Food distribution company United Natural Foods (NYSE: UNFI) will be reporting results this Tuesday morning. Here’s what you need to know.

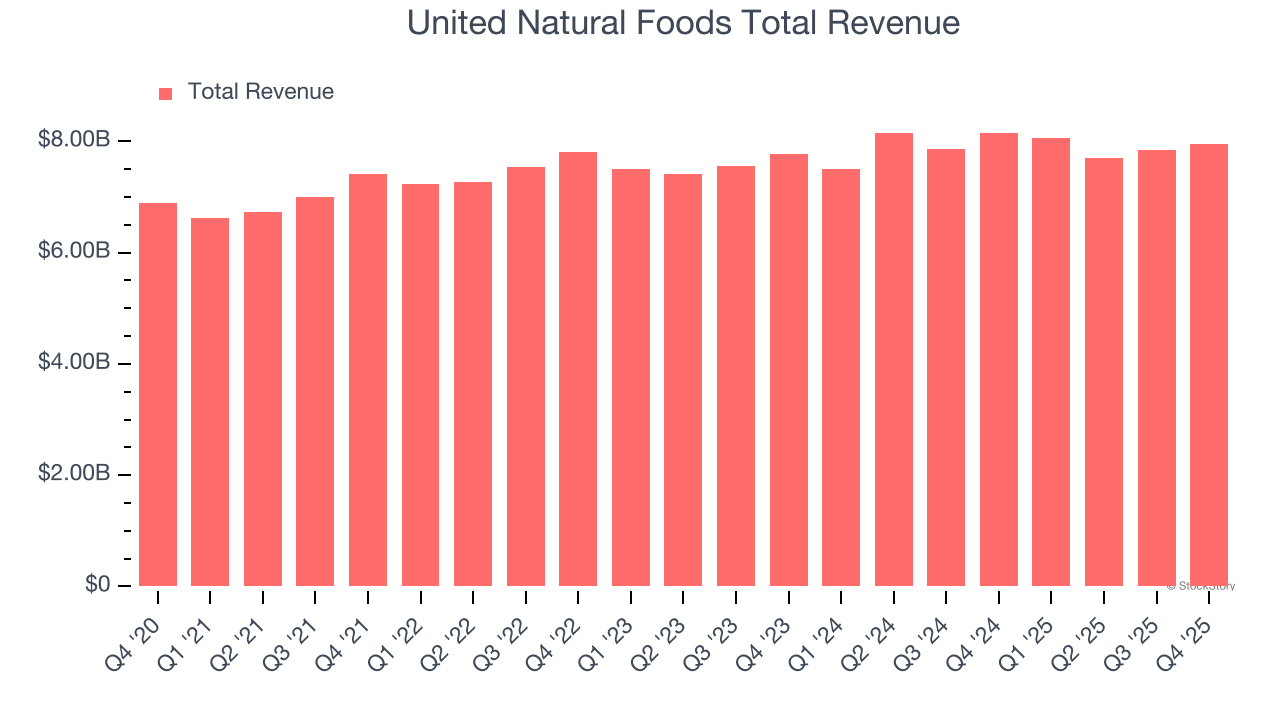

United Natural Foods missed analysts’ revenue expectations last quarter, reporting revenues of $7.95 billion, down 2.6% year on year. It was a satisfactory quarter for the company, with a solid beat of analysts’ EBITDA estimates but full-year revenue guidance missing analysts’ expectations.

Is United Natural Foods a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members.

This quarter, the market is expecting United Natural Foods’s revenue to decline 3.3% year on year, a reversal from the 7.5% increase it recorded in the same quarter last year.

The majority of analysts covering the company have reconfirmed their estimates over the last 30 days, suggesting they anticipate the business will stay the course heading into earnings. United Natural Foods has missed Wall Street’s revenue estimates multiple times over the last two years.

Looking at United Natural Foods’s peers in the perishable food segment, some have already reported their Q1 results, giving us a hint as to what we can expect. Freshpet delivered year-on-year revenue growth of 13.1%, beating analysts’ expectations by 2.2%, and Tyson Foods reported revenues up 4.4%, topping estimates by 1%. Freshpet traded down 7.1% following the results while Tyson Foods was up 7.5%.

Read our full analysis of Freshpet’s results here and Tyson Foods’s results here.

AI disruption fears rattled software and crypto through late 2025, but in spring 2026 the focus shifted to geopolitical risk, oil supply, and global stability. While some of the perishable food stocks have shown solid performance in this choppy environment, the group has generally underperformed, with share prices down 2.1% on average over the last month. United Natural Foods is up 4.5% during the same time and is heading into earnings with an average analyst price target of $46.25 (compared to the current share price of $54.61).

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.