The American stock market ended the first quarter in a state of deep conceptual uncertainty. The attention of the majority of traders and financial media today is closely focused on the rhetoric of Federal Reserve officials and expectations for the notorious “pivot” or, conversely, the maintenance of a tight monetary policy.

The market is left guessing: Will the Fed change course in the coming months, or will the regulator remain a hostage to its own targets?

At the same time, for fundamental macroeconomic analysis, this speculation is secondary. Interest rates, the Fed’s balance sheet, and quantitative tightening (QT) programs are merely instruments of monetary management. They have meaning only in the context of how exactly they influence the actual quantity of money in the economy. The true mirror reflecting the real state of affairs is not the text of the FOMC minutes, but the Fed Net Liquidity.

Fed Net Liquidity cuts through the noise and shows the actual volume of “free money” that the U.S. financial system relies on.

Beginning in 2022-2023, the liquidity curve didn’t simply stop growing — it transitioned into a phase of stagnation with a slight, but clear, downtrend. The physical amount of money in the financial system is no longer growing.

For the broader market, this means one thing: the fuel that provided the broad-based growth of assets on all fronts is no longer entering the financial system. The key question for investors today is not what Fed Chair Jerome Powell will say at the next press conference, but where this specific curve will head next.

Fundamental vs. Transient Factors: Liquidity and the Oil Shock

Undoubtedly, macroeconomic analysis today is impossible without factoring in the geopolitical context. The situation in the Middle East, the tension around the Strait of Hormuz, and, as a consequence, oil (CLK26) entrenching itself at high levels — this is a powerful factor exerting colossal pressure on business expenses and inflationary expectations. To ignore the energy shock would be a mistake; the cost of a barrel directly translates into higher prices for logistics and production, forcing the Fed to remain cautious.

But here is a nuance: for all their destructive power, oil prices remain an event-driven, tactical factor. They dictate market tactics in the moment and hit the margins of specific sectors.

Liquidity, however, is the fundamental baseline. If the liquidity curve continues moving sideways (stagnating) or downwards, the American stock market’s capacity for organic, broad-based growth will remain highly questionable. Market math is inexorable: with a shrinking money supply, a stable bull trend is unlikely. A fundamental continuation of growth is possible under only one condition — if this curve starts creeping upwards again. What exactly drives this (a rate cut, or new mechanisms for managing the Treasury’s balance) is a technical question. The main thing is the actual shift in trend regarding the economy’s money supply.

The Paradox of Growth and the Base Effect: How Did the Market Grow Without New Money?

A logical question arises here: if liquidity has stagnated over the last several years, what fueled the indexes (particularly the S&P 500 ($SPX)) to set historical records, sending the tech sector’s capitalization into the stratosphere? The answer lies in a combination of two powerful structural factors that temporarily compensated for this macroeconomic “hunger.”

The first factor: The inertia of the expanded 2020 monetary base.

The unprecedented monetary and fiscal injections of 2020-2021 did not disappear without a trace. They created a colossal overhang of money supply, which radically expanded the economic base. U.S. nominal GDP surged from roughly $21 trillion pre-pandemic to $31 trillion today — a growth of approximately 50%. For several years, the market “digested” this historic volume of liquidity, pricing the new scale of the nominal economy into corporate profits. However, by now, this low-base effect appears to be fully priced in. The economy has absorbed this money, inflation has raised nominal values, and the old yeast has stopped making the dough rise.

The second factor: Investment “doping.”

The second, and much more important factor explaining the paradox of growth, is the artificial intelligence boom. It is crucial to understand that market growth in recent years has been extremely uneven. While many traditional sectors of the American economy were stuck in a weak, stagnating state due to high rates and expensive credit, the tech sector kicked off an unprecedented capital expenditure (CapEx) cycle. The largest corporations stopped hoarding super-profits or funneling them exclusively into the traditional banking system. Instead, they began aggressively reinvesting their own funds into AI infrastructure, data centers, and semiconductors.

From a macroeconomic perspective, this process acted as a localized “quantitative easing” (QE). Tech giants, spending hundreds of billions of dollars of their retained earnings, essentially provided an intra-sector capital injection, giving the market a massive innovation premium. This investment boom within a single industry created the illusion of general prosperity, masking the fact that the external influx of fresh capital into the broader market remained extremely limited.

Credit Hunger and the Macroeconomic Reality Check for AI

Any investment boom, even the most massive and technologically disruptive one, eventually collides with a harsh macroeconomic reality check: the solvency of end-user demand. The AI industry is currently building grandiose infrastructure, but the market is now asking a perfectly logical question: where is the large-scale monetization at the end-user and enterprise level outside of the tech sector itself?

For real-sector companies to massively adopt expensive AI solutions, upgrade equipment, and buy subscriptions, they need capital. And this is exactly where we hit the main brake of the current economic cycle — a deep gap between nominal GDP growth and the state of credit.

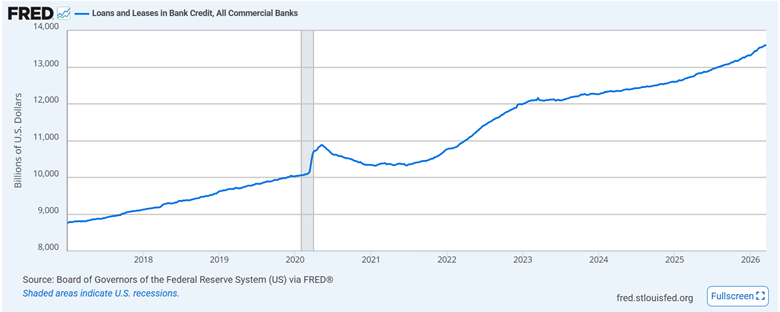

If we look at the structure of U.S. bank lending, the picture becomes perfectly clear. Take Total Loans and Leases: the overall volume of credit (including mortgages and consumer loans) grew by roughly 25%-30% in the post-pandemic period. Over that same time, nominal GDP increased by 50%. This means the economy grew nominally much faster than its credit base. Despite high rates, consumers continued borrowing out of inertia, but even this growth looks modest against the broader inflationary backdrop.

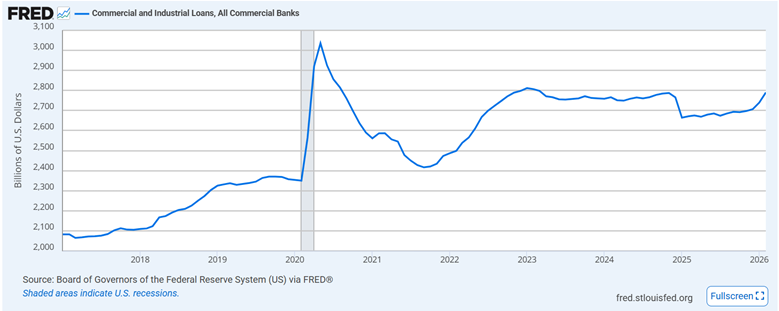

A much more alarming signal, however, comes from the corporate sector. The chart for Commercial and Industrial (C&I) Loans is effectively stagnating. Unlike the average consumer, businesses are guided by harsh math: when the cost of borrowing (high Fed rates) exceeds the expected return on investment, expansion is put on hold. Traditional businesses are not currently taking out loans for development; they are stuck in wait-and-see mode.

As a result, a paradox emerges. Aggregate macroeconomic demand in its current state (with stagnating corporate credit and a high cost of capital) physically lacks the resources to fully absorb and “pay off” the colossal volume of AI services and products currently being developed. The absence of cheap credit acts as a natural brake, suppressing broader economic turnover and limiting external revenue for the tech giants.

The Hidden Driver: Inflationary Deleveraging and the ‘Coiled Spring’ Effect

Looking at the stagnating commercial credit charts, it is easy to fall into pessimism and conclude that a recession is imminent. But there is a nuance: this coin has a positive flip side that the market is catastrophically underestimating right now. The current situation is fundamentally different from the systemic crisis of 2008.

The main distinction lies in the quality of private sector balance sheets. While the financial world has spent the last few years fighting inflation as an absolute evil, it actually fulfilled a crucial macroeconomic function: it inflated away old debts.

The math here is simple. As previously mentioned, U.S. nominal GDP grew from roughly $21 trillion to over $31 trillion. Meanwhile, business and household credit portfolios, constrained by high rates, grew much more slowly. Here we have a unique phenomenon: inflationary deleveraging. American businesses and everyday consumers became “lighter” relative to the new, inflation-adjusted size of the economy.

Unlike 2008, when the economy was over-leveraged and essentially a bubble of bad debt, today we are seeing the exact opposite. The U.S. economy is fundamentally under-leveraged. High Fed rates prevented banks from handing out cheap money, resulting in the cleanest corporate balance sheets we’ve seen in two decades.

This creates a “coiled spring” effect. Companies that spent the last few years on an investment pause, holding off on infrastructure upgrades and production expansion due to the high cost of capital, have accumulated colossal pent-up demand for credit. As soon as the cost of money drops to a level where new projects become profitable again, this pent-up demand will flood the economy. This dormant credit supercycle has enough power to finance the AI industry and pull the entire economy to new all-time highs. However, one fundamental barrier stands in the way of this scenario.

The 2% Trap: Has the Fed’s Main Target Become a Threat to Economic Growth?

Here we pivot from market mechanics to fundamental economic theory. For the “coiled spring” of credit to release, the Federal Reserve must begin an easing cycle. But the regulator is bound hand and foot by its historical mandate: exactly 2% inflation.

A complex but vital discussion is now overdue in the macroeconomic environment: Is the 2% target an excessively rigid and even destructive benchmark in today’s global reality?

If we look back at U.S. economic history, we see that in the 1980s and 1990s, the American economy delivered outstanding growth rates with inflation consistently running above 2%. Levels of 3%, 4%, and even localized spikes to 5% were not viewed as a catastrophe. The economy adapted perfectly: businesses borrowed, new technologies emerged, and capital flowed into the real sector. Inflation acted as a lubricant for the gears of the economic engine, rather than a deadly poison.

Today, however, the situation is compounded by severe geopolitical risks. Amid permanent tension in the Middle East, shipping disruptions, and instability in energy markets, oil and logistics prices create sustained inflationary pressure. Furthermore, attempting to force inflation back into a rigid 2% mandate under these tactical conditions is a titanically complex task.

Striving to hit this ideal, yet potentially outdated, target at all costs means the Fed will be forced to hold rates higher for an unjustifiably long time. A protracted path to 2% is a path of macroeconomic dehydration. By trying to squeeze the last few percentage points of inflation out of the system, the regulator effectively deprives businesses of credit liquidity, suppresses investment activity, and chokes off the very growth potential we see in clean balance sheets and AI technologies.

What is the worst that could happen if the Fed quietly, or even openly, accepts 3%-4% inflation as the new norm? In historical terms, absolutely nothing. This would allow the regulator to transition to rate cuts much faster, reanimating commercial credit and firing up the economic engine to full power.

Time for a Discussion: The Ball Is in the Fed’s Court

In summary, the American market has reached a highly complex crossroads. Structurally, the economy isn’t broken. It has a powerful technological driver in AI and massive, untapped potential in the form of businesses ready for a new credit cycle.

But there is a catch: the engine is stalled, and the keys to the ignition are held by a Federal Reserve that has become a hostage to its own dogma. The conflict of the current moment is a collision between new economic realities and old monetary rules. The future trend of the American market will not be dictated by tomorrow's oil quotes or Big Tech earnings reports, but by the macroeconomic elite's willingness to embrace a paradigm shift.

If the Fed demonstrates historical flexibility, accepts a slightly higher level of inflation as the norm in these new geopolitical realities, and allows the net liquidity curve to turn upward, the economy will get a revitalizing jolt. We will see the “coiled spring” release, justifying almost any valuation in the tech sector.

Conversely, if the Fed continues pursuing its 2% target for a prolonged period, dehydrating the system just for the sake of a perfect number in a report, the market simply won’t have the physical resources (liquidity) left for fundamental growth. Ultimately, all the market can do today is closely monitor the net liquidity chart and wait for the Fed to make its move.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- CoreWeave Just Scored a Major Anthropic Data Center Deal. Does That Make CRWV Stock a Buy Here?

- Is Alibaba Stock a Buy as It Reveals It's Behind the Viral Happy Horse AI Model?

- Bloom Energy Breaks Into Overbought Territory on Oracle Deal. Is It Too Late to Buy BE Stock?

- Meta Is Set to Overtake Google in Digital Ads. Is the Stock a Buy Before April 29 Earnings?