On Wall Street, when a company buys shares in another, it is rarely a random act of portfolio diversification. It can signal alignment, future partnerships, or simply confidence about where an industry is headed. That is why investors review 13F disclosures — mandatory quarterly filings with the U.S. Securities and Exchange Commission (SEC) for institutions managing more than $100 million. These filings disclose holdings, position sizes, market values, and portfolio weightings, offering rare insight into how sophisticated investors are positioning for the future, even if the data comes with a slight delay.

Against the backdrop of the artificial intelligence (AI) boom, chip heavyweight Nvidia (NVDA) is not only selling the chips that power AI — it is also strategically investing across the broader technology sector. Nvidia's latest 13F filing shows positions in rival chipmaker Intel (INTC), chip design software leader Synopsys (SNPS), AI cloud infrastructure provider CoreWeave (CRWV), and Finnish telecom operator Nokia (NOK) .

Some of these stakes reinforce existing partnerships, while others hint at deeper ecosystem ties. Either way, when Jensen Huang’s Nvidia puts capital to work, the market pays attention — and perhaps so should investors.

Stock to Buy #1: Intel (INTC)

Based in Santa Clara, California, Intel is one of the most recognized names in the semiconductor industry, with a market capitalization of about $217.9 billion. The company designs and manufactures chips that power personal computers, data centers and, increasingly, AI systems. From central processing units (CPUs) to graphics chips and system-on-chip solutions, Intel has long played a central role in advancing computing technology. With decades of innovation behind it, the company continues to shape the infrastructure that supports the modern digital economy.

Nvidia has built a significant position in Intel, investing roughly $7.9 billion and holding 214.77 million shares, making it one of Intel’s largest shareholders. The move was deliberate. Intel has been working to rebuild its competitive edge for the AI era, and Nvidia’s capital signals confidence in that turnaround.

The investment did not come out of nowhere. Back in September, Nvidia announced a $5 billion commitment to Intel as part of a broader AI collaboration, which was completed in December. The partnership centers on Intel manufacturing custom x86 CPUs for Nvidia’s AI platforms and developing system-on-chips that integrate Nvidia RTX GPU chiplets. The goal is strategic alignment, combining Nvidia’s AI leadership with Intel’s manufacturing scale while diversifying Nvidia’s supply chain.

For Intel, the fresh capital arrives at a critical moment. After leadership turnover and steep losses in 2024, the company needed stability and validation. That support began with the U.S. government taking a 10% stake under the CHIPS Act to strengthen domestic semiconductor manufacturing, and it gained momentum when Nvidia started building its position last year.

Since then, momentum has shifted. INTC stock has climbed 89% over the past 52 weeks, rebounding from a low of $17.67 to a high of $54.60 in January, with shares steadily rising. While the stock carried that momentum into early 2026, the rally hit turbulence after Intel issued softer-than-expected guidance in its latest earnings report, triggering a pullback and reminding investors that the turnaround story is still in motion.

The chipmaker delivered a better-than-expected fourth-quarter earnings report, generating revenue of $13.7 billion, topping both Wall Street’s estimates and management’s own guidance. Growth was broad-based, with AI-enabled PCs, traditional servers, and networking products all posting double-digit gains sequentially and year-over-year (YOY). Adjusted EPS of $0.15 comfortably beat the outlook, helped by better gross margins and tighter cost control. After a volatile stretch, it was a quarter that showed real operational traction.

But the tone shifts as Intel looks ahead. To meet heavy demand in late 2025, the company leaned on existing inventory and intra-quarter wafer production. That cushion is now largely gone. With production shifting toward server chips, supply constraints are expected to pinch in the first quarter. Management guided for Q1 revenue of $12.2 billion and forecast breakeven profitability, softer than investors hoped.

Still, the longer view looks firmer. Management expects supply to ease starting in Q2, while AI-driven demand in data centers and PCs accelerates. With its x86 franchise and expanding AI portfolio, Intel appears positioned to regain momentum as 2026 unfolds.

Analysts tracking the company anticipate Q1 revenue to be around $12.3 billion, with losses widening. Looking further out, however, the earnings trajectory is projected to improve. EPS for the full year is expected to rise 158% YOY to $0.07 before surging by a whopping 671% annually to $0.54 in fiscal 2027.

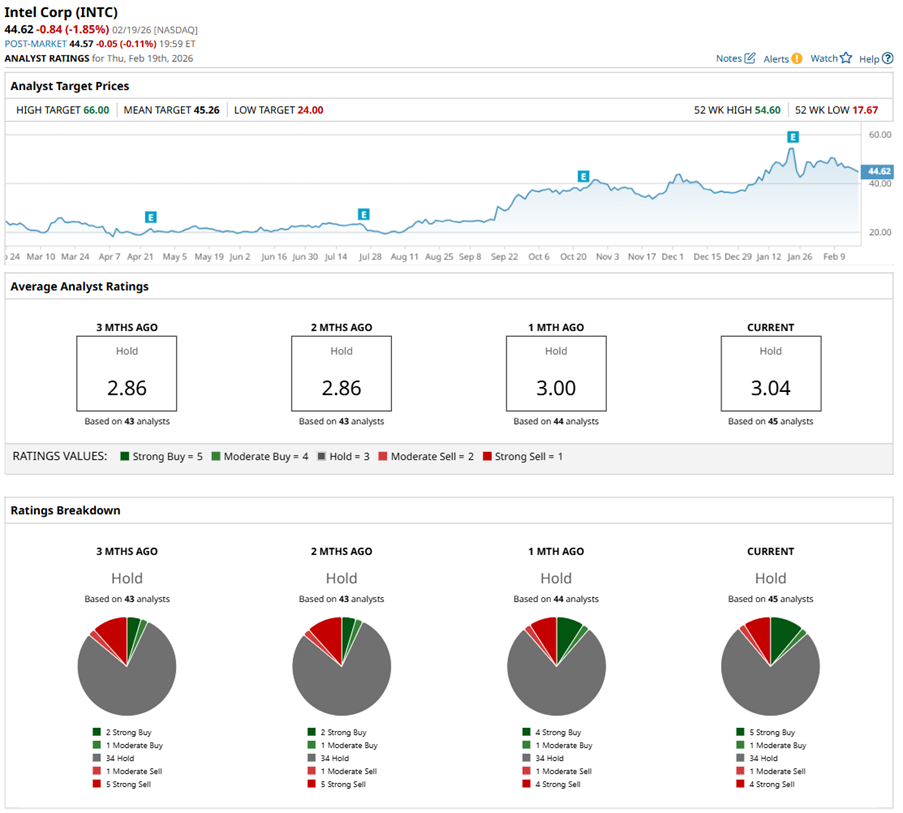

Wall Street seems cautiously open to Intel’s comeback, though not fully convinced, with an overall “Hold" rating. Of the 45 analysts covering INTC stock, five suggest a “Strong Buy,” one has a “Moderate Buy” rating, 34 recommend a “Hold,” one analyst has a “Moderate Sell,” and four advise a “Strong Sell" rating.

As of this writing, INTC stock is currently trading near its average price target of $45.26. Still, the most bullish target on the Street stands at $66, implying potential upside of 44% over the next year if the turnaround gains traction.

Stock to Buy #2: Synopsys (SNPS)

Incorporated in 1986 and headquartered in Sunnyvale, California, Synopsys develops the critical software and design IP that power modern semiconductor innovation. With a market capitalization of roughly $80.6 billion, the company sits at the heart of the chip design ecosystem. As AI workloads and hyperscale data centers expand, chipmakers increasingly rely on Synopsys’ tools to deliver precision, performance, and speed to market.

Nvidia partnered with Synopsys last year and also put real capital behind the relationship. The companies entered a multiyear collaboration aimed at extending Nvidia’s Compute Unified Device Architecture (CUDA) platform deeper into chip design and engineering workflows.

The scope goes well beyond software tools. It spans agentic AI, physical AI, and Omniverse-powered digital twins, with the goal of helping R&D teams design and verify increasingly intelligent products faster and more efficiently. By embedding Nvidia’s accelerated computing into Synopsys’ EDA stack, both companies expand their reach across industries hungry for AI-enabled innovation.

Nvidia reinforced that commitment by acquiring 4.82 million Synopsys shares, a stake valued at about $2.26 billion. Nvidia continues to hold the position.

It has not been an easy stretch for Synopsys. SNPS stock has failed to reclaim its July high of $651.73 and now trades roughly 32% below that level, as investors weigh uncertainty around its IP business transition and softer demand tied to China. Over the past 52 weeks, shares are still down about 7%.

That said, momentum has quietly improved. SNPS stock has climbed 8.5% in the last three months and added another 4% in just the past five days, hinting at stabilizing sentiment.

On Dec. 10, Synopsys reported its fiscal Q4 numbers, which edged past the Street’s estimates. Revenue grew 38% YOY to $2.25 billion. Growth was fueled largely by strength in its Time-Based Product and Upfront Product segments, reflecting steady demand for advanced design tools. Profitability, however, told a more mixed story. Non-GAAP EPS slipped 15% to $2.90, slightly beating projections.

Synopsys ended Q4 with $2.96 billion in cash, cash equivalents and short-term investments, up from the prior quarter. Total long-term debt stood at $13.46 billion.

Looking ahead, management is guiding for fiscal 2026 revenue between $9.56 billion and $9.66 billion, including an expected $2.9 billion contribution from Ansys, as integration efforts move forward. Non-GAAP EPS is projected in the range of $14.32 to $14.40, signaling confidence in operational efficiencies.

The company is all set to release its first-quarter fiscal 2026 earnings report on Feb. 25, after the market closes. Management expects revenue between $2.365 billion and $2.415 billion, while non-GAAP EPS is anticipated to be between $3.52 and $3.58.

Analysts tracking Synopsys expect first-quarter EPS of about $2.43, marking an 8% YOY increase, with revenue coming in near $2.39 billion. Looking ahead, the bottom line is projected to rise by 17% YOY to $10.11 per share in fiscal 2026, then rise another 19% annually to $12.07 per share in fiscal 2027.

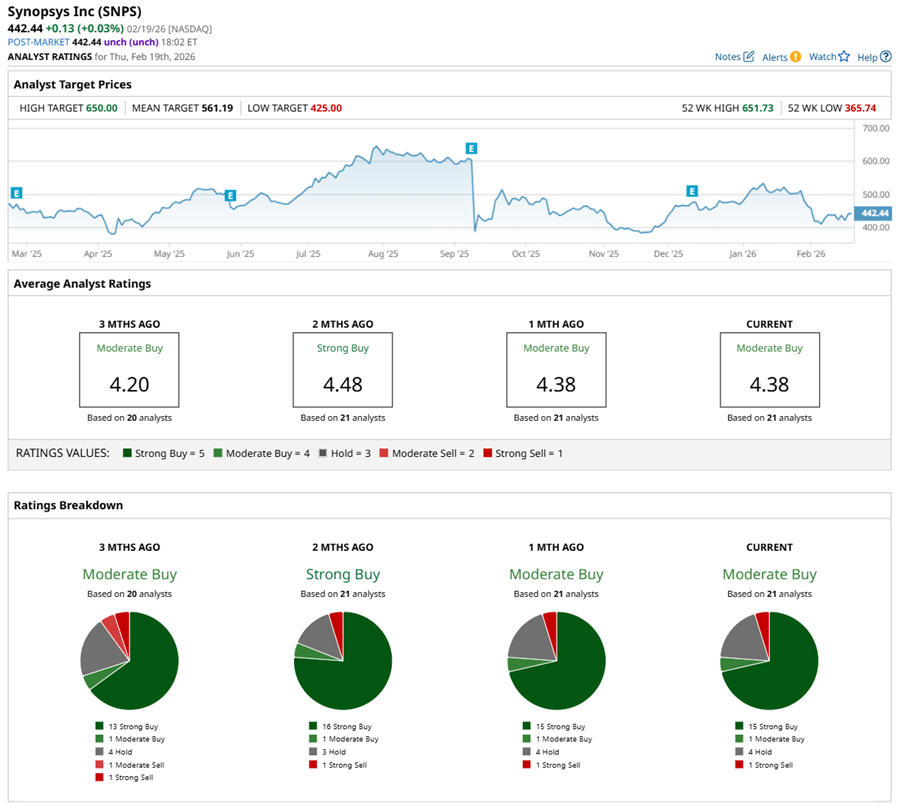

Wall Street’s confidence in SNPS is evident, as the stock has a “Moderate Buy” rating overall. Among the 21 analysts covering the stock, 15 are highly bullish with a “Strong Buy,” one advises a “Moderate Buy,” four have a “Hold,” and one has a “Strong Sell” rating.

The average analyst price target of $556.90 indicates potential upside of 26% from the current price levels. However, the Street-high target of $650 suggests that the stock could surge as much as 47%.

Stock to Buy #3: CoreWeave (CRWV)

Founded in 2017 and headquartered in Livingston, New Jersey, CoreWeave has quickly become a key player in GPU-optimized cloud infrastructure. With a market cap of about $35.1 billion, the company focuses on delivering high-performance computing systems built for generative AI and large-scale workloads. CoreWeave aims to simplify AI deployment for enterprises, helping businesses scale advanced computing efficiently in the evolving AI-driven economy.

Beyond chips, Nvidia is deepening its footprint in AI infrastructure through a major investment in CoreWeave. The GPU cloud provider, built largely on Nvidia hardware, secured a $2 billion investment that underscores a tight strategic alliance rather than a simple financial bet. Nvidia now owns 24.27 million shares valued at roughly $1.7 billion.

This is an active partnership. CoreWeave is deploying multiple generations of Nvidia technology across its AI cloud platform, including early access to the Vera CPU, Rubin GPUs, and BlueField systems. The two are collaborating on AI factories, validating AI-native software stacks, and accelerating data center buildouts. For Nvidia, it strengthens the distribution of its full-stack AI architecture. For CoreWeave, it ensures priority access to cutting-edge compute.

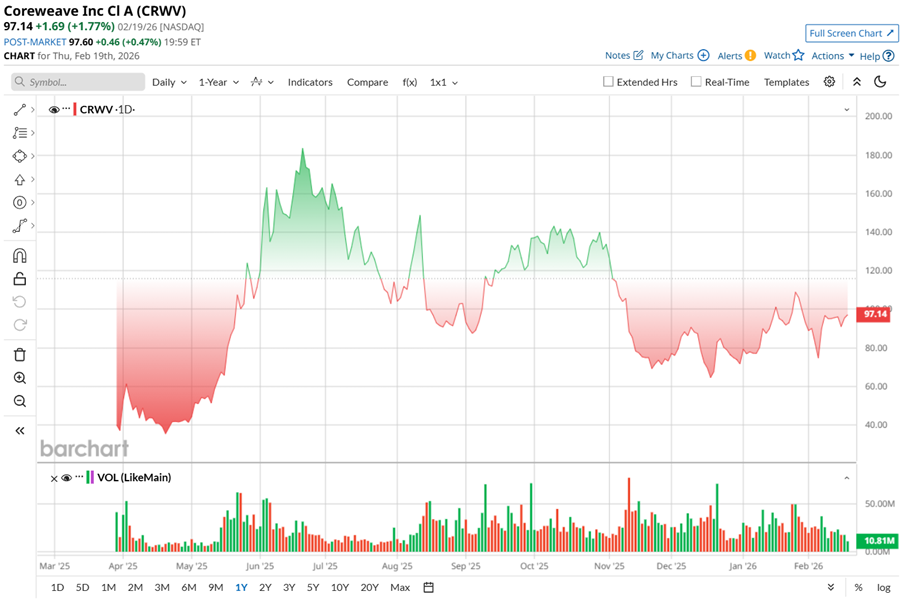

CRWV stock's price performance has mirrored the volatility of the AI trade. The stock debuted at $40 in March 2025 and quickly caught fire, rallying to $187 by June 20 as investors piled into AI cloud names tied to major partnerships, acquisitions, and expanding federal opportunities.

But volatility followed the surge. Shares have since pulled back roughly 50% from their peak and sit about 14% below their year-to-date (YTD) high of $114.45 reached on Jan. 28. Even with the sharp retracement, the stock remains up by around 34% in 2026, underscoring the strength of its earlier run.

Recent weakness has also been tied to legal uncertainty after Bleichmar Fonti & Auld LLP announced a class-action lawsuit alleging securities law violations following significant price declines. For investors, CRWV stock remains a high-beta AI name — capable of outsized gains, but equally exposed to swift sentiment shifts.

CoreWeave delivered a headline-grabbing Q3 earnings report in November with revenue soaring to a record $1.36 billion, up 134% YOY and comfortably ahead of expectations. The growth reflects unrelenting demand for high-performance GPU infrastructure as enterprises race to scale AI workloads. Losses narrowed sharply to $0.22 per share, an 88% improvement YOY, signaling improving operating leverage even as the company remains in investment mode.

Total backlog nearly doubled sequentially and surged 271% YOY to $55.6 billion, reinforcing long-term visibility. Adjusted operating income climbed 74% to $217.2 million, and the company ended the quarter with $3 billion in cash, indicating solid liquidity to fund expansion.

Management trimmed full-year revenue guidance, now expecting the top line to be between $5.05 billion and $5.15 billion due to project timing shifts tied to a third-party data center delay, though contract value remains intact. Capex is expected to range between $12 billion and $14 billion, with 2026 spending projected to rise meaningfully. While debt levels and interest costs warrant monitoring, CoreWeave’s expanding capacity, diversified backlog, and accelerating AI demand continue to anchor a constructive long-term outlook.

CoreWeave is all set to discuss Q4 and fiscal 2025 financial results on Feb. 26. Analysts tracking the company anticipate fiscal 2025 revenue to be around $5.1 billion, while losses are expected to continue, pegged at -$2.46 per share, widening by 100% YOY. The turnaround might start showing in fiscal 2026, when losses are expected to shrink by 97% annually.

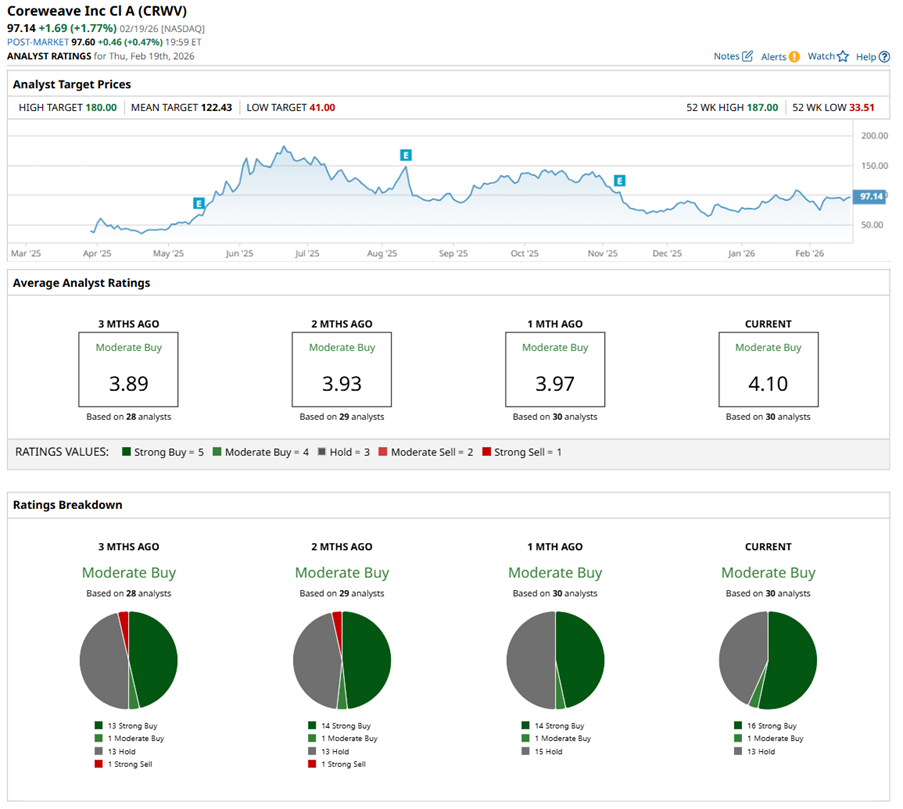

CRWV stock has an overall “Moderate Buy” rating, reflecting a generally positive analyst outlook. Among 30 analysts covering the stock now, 16 advise a “Strong Buy,” one suggests a “Moderate Buy,” and the remaining 13 analysts play it safe with a “Hold” rating.

Even with the stock slipping, analysts are optimistic. The average target of $122.43 signals 25% potential upside, while the Street-high target of $180 suggests that the stock could rise as much as 84% from here.

Stock to Buy #4: Nokia (NOK)

Originally founded in 1865 with roots in the paper industry, Nokia is now a global leader in network infrastructure, cloud services, and technology licensing. The Finland-based company designs and delivers mobile, fixed, and cloud-based network solutions, including 5G, optical transport, and IP routing systems used by telecom operators and enterprises worldwide.

Nokia also develops software for automation, cybersecurity, and network management, while monetizing one of the industry’s deepest patent portfolios. Nokia invests heavily in research and development, positioning itself at the forefront of AI-driven networks and early 6G innovation. With a market cap of over $43 billion, it remains a foundational player in global connectivity.

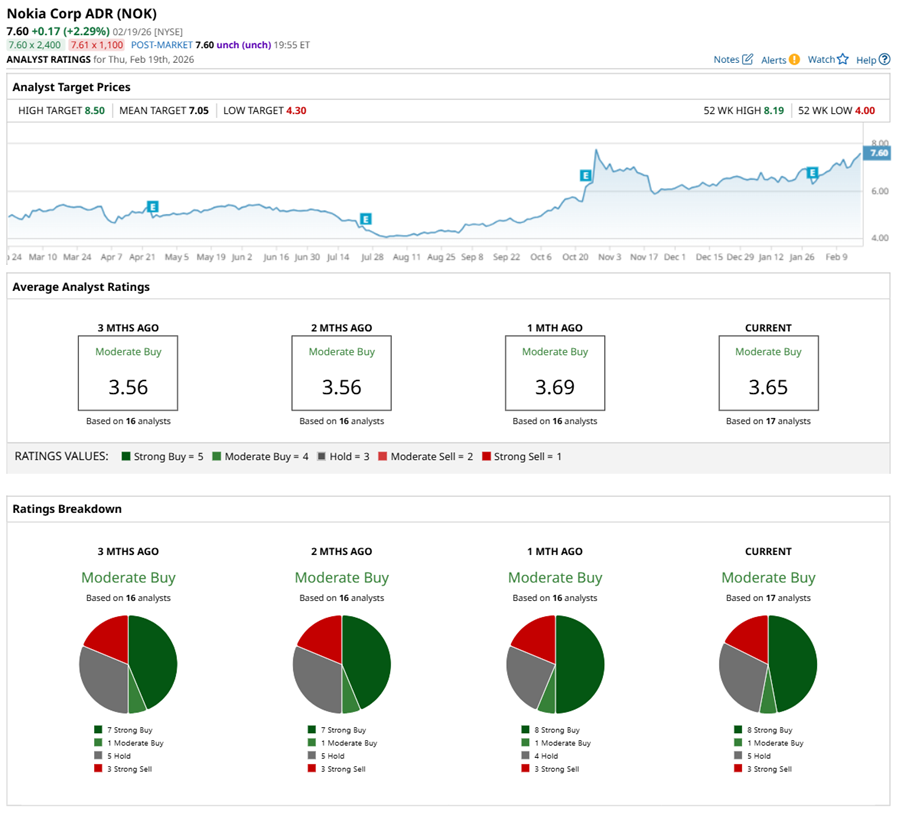

Nokia's strategic relevance deepened after Nvidia took a $1 billion equity stake, now holding 166.38 million shares.

Nokia has built steady momentum on Wall Street. Over the past 52 weeks, NOK stock has rallied roughly 53%, reflecting renewed investor confidence in telecom infrastructure and AI-driven networking demand. In just the last three months, shares have advanced 23%, signaling accelerating buying interest. The stock touched a 52-week high of $8.19 in October and continues to trade only modestly below that level, keeping its overall trend steady.

On Jan. 29, Nokia released its Q4 fiscal 2025 numbers, which came in ahead of expectations. Net sales reached €6.12 billion ($7.2 billion), marking a 2% YOY increase. The growth was largely driven by strength in the Network Infrastructure segment, particularly in optical networks, where revenue rose to €2.4 billion from €2.03 billion a year earlier.

Profitability, however, softened. Net income declined to €544 million, or €0.10 per share, compared with €813 million, or €0.15 per share, in the prior-year quarter, as higher operating expenses weighed on margins.

For the full year, operating cash flow totaled €2.07 billion, down from €2.49 billion in 2024. Nokia ended the year with €5.46 billion in cash and €2.32 billion in long-term interest-bearing liabilities, maintaining a solid balance-sheet position.

Looking ahead to 2026, management forecasts comparable operating profit between €2 billion and €2.5 billion. Free cash flow is projected at 55% to 75% of operating profit, with capital expenditures expected between €900 million and €1 billion. Network Infrastructure sales are anticipated to grow 6% to 8%.

Wall Street analysts have a bullish view about Nokia’s bottom-line trajectory. For fiscal 2026, EPS is expected to grow by 12% YOY to $0.37, followed by a 13.5% annual increase to $0.42 in fiscal 2027.

This steady growth profile is supporting a favorable tone around the stock. NOK has a consensus “Moderate Buy” rating overall. Of the 17 analysts rating the stock, eight have a “Strong Buy” rating, one analyst has a “Moderate Buy,” five analysts are playing it safe with a “Hold” rating, and three recommended a “Strong Sell.” NOK stock is currently trading above the consensus price target of $7.05. However, the Street-high price target of $8.50 indicates about 13% potential upside from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart