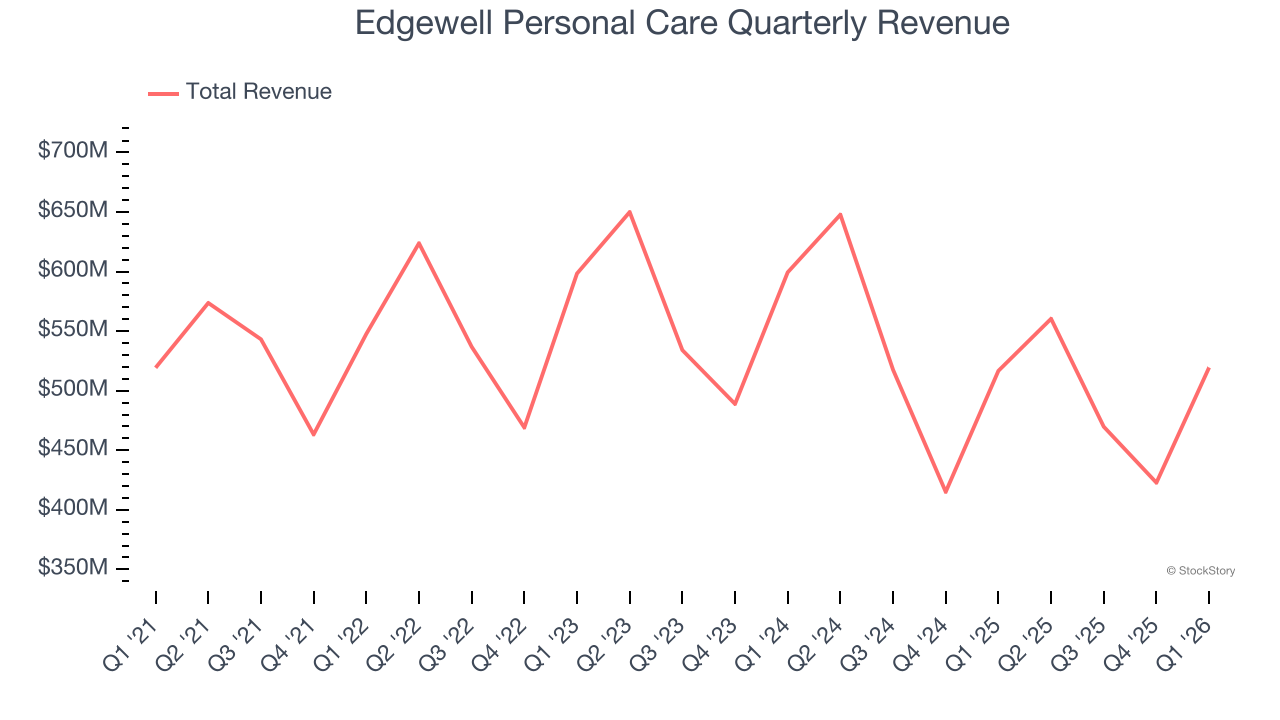

Personal care company Edgewell Personal Care (NYSE: EPC) met Wall Street’s revenue expectations in Q1 CY2026, but sales were flat year on year at $519.5 million. Its non-GAAP profit of $0.60 per share was 36.4% above analysts’ consensus estimates.

Is now the time to buy Edgewell Personal Care? Find out by accessing our full research report, it’s free.

Edgewell Personal Care (EPC) Q1 CY2026 Highlights:

- Revenue: $519.5 million vs analyst estimates of $517.6 million (flat year on year, in line)

- Adjusted EPS: $0.60 vs analyst estimates of $0.44 (36.4% beat)

- Adjusted EBITDA: $73.8 million vs analyst estimates of $63.49 million (14.2% margin, 16.2% beat)

- EBITDA guidance for the full year is $255 million at the midpoint, in line with analyst expectations

- Operating Margin: 3.5%, down from 9.5% in the same quarter last year

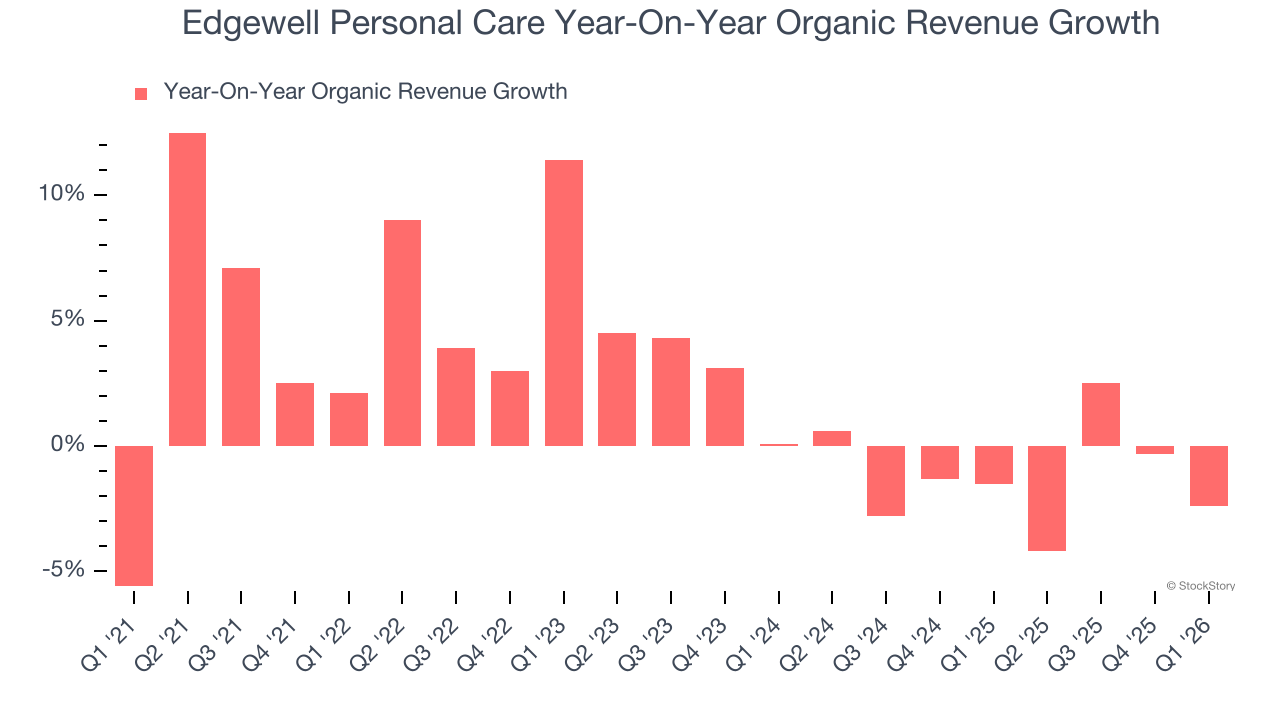

- Organic Revenue fell 2.4% year on year (beat)

- Market Capitalization: $1.07 billion

"We delivered a strong second quarter, with results ahead of our expectations, driven by improved execution and innovation that is resonating with consumers, reflected in the continued momentum in brands like Cremo, Hawaiian Tropic and Billie," said Rod Little, President and Chief Executive Officer of Edgewell Personal Care.

Company Overview

Boasting brands such as Banana Boat, Schick, and Skintimate, Edgewell Personal Care (NYSE: EPC) sells personal care products in the skin and sun care, shave, and feminine care categories.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.97 billion in revenue over the past 12 months, Edgewell Personal Care is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Edgewell Personal Care’s demand was weak over the last three years. Its sales fell by 4% annually, a rough starting point for our analysis.

This quarter, Edgewell Personal Care’s $519.5 million of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months. While this projection suggests its newer products will catalyze better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Edgewell Personal Care’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 1.2% year on year.

In the latest quarter, Edgewell Personal Care’s organic sales fell by 2.4% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Edgewell Personal Care’s Q1 Results

We were impressed by how significantly Edgewell Personal Care blew past analysts’ EBITDA expectations this quarter. We were also excited its organic revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its adjusted operating income missed and its gross margin fell short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. The stock remained flat at $22.84 immediately after reporting.

So should you invest in Edgewell Personal Care right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).