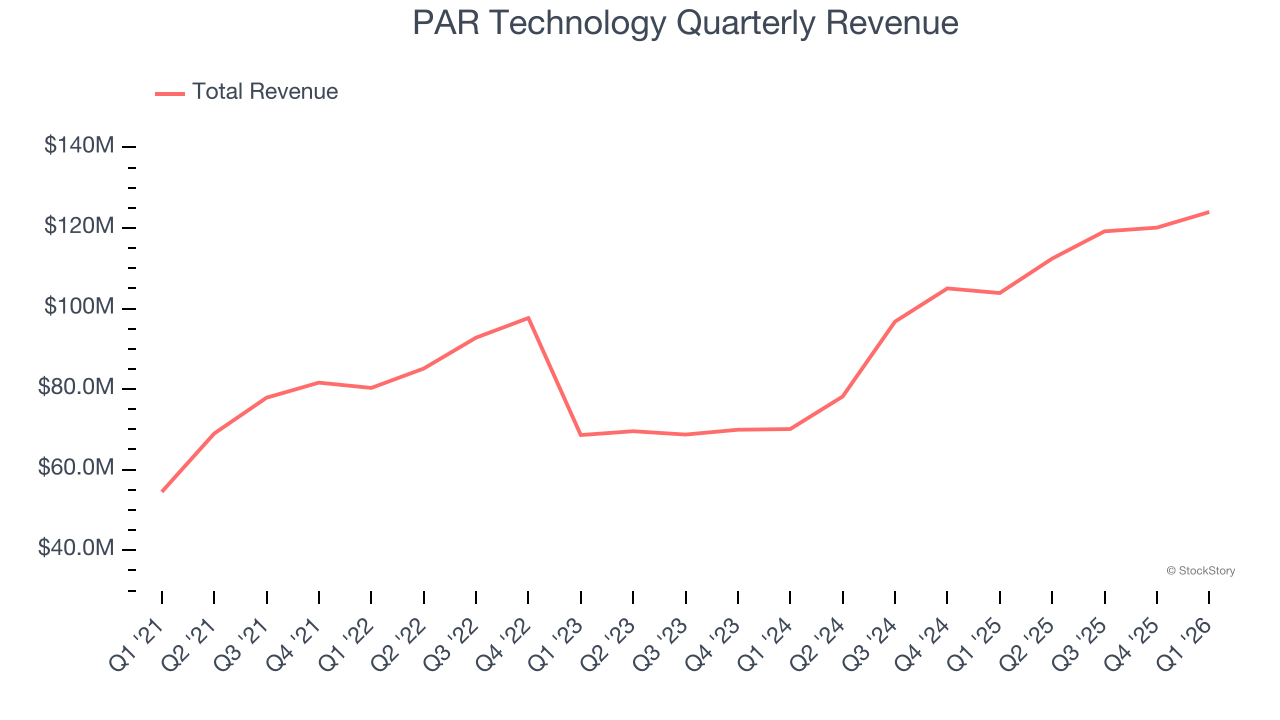

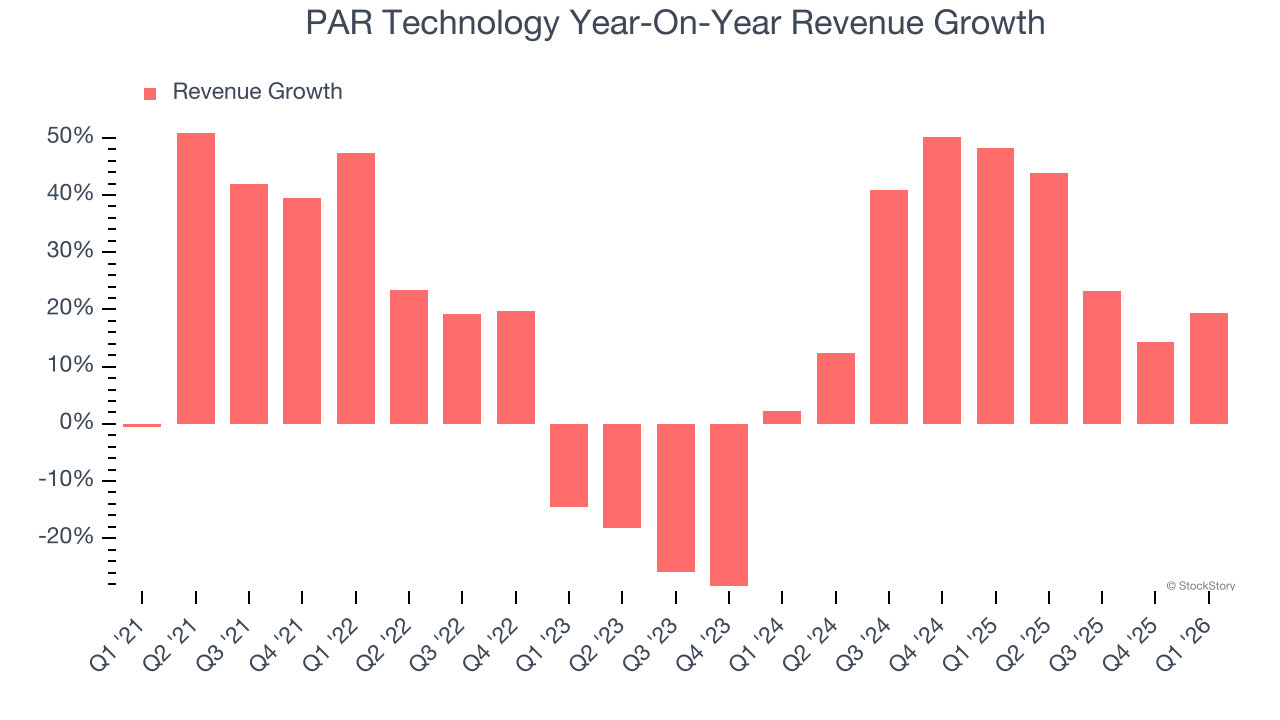

Restaurant technology provider PAR Technology (NYSE: PAR) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 19.4% year on year to $124 million. On top of that, next quarter’s revenue guidance ($125 million at the midpoint) was surprisingly good and 3.9% above what analysts were expecting. Its non-GAAP profit of $0.10 per share was 66.7% above analysts’ consensus estimates.

Is now the time to buy PAR Technology? Find out by accessing our full research report, it’s free.

PAR Technology (PAR) Q1 CY2026 Highlights:

- Revenue: $124 million vs analyst estimates of $116.6 million (19.4% year-on-year growth, 6.3% beat)

- Adjusted EPS: $0.10 vs analyst estimates of $0.06 (66.7% beat)

- Adjusted EBITDA: $8.95 million vs analyst estimates of $6.87 million (7.2% margin, 30.2% beat)

- Revenue Guidance for the full year is $507.5 million at the midpoint, above analyst estimates of $493.8 million

- EBITDA guidance for the full year is $45.5 million at the midpoint, above analyst estimates of $39.6 million

- Operating Margin: -11.2%, up from -15.2% in the same quarter last year

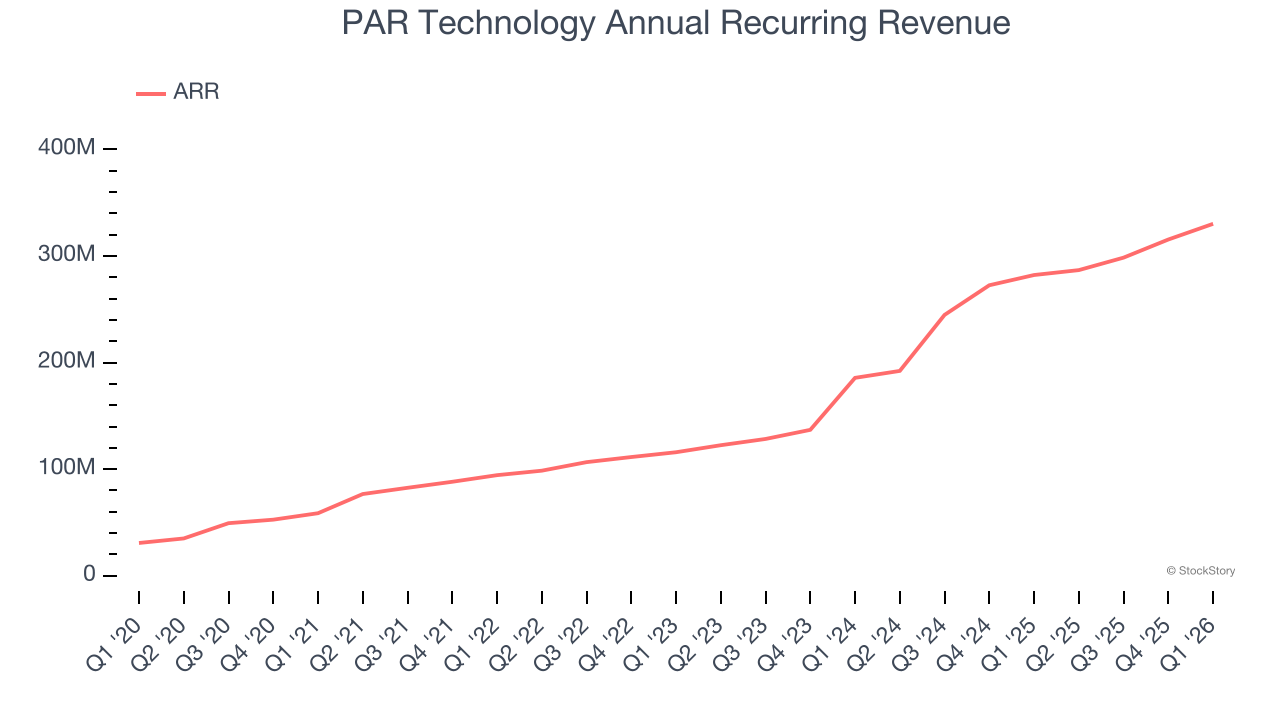

- Annual Recurring Revenue: $330.1 million (17% year-on-year growth, beat)

- Market Capitalization: $571.3 million

“We delivered a strong start to 2026, with 19% year-over-year revenue growth and adjusted EBITDA doubling to $9 million, demonstrating increasing operating leverage as the platform scales,” said Savneet Singh, Chief Executive Officer of PAR Technology.

Company Overview

Originally founded in 1968 as a defense contractor for the U.S. government, PAR Technology (NYSE: PAR) provides cloud-based software, payment processing, and hardware solutions that help restaurants manage everything from point-of-sale to customer loyalty programs.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $475.7 million in revenue over the past 12 months, PAR Technology is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, PAR Technology’s 17.4% annualized revenue growth over the last five years was incredible. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. PAR Technology’s annualized revenue growth of 30.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s sales dynamics by analyzing its annual recurring revenue (ARR), or the predictable, normalized yearly income from subscriptions and contracts. PAR Technology’s ARR reached $330.1 million in the latest quarter and averaged 50.3% year-on-year growth over the last two years. Because this number is better than its normal revenue growth, we can see the company’s proportion of recurring revenue from long-term contracts and subscriptions has increased. This implies more stability in its business model and revenue streams.

This quarter, PAR Technology reported year-on-year revenue growth of 19.4%, and its $124 million of revenue exceeded Wall Street’s estimates by 6.3%. Company management is currently guiding for a 11.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is commendable and indicates the market sees success for its products and services.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

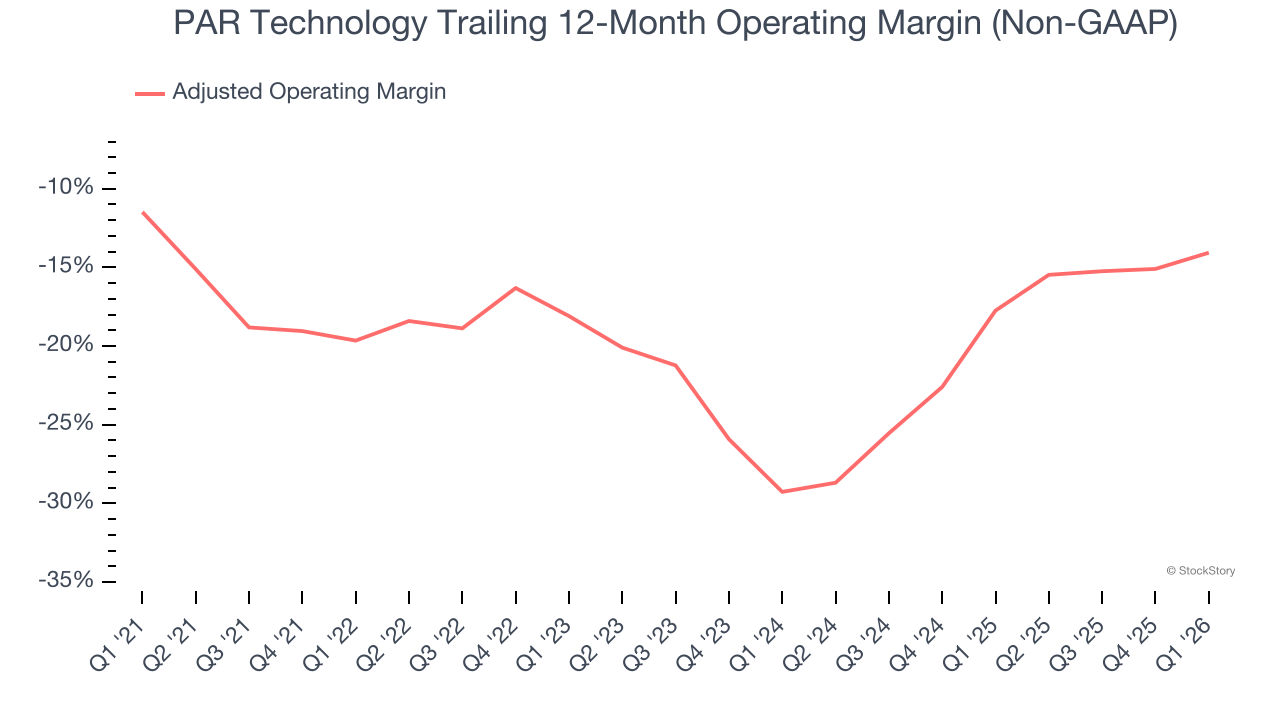

Adjusted Operating Margin

PAR Technology’s high expenses have contributed to an average adjusted operating margin of negative 19% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, PAR Technology’s adjusted operating margin rose by 5.6 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

PAR Technology’s adjusted operating margin was negative 11.2% this quarter.

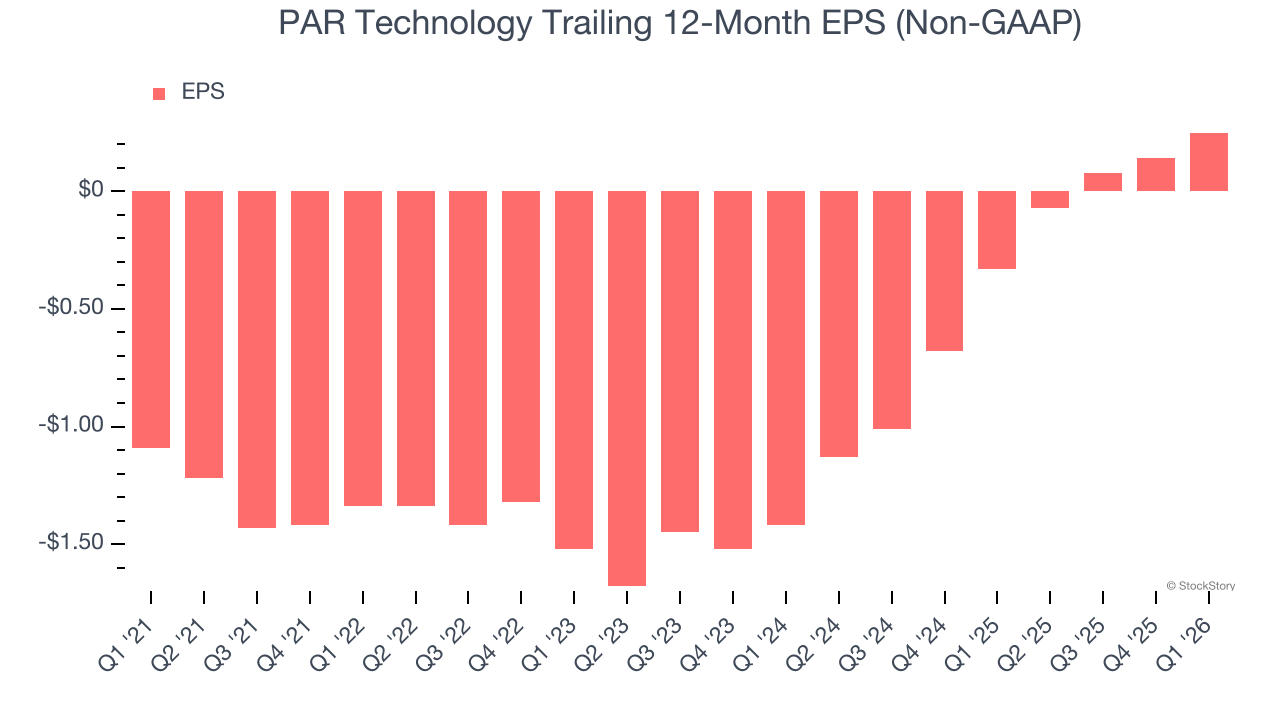

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

PAR Technology’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For PAR Technology, its two-year annual EPS growth of 47.5% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, PAR Technology reported adjusted EPS of $0.10, up from negative $0.01 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects PAR Technology’s full-year EPS of $0.25 to grow 158%.

Key Takeaways from PAR Technology’s Q1 Results

We were impressed by how significantly PAR Technology blew past analysts’ ARR expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.9% to $15.87 immediately after reporting.

PAR Technology may have had a good quarter, but does that mean you should invest right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).