Sysco (SYY) just made its biggest bet in years. On March 30, the largest U.S. foodservice distributor announced a $29.1 billion acquisition of Jetro Restaurant Depot, propelling it into the high-margin cash-and-carry channel serving smaller independent operators.

The deal instantly boosts Sysco’s scale but has triggered a sharp selloff. SYY stock plunged 15% intraday on March 30, marking the largest single-day percentage decline since the March 2020 Covid-19 crash.

Investors are focused on the downsides — $21 billion in new debt that will push leverage up from 2.9 times to roughly 4.5 times, 91.5 million new shares diluting owners by 19.1%, the sudden end to Sysco's big buyback program, and S&P Global cutting the credit outlook to Negative. At the same time, Sysco still offers a solid annualized dividend of $2.16 per share, yielding around 3% at current prices, backed by 55-straight years of increases as a Dividend King.

Wall Street is nervous about all the debt and the risks of making this deal work. But with that steady payout, the big question is whether Sysco's reliable dividend can sweeten what looks like a high-stakes gamble. Let’s take a closer look.

Sysco Overview and Market Position

Headquartered in Houston, Texas, Sysco is the world’s largest food‑away‑from‑home distributor, selling and delivering food and related products to about 730,000 customer locations across restaurants, healthcare, education, lodging, and other institutional channels.

SYY stock trades near $72, down sharply from the 52-week high of $91.85. Shares are down about 2% year-to-date (YTD) and down 4% for the past 12 months. The stock has experienced significant volatility recently, with a 13% five-day decline largely attributable to the acquisition announcement, which sent shares reeling from a pre-deal close of $81.80.

SYY stock carries a forward price-to-earnings (P/E) ratio of 15 times, with a market capitalization of roughly $34.1 billion.

Sysco's second-quarter fiscal 2026 results showed sales of $20.8 billion, reflecting 3% year-over-year (YOY) growth. U.S. Foodservice volume grew 0.8% overall and 1.2% locally, marking the third consecutive quarter of positive local case growth. Gross profit rose 3.9% to $3.8 billion, with margins expanding 15 basis points to 18.3%. Adjusted operating income increased 3.1% to $807 million, while adjusted net earnings grew 3.9% to $476 million. Adjusted EPS came in at $0.99, climbing 6.5% YOY, while adjusted EBITDA rose 3.3% to $1 billion.

Sysco ended the quarter with $1.2 billion of cash and total liquidity of about $2.9 billion. Net debt to adjusted EBITDA stood at around 2.9 times, consistent with an investment‑grade balance sheet before the Jetro deal.

CEO Kevin Hourican highlighted “strong results […] driven by increased local case growth” and momentum from key initiatives while CFO Kenny Cheung emphasized “high-quality performance across the income statement and cash flow.” The company's figures underscore operational discipline even as the market digests Sysco's transformative acquisition.

Sysco’s Growth Strategy and Strategic Developments

Sysco's move to acquire Jetro Restaurant Depot for $29.1 billion marks a major expansion into the high-margin, resilient cash-and-carry segment. The deal includes $21.6 billion in cash and 91.5 million shares of SYY stock issued to Jetro shareholders. Based on the stock’s $81.80 closing price on March 27, that values Jetro at about 14.6 times its operating income, or 13 times once counting the expected savings.

To pay for it, Sysco is borrowing roughly $21 billion in new debt and using about $1 billion from cash or other sources. That will push its leverage higher for a bit, so mangement is pausing share buybacks while they focus on paying down the debt.

Jetro, which serves a $60 billion to $70 billion market, will run as its own segment within Sysco. Management expects about $250 million in yearly cost savings within three years, mostly from better purchasing and supply‑chain efficiencies. Mangement also believes the deal should add mid‑ to high‑single‑digit percentage growth to EPS in the first year and ramp to low‑ to mid‑teens in the second year.

As for the dividend, Sysco isn’t touching it. The company just declared the next quarterly payment, keeping the annual payout at $2.16 per share, translating to a yield of roughly 3%. The next payment is due April 24, 2026, to shareholders of record on April 2, 2026. With a payout ratio of 45.73% and 55 consecutive years of increases, the dividend will remain rock-solid even through this big acquisition.

What Do Analysts Think of Sysco Stock?

Sysco just reaffirmed fiscal 2026 adjusted EPS guidance, keeping earnings at the high end of $4.50 to $4.60 per share. Management is counting on at least 2.5% local sales growth in the second half of the year, plus the usual push from day-to-day operations.

For the current quarter, analysts are looking for about $0.95 per share. That’s pretty close to the $0.99 earned in the most recent quarter.

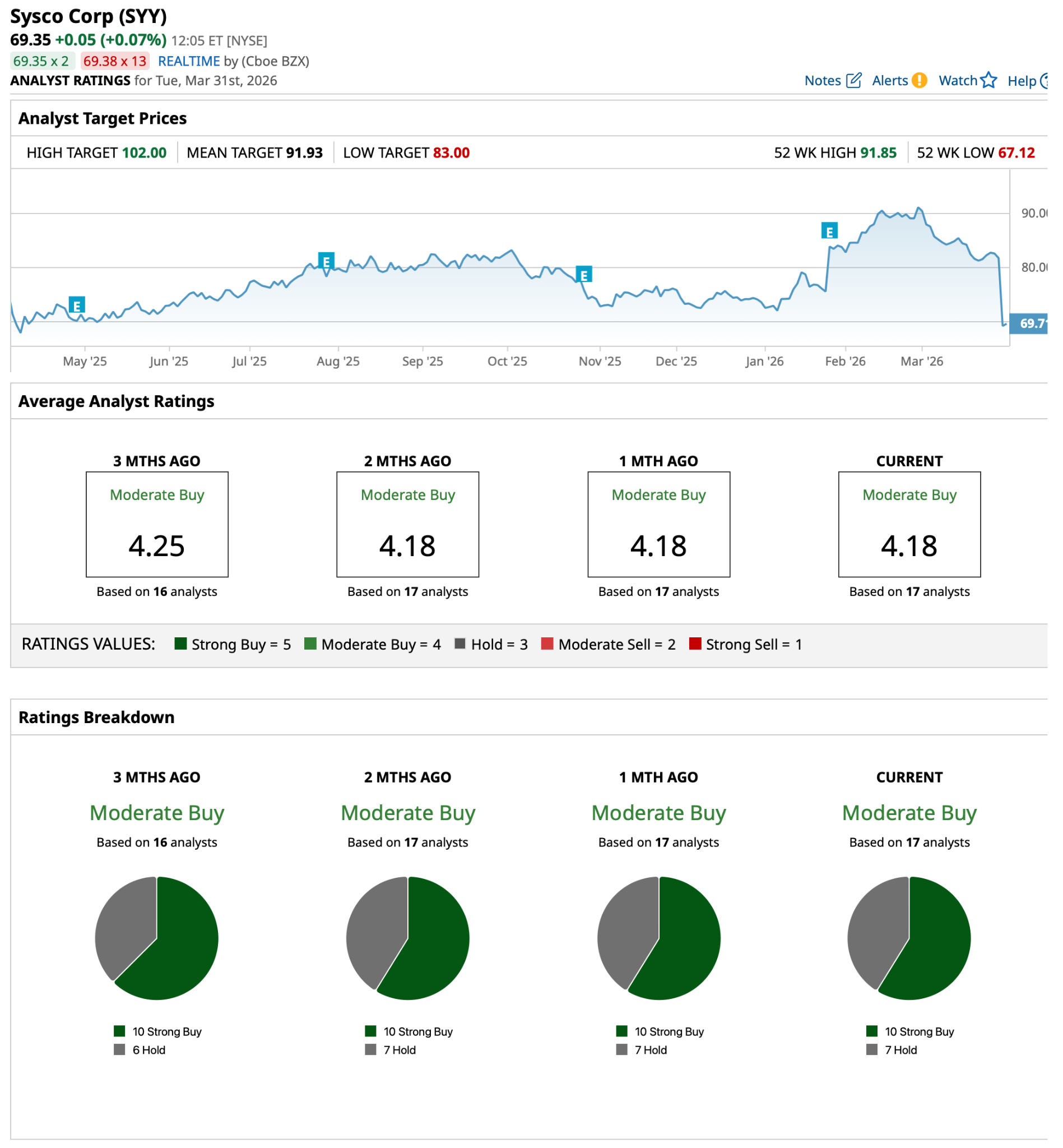

Based on 17 analysts with coverage, SYY stock has a “Moderate Buy" consensus rating. The average price target of $90.78 points to potential upside of roughly 26% from current levels.

Conclusion

Sysco is paying full price for Jetro and borrowing a ton of money to make it happen, especially with interest rates still high. That’s exactly why SYY stock tanked right after the news. But the main business is still growing at a decent pace. Sysco throws off strong free cash flow, and it keeps paying a solid dividend that has been raised for more than 50 years.

I expect the stock to calm down and slowly head higher over the next six to 12 months as the cost savings start showing up and that dividend keeps compounding. Sysco looks like a good buy right now for income investors who are okay with this big move.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart