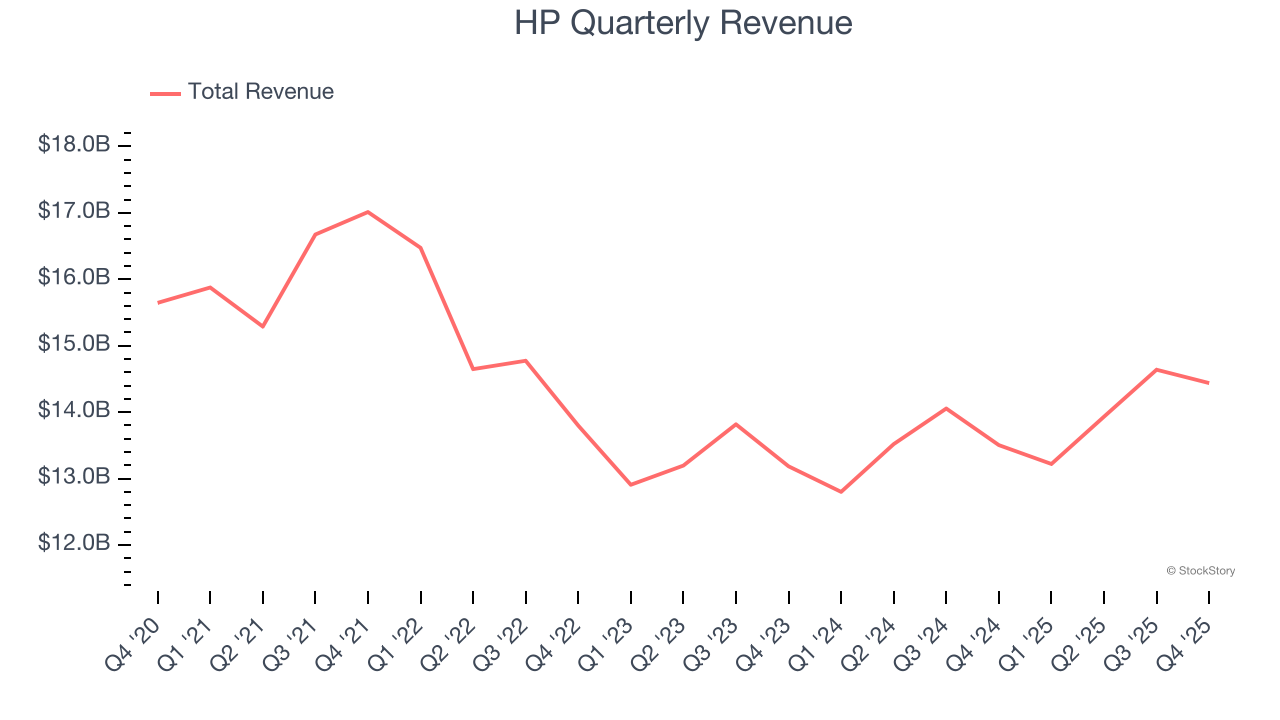

Personal computing and printing company HP (NYSE: HPQ) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 6.9% year on year to $14.44 billion. Its non-GAAP profit of $0.81 per share was 5.3% above analysts’ consensus estimates.

Is now the time to buy HP? Find out by accessing our full research report, it’s free.

HP (HPQ) Q4 CY2025 Highlights:

- Revenue: $14.44 billion vs analyst estimates of $13.99 billion (6.9% year-on-year growth, 3.2% beat)

- Adjusted EPS: $0.81 vs analyst estimates of $0.77 (5.3% beat)

- Adjusted EBITDA: $1.16 billion vs analyst estimates of $1.16 billion (8% margin, 0.8% miss)

- Management reiterated its full-year Adjusted EPS guidance of $3.05 at the midpoint

- Operating Margin: 5.3%, down from 6.3% in the same quarter last year

- Free Cash Flow Margin: 1%, similar to the same quarter last year

- Market Capitalization: $16.85 billion

"We are pleased to report a strong first quarter, highlighted by robust growth in Personal Systems, including the continued momentum in AI PCs. Our performance reflects the strength of our portfolio and our disciplined execution of our Future of Work strategy, even as we navigate industry-wide headwinds,” said Bruce Broussard, Interim CEO, HP Inc.

Company Overview

Born from the legendary Silicon Valley garage startup founded by Bill Hewlett and Dave Packard in 1939, HP (NYSE: HPQ) designs and sells personal computers, printers, and related technology products and services to consumers, businesses, and enterprises worldwide.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $56.23 billion in revenue over the past 12 months, HP is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. To accelerate sales, HP likely needs to optimize its pricing or lean into new offerings and international expansion.

As you can see below, HP struggled to increase demand as its $56.23 billion of sales for the trailing 12 months was close to its revenue five years ago. This shows demand was soft, a tough starting point for our analysis.

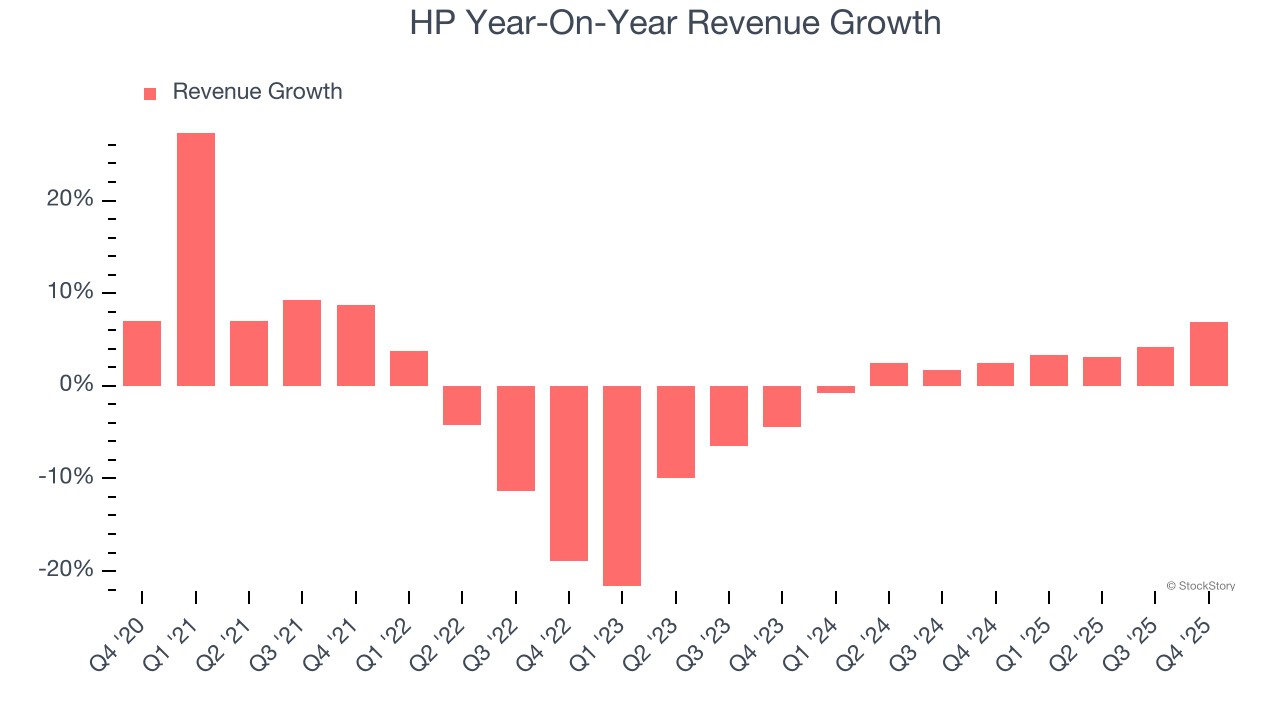

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. HP’s annualized revenue growth of 2.9% over the last two years is above its five-year trend, which is encouraging.

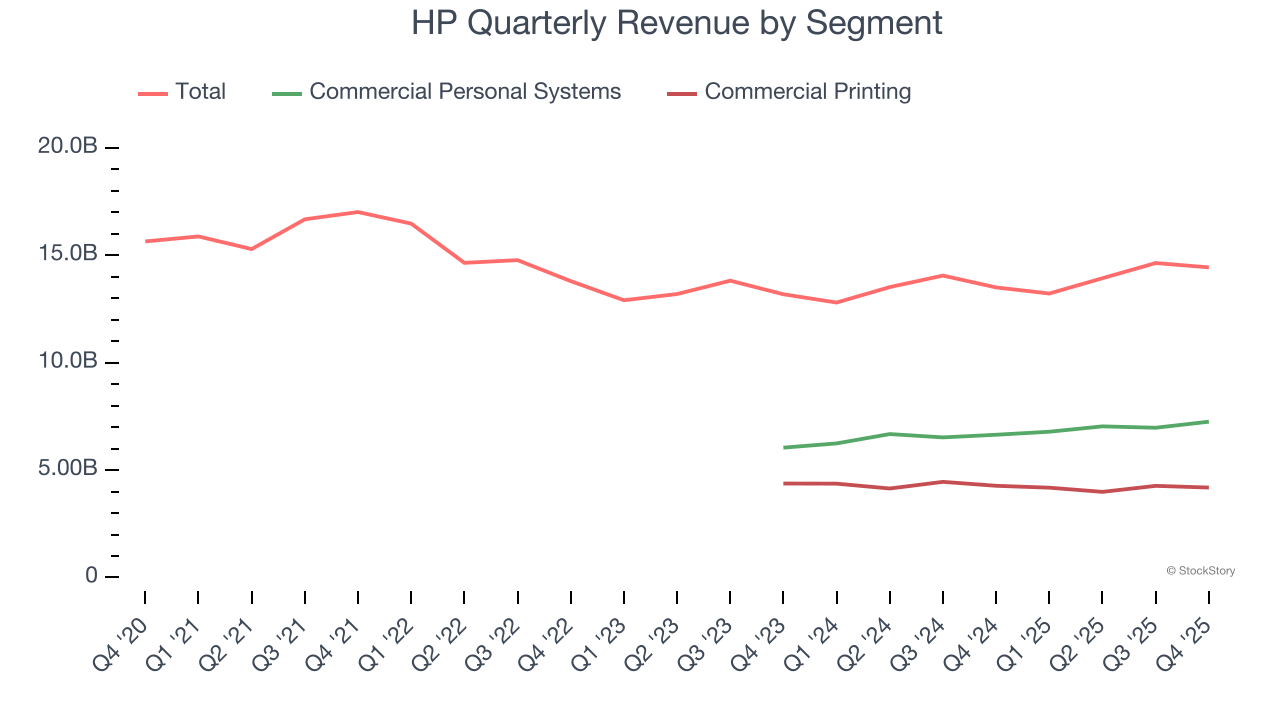

HP also breaks out the revenue for its most important segments, Commercial Personal Systems and Commercial Printing, which are 50.2% and 29% of revenue. Over the last two years, HP’s Commercial Personal Systems revenue (desktops, laptops, etc.) averaged 8% year-on-year growth. On the other hand, its Commercial Printing revenue (commercial or industrial printers) averaged 3.3% declines.

This quarter, HP reported year-on-year revenue growth of 6.9%, and its $14.44 billion of revenue exceeded Wall Street’s estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to decline by 2.1% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

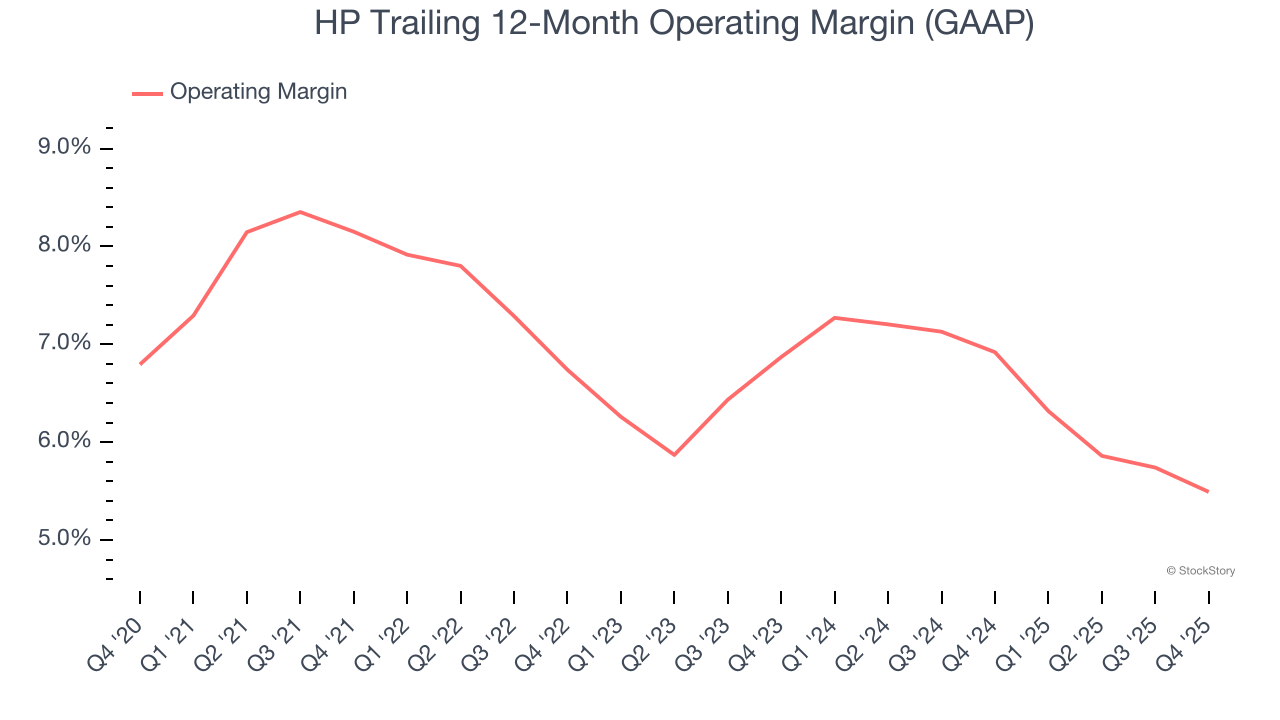

Operating Margin

HP was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.9% was weak for a business services business.

Analyzing the trend in its profitability, HP’s operating margin decreased by 2.7 percentage points over the last five years. HP’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, HP generated an operating margin profit margin of 5.3%, down 1 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

HP’s EPS grew at an unimpressive 4.7% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

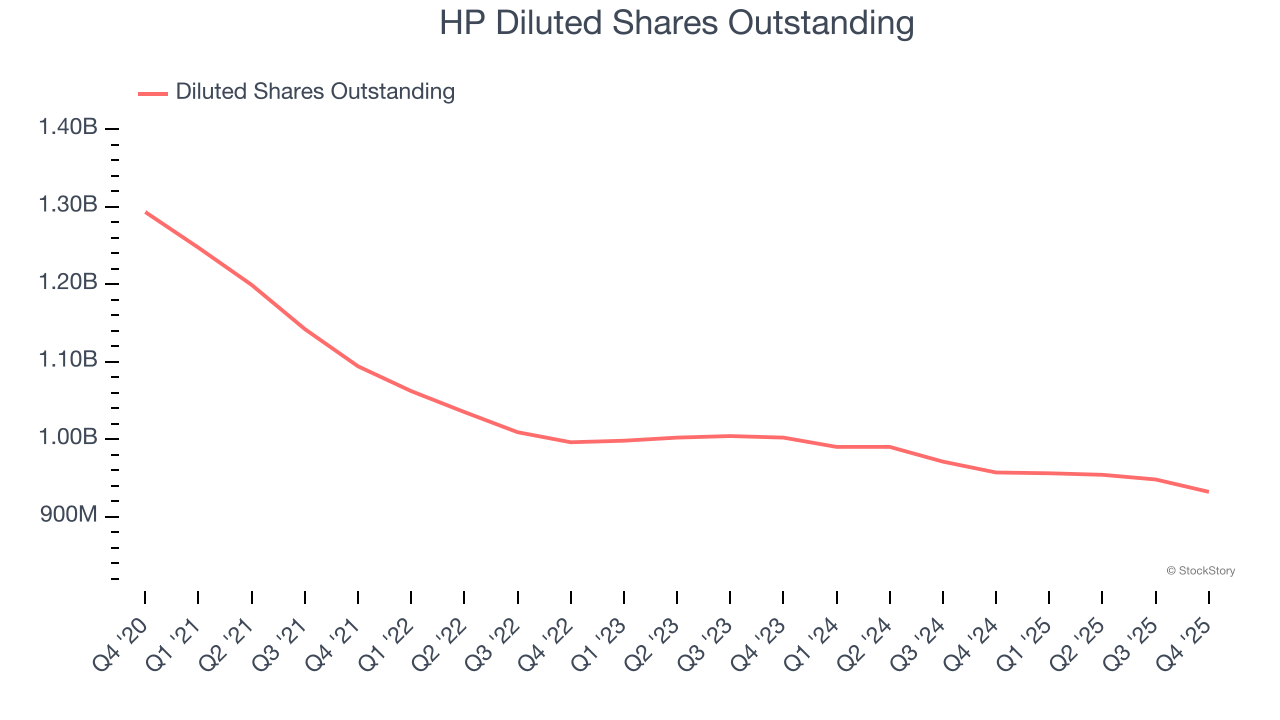

Diving into the nuances of HP’s earnings can give us a better understanding of its performance. A five-year view shows that HP has repurchased its stock, shrinking its share count by 27.9%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For HP, its two-year annual EPS declines of 2.6% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, HP reported adjusted EPS of $0.81, up from $0.74 in the same quarter last year. This print beat analysts’ estimates by 5.3%. Over the next 12 months, Wall Street expects HP’s full-year EPS of $3.20 to shrink by 9.4%.

Key Takeaways from HP’s Q4 Results

We enjoyed seeing HP beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 5.4% to $17.21 immediately following the results.

Is HP an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).