With a market cap of $14.4 billion, Generac Holdings Inc. (GNRC) is a leading manufacturer of backup power generation equipment, energy technology solutions, and other power products for residential, commercial, and industrial customers. Headquartered in Waukesha, Wisconsin, the company is best known for its standby and portable generators, particularly for homes and businesses seeking protection against power outages and grid instability.

Shares of this backup power giant have outperformed the broader market over the past year. GNRC has gained 89.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 23.3%. In 2026, GNRC stock is up 78.9%, surpassing the SPX’s 7.4% YTD rise.

Zooming in further, GNRC has also surpassed the State Street Industrial Select Sector SPDR Fund (XLI), which has gained 17% over the past year and returned 8.8% in 2026.

On Apr. 29, Generac shares popped 16.5% after the company released its Q1 2026 earnings. Driven by robust growth in its commercial and industrial business, improving profitability, and rising demand for backup power solutions amid ongoing grid reliability concerns, its net sales increased 12% year over year to $1.06 billion. Its adjusted EPS stood at $1.80, up 42.9% from the prior-year quarter, significantly exceeding analyst expectations.

For fiscal 2026, ending in December, analysts expect GNRC’s EPS to grow 40.5% to $8.91 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

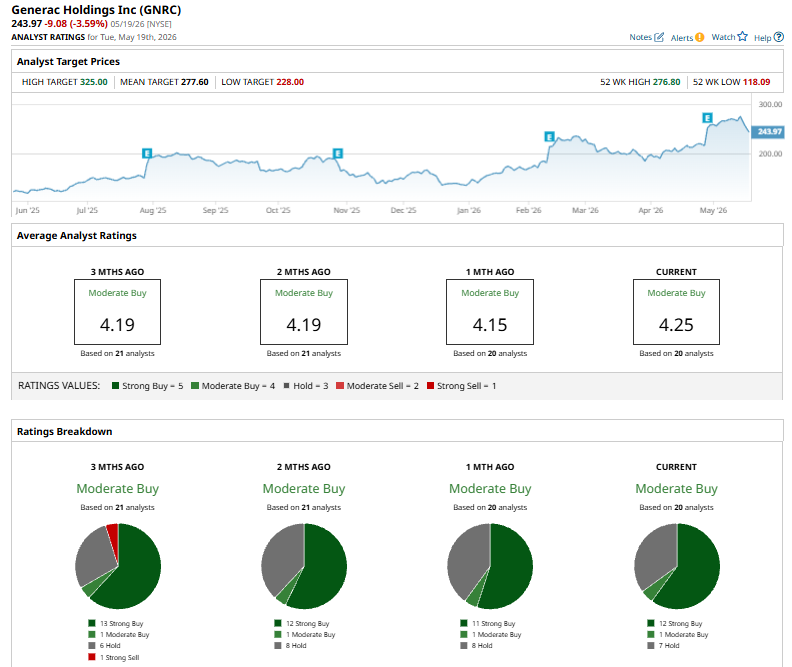

Among the 20 analysts covering GNRC stock, the consensus is a “Moderate Buy.” That’s based on 12 “Strong Buy” ratings, one “Moderate Buy,” and seven “Holds.”

This configuration is bullish than a month ago, with 11 analysts suggesting a “Strong Buy.”

On May 5, UBS analyst Jon Windham maintained a “Buy” rating on Generac Holdings and raised the price target to $305 from $270, reflecting continued confidence in Generac’s growth outlook and demand trends across its power and energy solutions business.

Its mean price target of $277.60 implies a premium of 13.8% from the current market prices, and the Street-high price target of $325 suggests an upside potential of 33.2%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Paul Tudor Jones’ Hedge Fund Buys 7 Million Shares of Warner Bros. Discovery. The WBD Stock Turnaround Could Finally Be Here.

- Don’t Panic, Says Our Top Technical Strategist. The Charts Say an S&P Pullback from Here Could Be Constructive.

- Everyone’s Turning Bearish on Tesla Ahead of SpaceX IPO. Be a Contrarian and Buy TSLA Stock Instead.