Valued at a market cap of $32 billion, Fair Isaac Corporation (FICO) provides analytics software solutions. The Bozeman, Montana-based company is best known for creating the widely used FICO Score, a standard measure of consumer credit risk used by lenders globally.

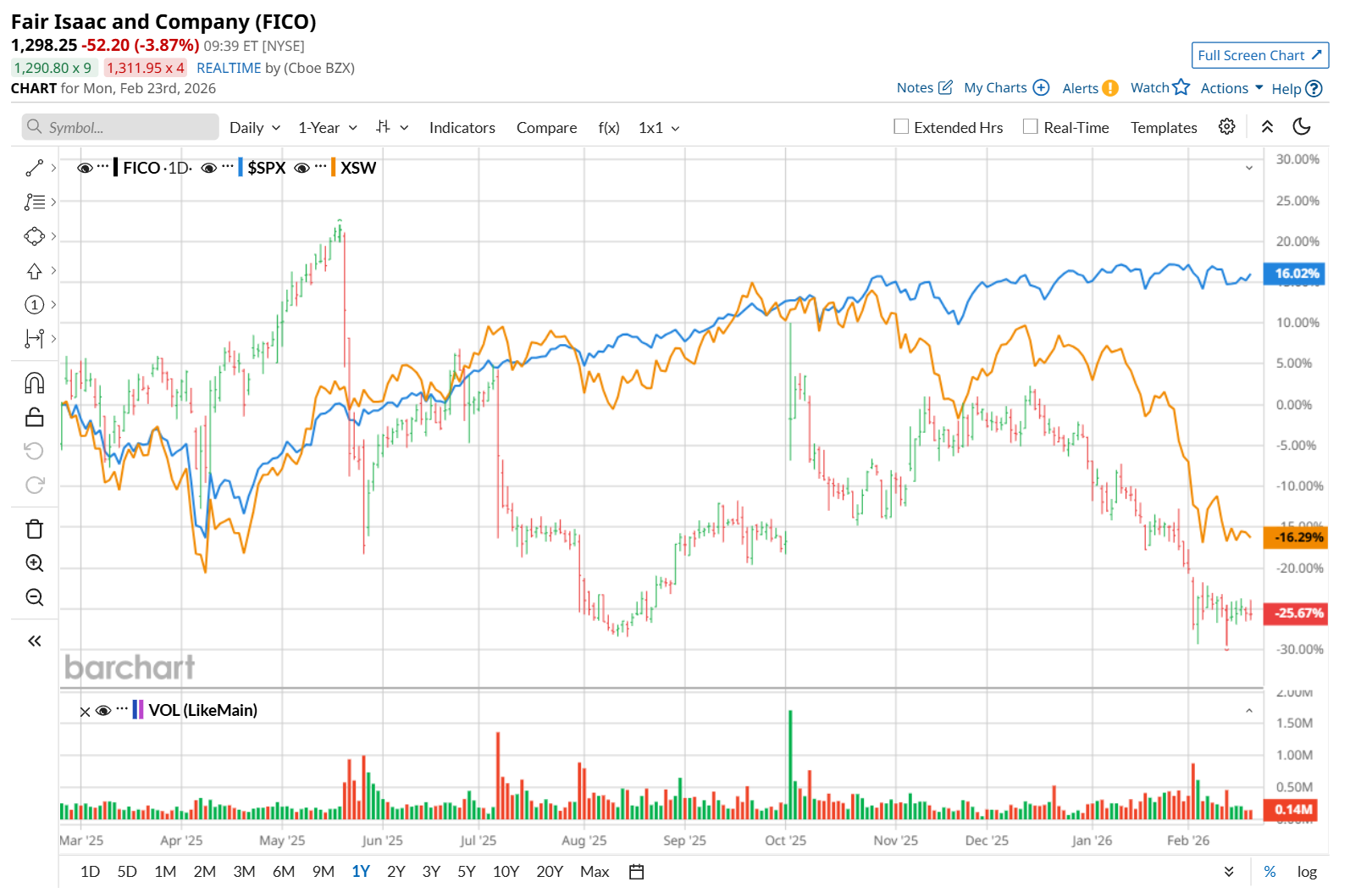

This tech company has considerably trailed the broader market over the past 52 weeks. Shares of FICO have declined 21.3% over this time frame, while the broader S&P 500 Index ($SPX) has gained 13%. Moreover, on a YTD basis, the stock is down 20.9%, compared to SPX’s marginal rise.

Zooming in further, FICO has slightly outpaced the State Street SPDR S&P Software & Services ETF (XSW), which decreased 21.5% over the past 52 weeks. However, FICO has underperformed XSW’s 20.2% YTD drop.

On Jan. 28, FICO delivered stronger-than-expected Q1 results, yet its shares plunged 1.6% in the following trading session. Due to higher on-premises and SaaS software revenue and a rise in Scores revenue, the company’s total revenue increased 16.4% year-over-year to $512 million, surpassing consensus estimates by 2.8%. Moreover, its adjusted EPS of $7.33 grew 26.6% from the year-ago quarter, topping analyst expectations of $6.95.

For the current fiscal year, ending in September, analysts expect FICO’s EPS to grow 44.8% year over year to $36.30. The company’s earnings surprise history is mixed. It topped the consensus estimates in three of the last four quarters, while missing on another occasion.

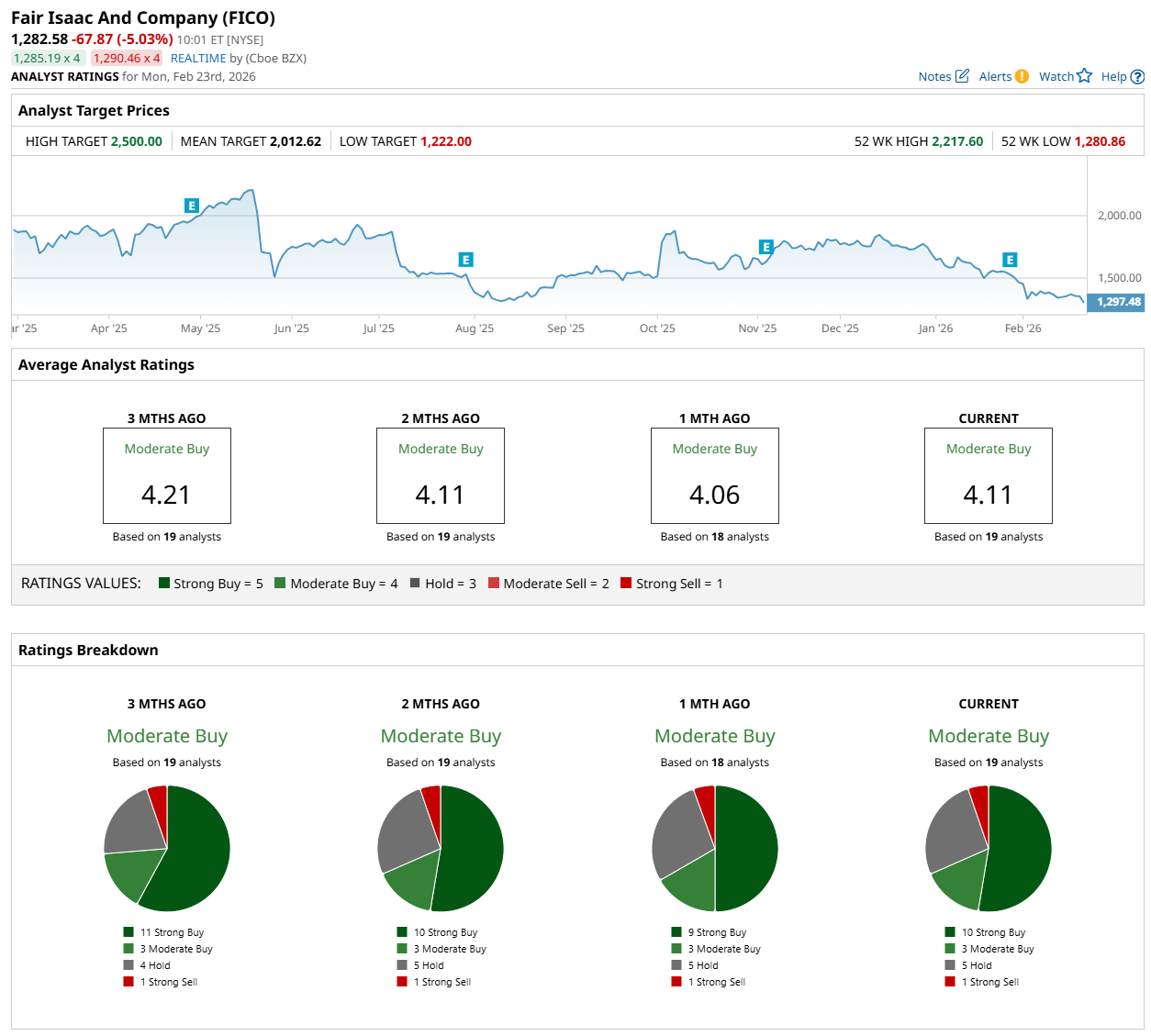

Among the 19 analysts covering the stock, the consensus rating is a "Moderate Buy,” which is based on 10 “Strong Buy,” three "Moderate Buy,” five "Hold,” and one "Strong Sell” rating.

The configuration is more bullish than a month ago, with nine analysts suggesting a “Strong Buy” rating.

On Feb. 17, Bank of America Corporation (BAC) reinstated coverage of FICO with a “Buy” rating and $1,900 price target, indicating a 48.1% potential upside from the current levels.

The mean price target of $2,012.62 suggests a 56.9% potential upside from the current levels, while its Street-high price target of $2,500 suggests a 94.9% potential upside from the current levels.

On the date of publication, Neharika Jain did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Why Citi Analysts Think You Should Buy Microsoft Stock Now

- Domino's Pizza Hikes Its Dividend By 14.3% After Free Cash Flow Rises 29% - Value Buyers Love DPZ Stock

- Up 265% in the Past 5 Days, Is There Any More Upside Left for Rackspace Stock?

- CoreWeave’s Q4 Results Due Feb. 26: What It Means for CRWV Stock