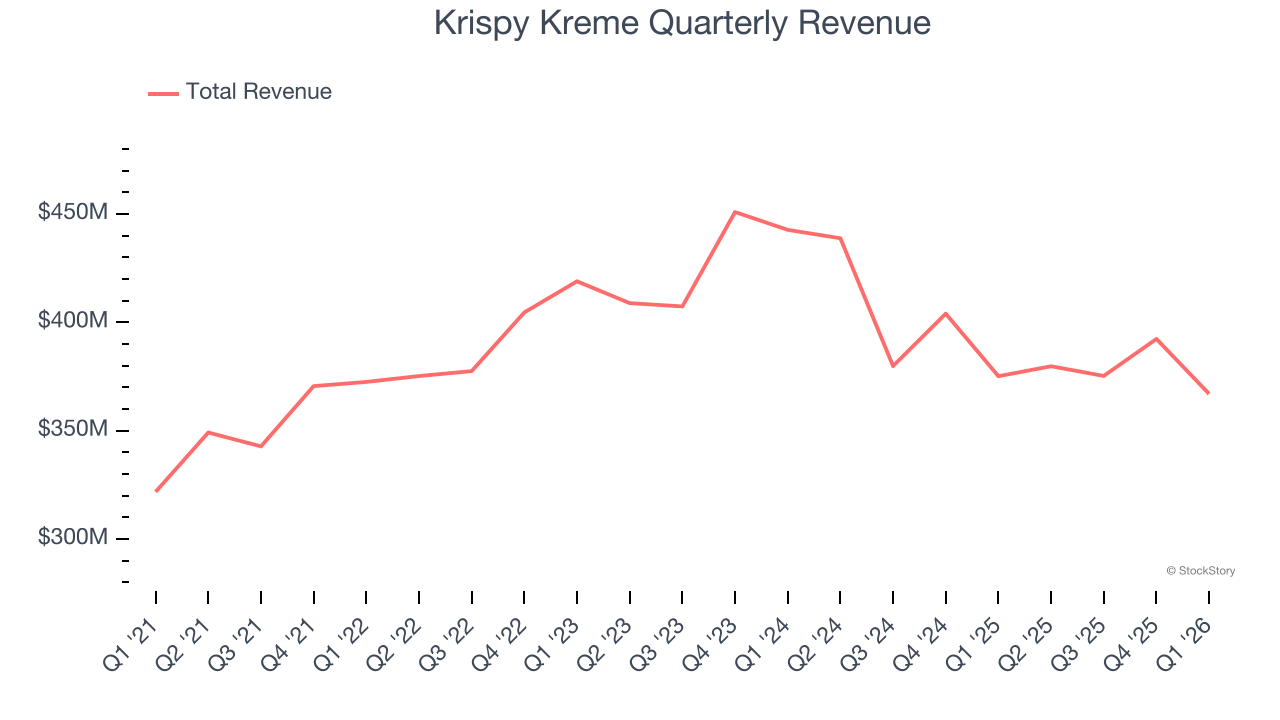

Doughnut chain Krispy Kreme (NASDAQ: DNUT) reported Q1 CY2026 results beating Wall Street’s revenue expectations, but sales fell by 2.2% year on year to $367 million. Its non-GAAP loss of $0.05 per share was $0.03 below analysts’ consensus estimates.

Is now the time to buy Krispy Kreme? Find out by accessing our full research report, it’s free.

Krispy Kreme (DNUT) Q1 CY2026 Highlights:

- Revenue: $367 million vs analyst estimates of $365 million (2.2% year-on-year decline, 0.5% beat)

- Adjusted EPS: -$0.05 vs analyst estimates of -$0.02 ($0.03 miss)

- Adjusted EBITDA: $33.1 million vs analyst estimates of $28.96 million (9% margin, 14.3% beat)

- Operating Margin: -1%, up from -5.4% in the same quarter last year

- Free Cash Flow was $11.38 million, up from -$46.73 million in the same quarter last year

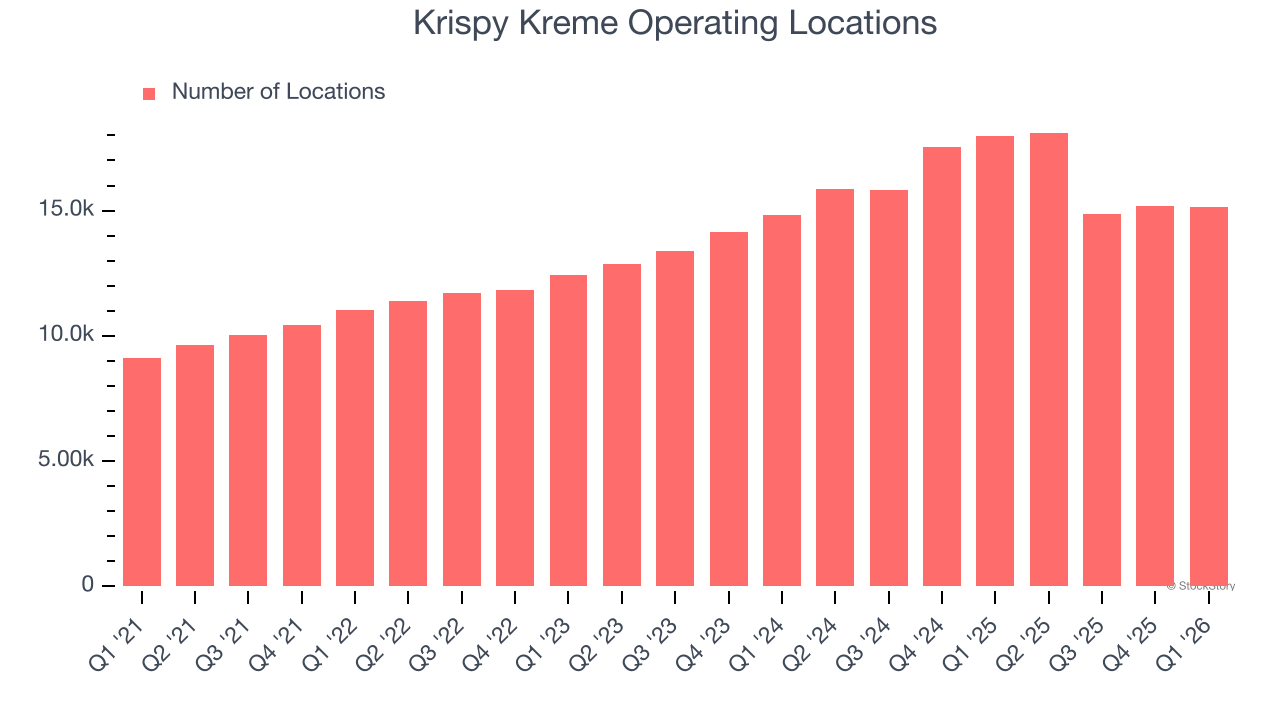

- Locations: 15,125 at quarter end, down from 17,982 in the same quarter last year

- Market Capitalization: $634.4 million

Company Overview

Famous for its Original Glazed doughnuts and parent company of Insomnia Cookies, Krispy Kreme (NASDAQ: DNUT) is one of the most beloved and well-known fast-food chains in the world.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.51 billion in revenue over the past 12 months, Krispy Kreme is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

As you can see below, Krispy Kreme grew its sales at a decent 7.3% compounded annual growth rate over the last six years as it opened new restaurants and expanded its reach.

This quarter, Krispy Kreme’s revenue fell by 2.2% year on year to $367 million but beat Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to decline by 6.4% over the next 12 months, a deceleration versus the last six years. This projection is underwhelming and indicates its menu offerings will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Number of Restaurants

Krispy Kreme operated 15,125 locations in the latest quarter. It has opened new restaurants at a rapid clip over the last two years, averaging 8.2% annual growth, much faster than the broader restaurant sector. This gives it a chance to become a large, scaled business over time.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Key Takeaways from Krispy Kreme’s Q1 Results

We were impressed by how significantly Krispy Kreme blew past analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS was in line. Zooming out, we think this was a mixed quarter. The stock traded up 2.1% to $3.83 immediately following the results.

Is Krispy Kreme an attractive investment opportunity right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).