Industrial distributor DXP Enterprises (NASDAQ: DXPE) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 9.5% year on year to $521.7 million. Its non-GAAP profit of $1.26 per share was 2.3% below analysts’ consensus estimates.

Is now the time to buy DXP? Find out by accessing our full research report, it’s free.

DXP (DXPE) Q1 CY2026 Highlights:

- Revenue: $521.7 million vs analyst estimates of $531.5 million (9.5% year-on-year growth, 1.9% miss)

- Adjusted EPS: $1.26 vs analyst expectations of $1.29 (2.3% miss)

- Adjusted EBITDA: $57.81 million vs analyst estimates of $59.1 million (11.1% margin, 2.2% miss)

- Operating Margin: 8.1%, in line with the same quarter last year

- Free Cash Flow was $26.28 million, up from -$16.94 million in the same quarter last year

- Market Capitalization: $2.82 billion

David R. Little, Chairman and Chief Executive Officer commented, "The Company posted first quarter financial results, delivering solid sales, adjusted EBITDA, earnings per share and free cash flow. First quarter results reflect the continued execution of our growth strategy. This resulted in operating leverage that produced diluted earnings per share of $1.22. DXP’s fiscal year 2026 first quarter sales were $521.7 million, or a 9.5 percent growth over the same period in 2025. Adjusted EBITDA was $57.8 million in the quarter. During the first quarter of 2026, sales were $338.0 million for Service Centers, $118.7 million for Innovative Pumping Solutions, and $65.0 million for Supply Chain Services. Overall, we are pleased with our performance and the progress DXP continues to make as a growth company. "

Company Overview

Founded during the emergence of Big Oil in Texas, DXP (NASDAQ: DXPE) provides pumps, valves, and other industrial components.

Revenue Growth

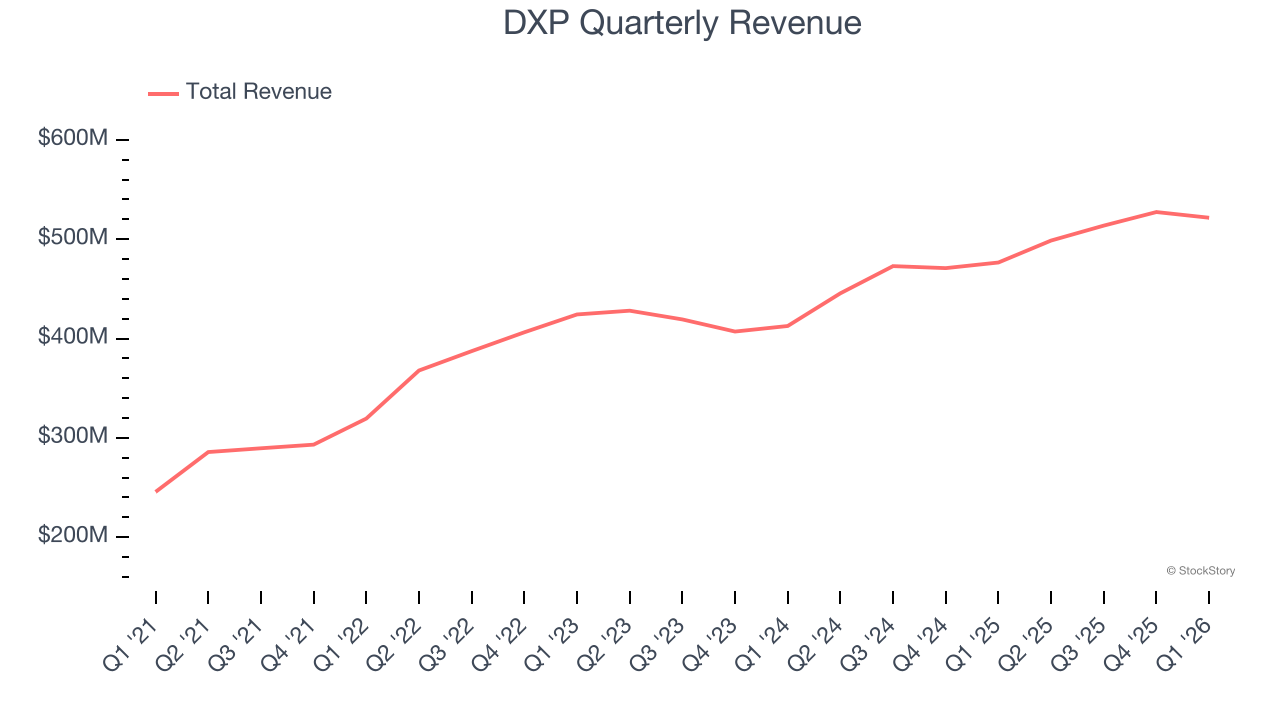

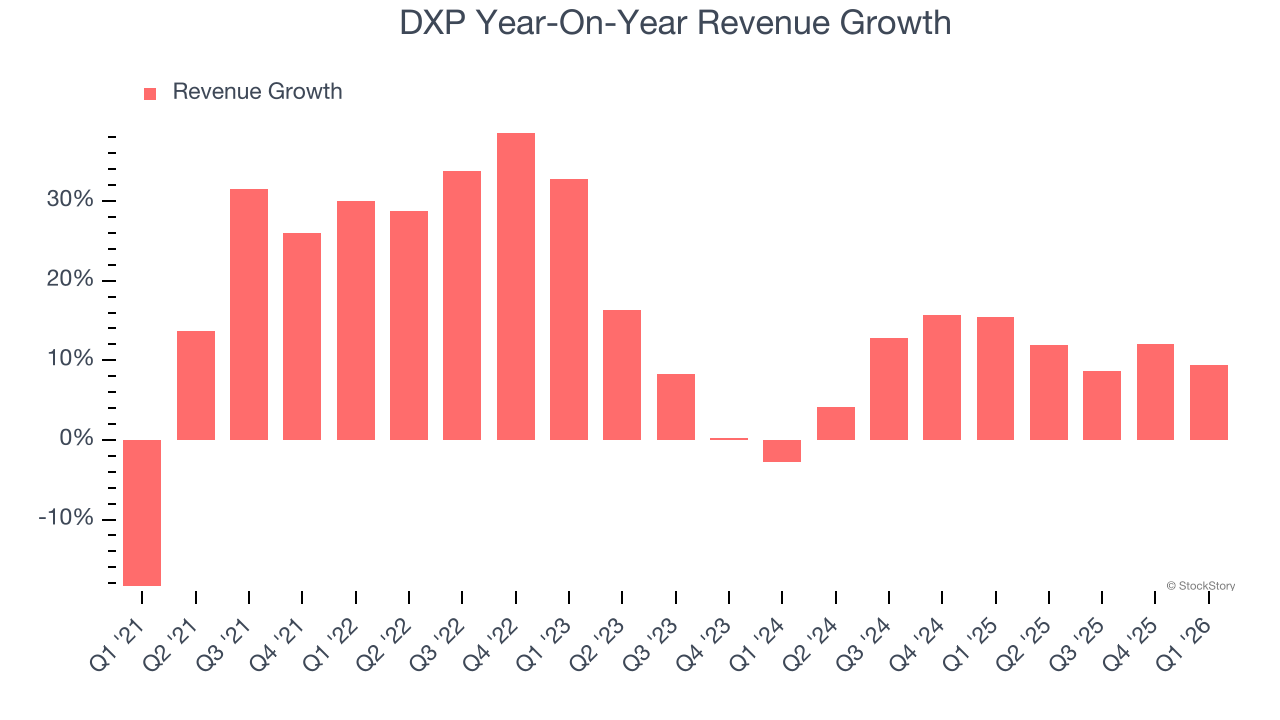

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Luckily, DXP’s sales grew at an incredible 16.8% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. DXP’s annualized revenue growth of 11.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, DXP’s revenue grew by 9.5% year on year to $521.7 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.9% over the next 12 months, a slight deceleration versus the last two years. Despite the slowdown, this projection is above average for the sector and implies the market sees some success for its newer products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

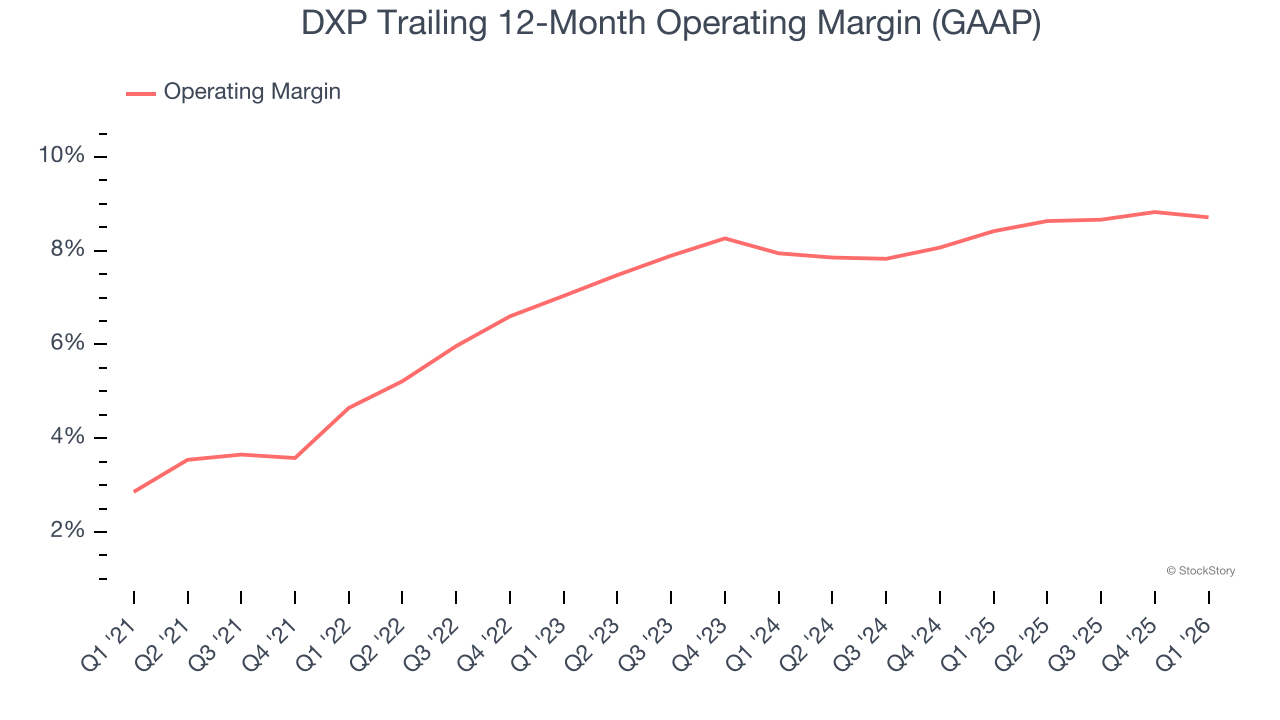

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

DXP was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.6% was weak for an industrials business.

On the plus side, DXP’s operating margin rose by 4.1 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, DXP generated an operating margin profit margin of 8.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

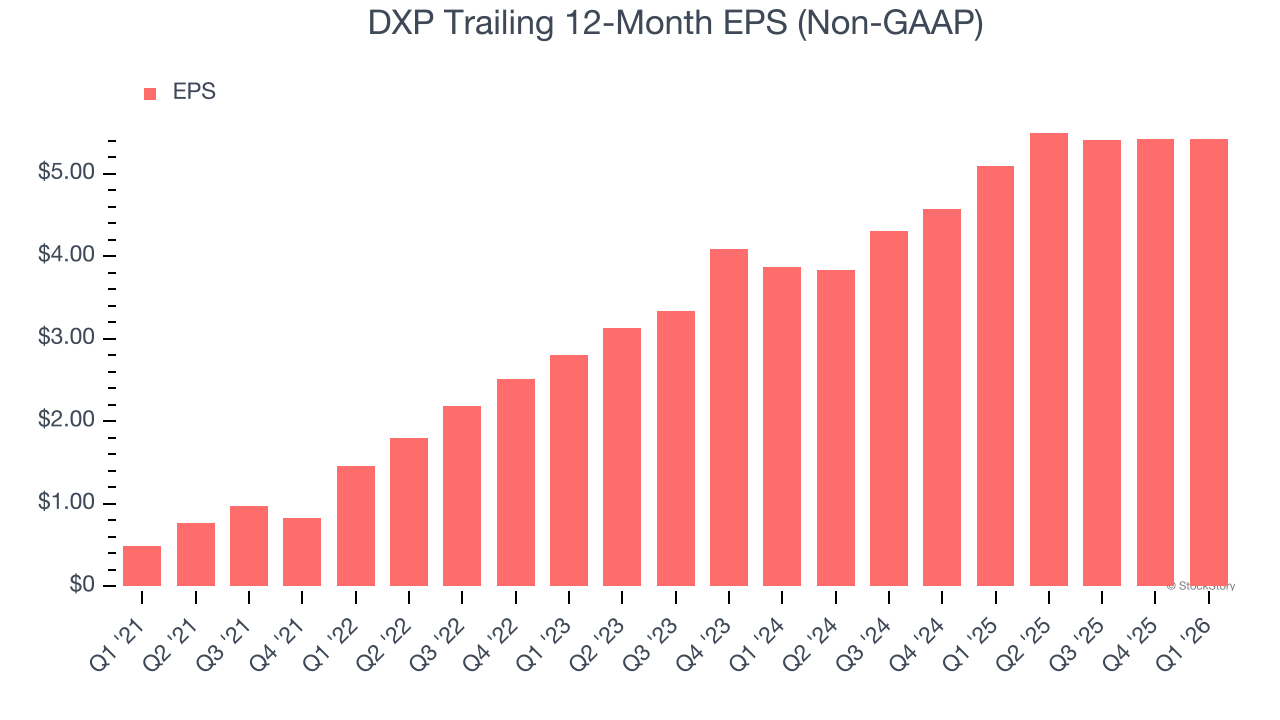

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

DXP’s EPS grew at 61.7% compounded annual growth rate over the last five years, higher than its 16.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

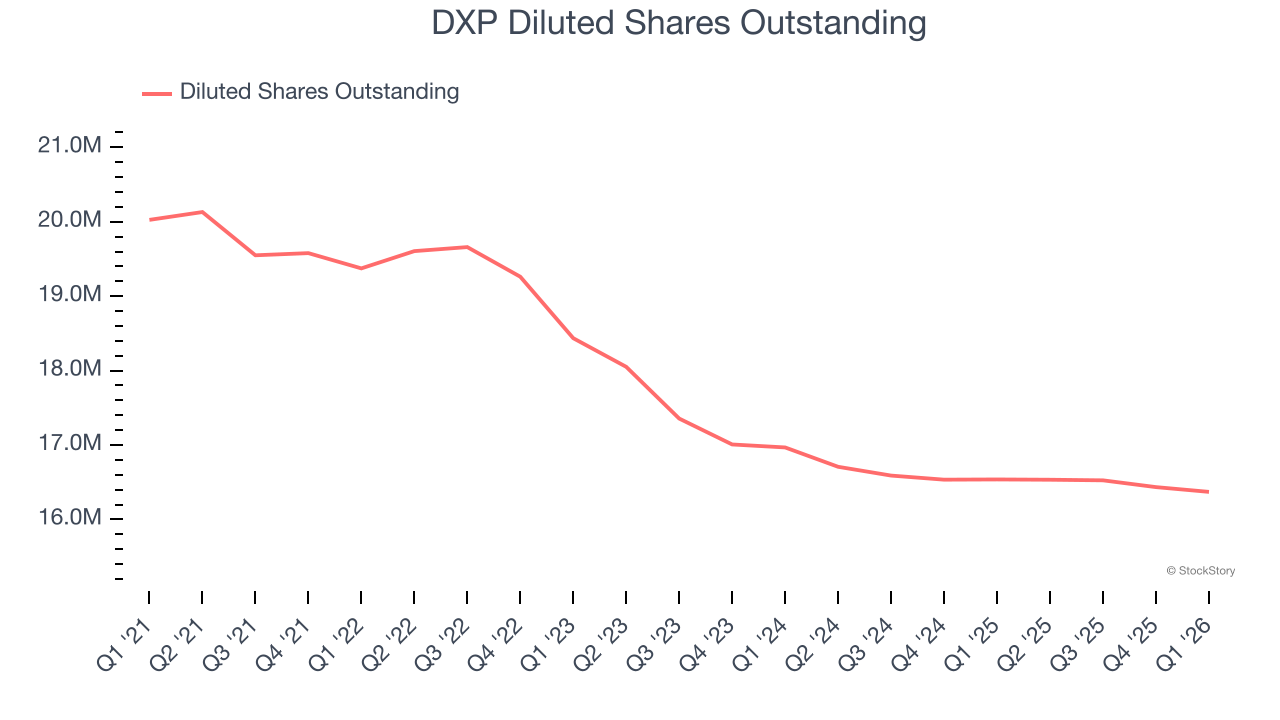

We can take a deeper look into DXP’s earnings to better understand the drivers of its performance. As we mentioned earlier, DXP’s operating margin was flat this quarter but expanded by 4.1 percentage points over the last five years. On top of that, its share count shrank by 18.3%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For DXP, its two-year annual EPS growth of 18.3% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, DXP reported adjusted EPS of $1.26, in line with the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects DXP’s full-year EPS of $5.42 to grow 20.1%.

Key Takeaways from DXP’s Q1 Results

We struggled to find many positives in these results. Its adjusted operating income missed and its revenue fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.5% to $167.32 immediately following the results.

DXP’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).