Rumble has been treading water for the past six months, recording a small return of 4.9% while holding steady at $7.55. The stock also fell short of the S&P 500’s 10.7% gain during that period.

Is there a buying opportunity in Rumble, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Rumble Not Exciting?

We’re swiping left on Rumble for now. Here are three reasons we avoid RUM, plus one stock we’d rather own.

1. Fewer Distribution Channels Limit Its Ceiling

With $102.4 million in revenue over the past 12 months, Rumble is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

2. Cash Burn Ignites Concerns

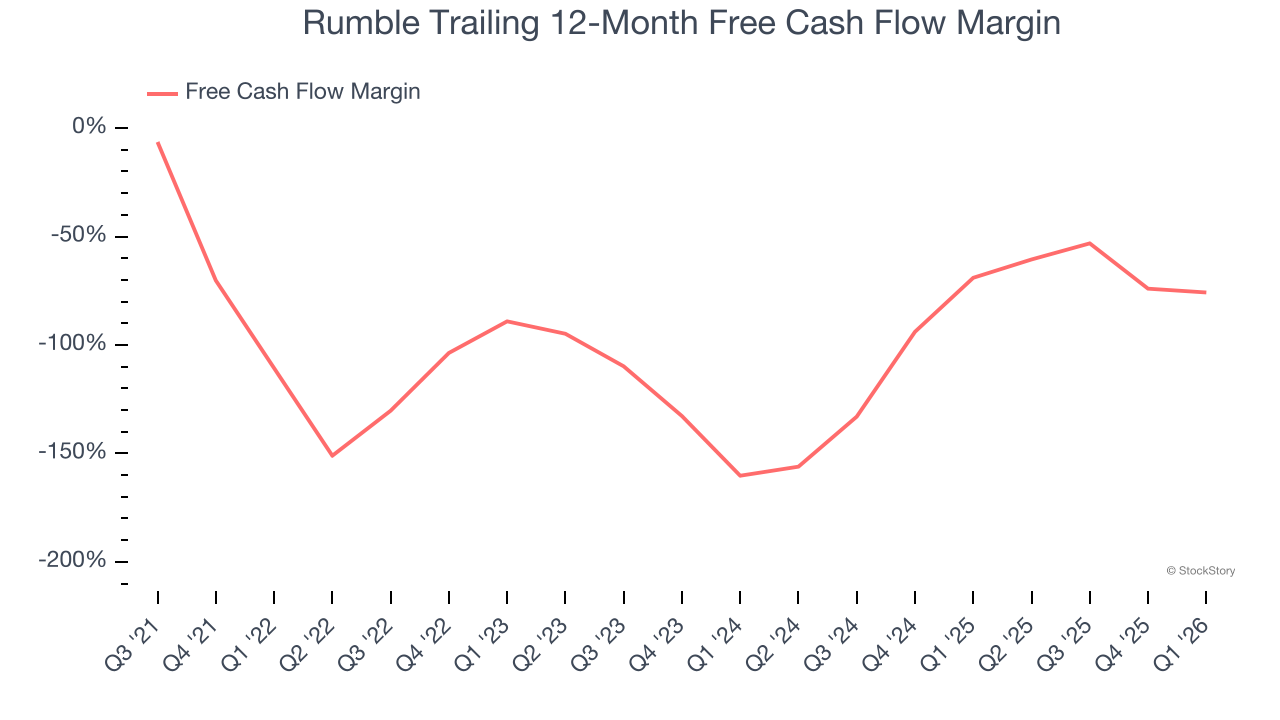

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Rumble’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 96.6%, meaning it lit $96.58 of cash on fire for every $100 in revenue.

3. Restricted Access to Capital Increases Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

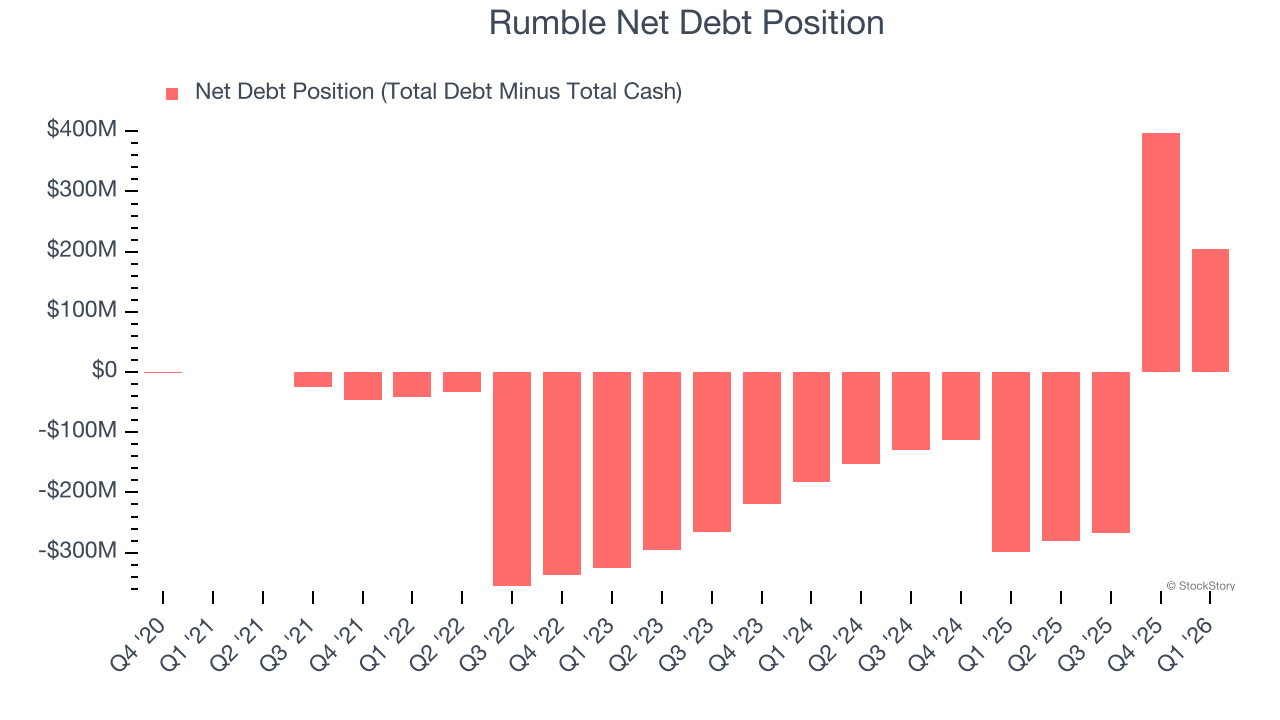

Rumble posted negative $72.57 million of EBITDA over the last 12 months, and its $423.5 million of debt exceeds the $219 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Rumble if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Rumble can improve its profitability and remain cautious until then.

Final Judgment

Rumble’s business quality ultimately falls short of our standards. With its shares underperforming the market lately, the stock trades at $7.55 per share (or a trailing 12-month price-to-sales ratio of 20.9×). The market typically values companies like Rumble based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Like More Than Rumble

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.