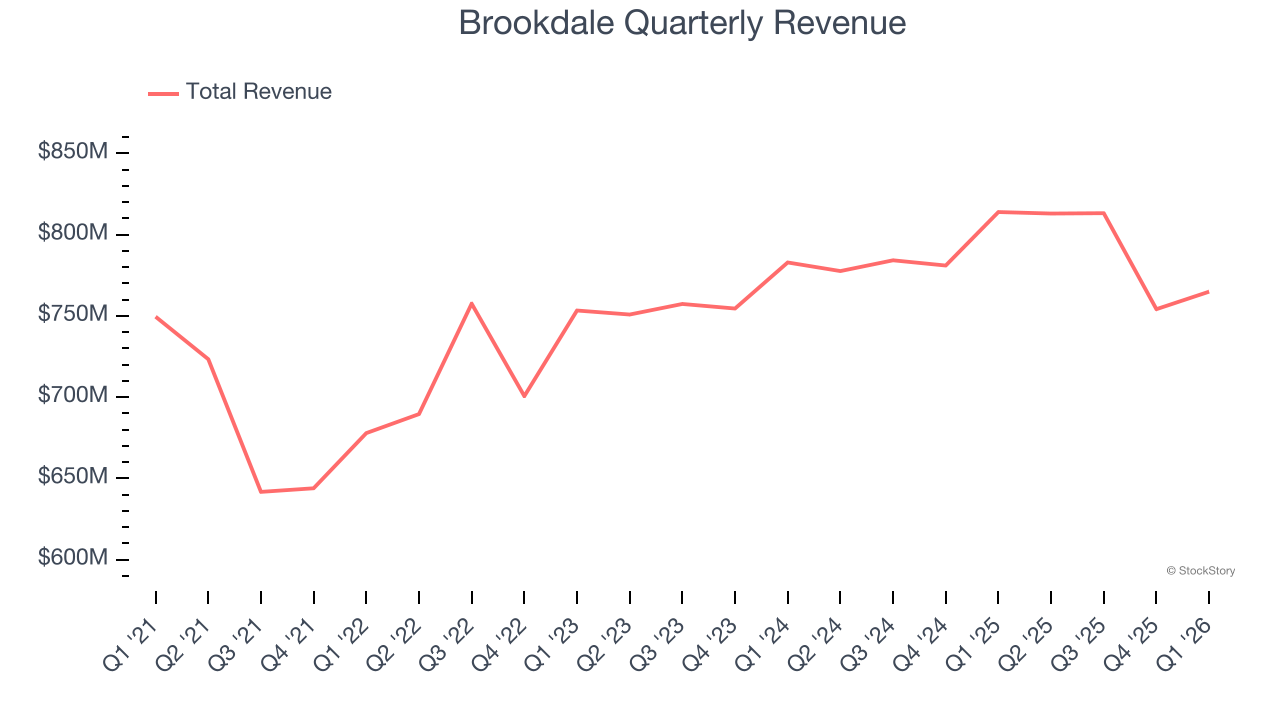

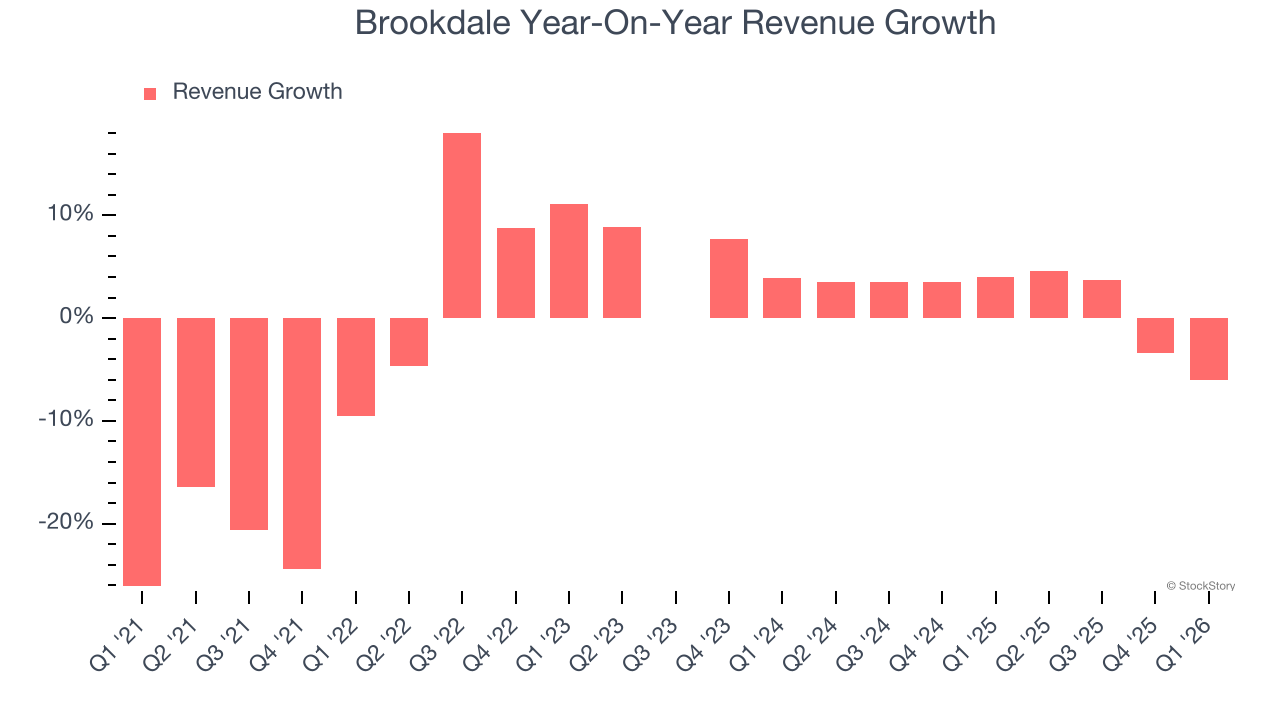

Senior living provider Brookdale Senior Living (NYSE: BKD) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 6% year on year to $764.9 million. Its GAAP loss of $0.03 per share was in line with analysts’ consensus estimates.

Is now the time to buy Brookdale? Find out by accessing our full research report, it’s free.

Brookdale (BKD) Q1 CY2026 Highlights:

- Revenue: $764.9 million vs analyst estimates of $771.2 million (6% year-on-year decline, 0.8% miss)

- EPS (GAAP): -$0.03 vs analyst estimates of -$0.02 (in line)

- Adjusted EBITDA: $131.1 million vs analyst estimates of $135.8 million (17.1% margin, 3.5% miss)

- EBITDA guidance for the full year is $509 million at the midpoint, in line with analyst expectations

- Operating Margin: 6.8%, up from 3.9% in the same quarter last year

- Free Cash Flow was -$25.59 million compared to -$18.42 million in the same quarter last year

- Market Capitalization: $3.34 billion

"Over the past six months, we have executed on a significant number of meaningful changes that have Brookdale strongly positioned for the next wave of growth," said Nick Stengle, Brookdale's Chief Executive Officer.

Company Overview

With a network of over 650 communities serving approximately 59,000 residents across 41 states, Brookdale Senior Living (NYSE: BKD) operates senior living communities across the United States, offering independent living, assisted living, memory care, and continuing care retirement communities.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Brookdale struggled to consistently increase demand as its $3.15 billion of sales for the trailing 12 months was close to its revenue five years ago. This wasn’t a great result and suggests it’s a lower quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Brookdale’s annualized revenue growth of 1.6% over the last two years is above its five-year trend, which is encouraging.

This quarter, Brookdale missed Wall Street’s estimates and reported a rather uninspiring 6% year-on-year revenue decline, generating $764.9 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 4.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

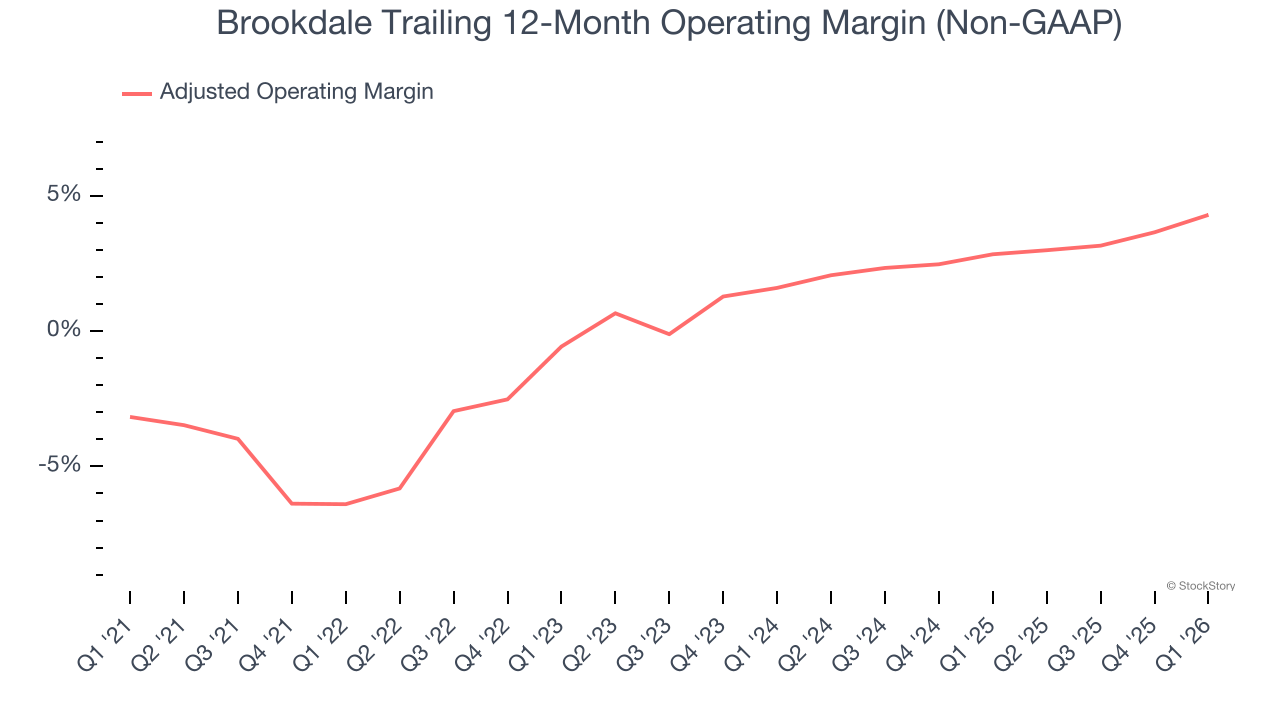

Adjusted Operating Margin

Brookdale was roughly breakeven when averaging the last five years of quarterly operating profits, lousy for a healthcare business.

On the plus side, Brookdale’s adjusted operating margin rose by 10.7 percentage points over the last five years. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 2.7 percentage points on a two-year basis.

In Q1, Brookdale generated an adjusted operating margin profit margin of 7.3%, up 2.7 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

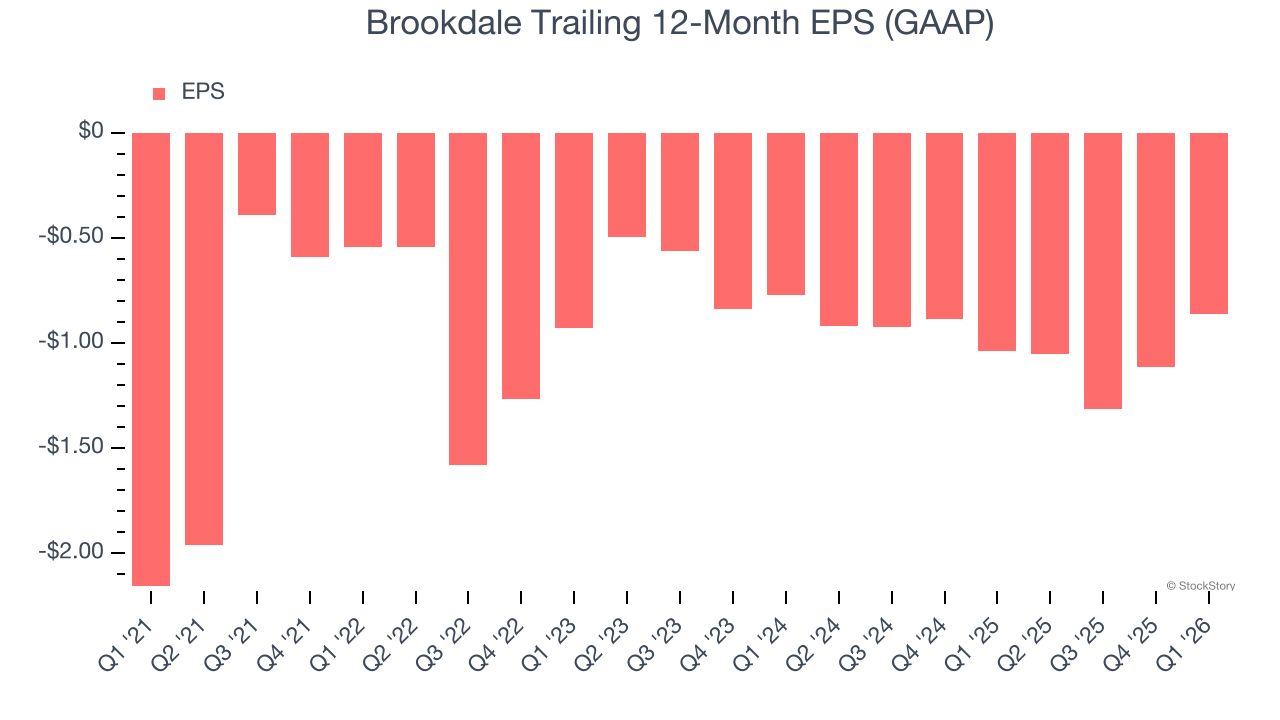

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Brookdale’s full-year earnings are still negative, it reduced its losses and improved its EPS by 16.7% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Brookdale reported EPS of negative $0.03, up from negative $0.28 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Brookdale to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.86 will advance to negative $0.12.

Key Takeaways from Brookdale’s Q1 Results

We struggled to find many positives in these results. Its EPS was in line and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.6% to $13.81 immediately following the results.

Brookdale may have had a tough quarter, but does that actually create an opportunity to invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).